Our New Portfolio Pick in the Pentagon's Line of Sight

For 35 years the US hasn't had a meaningful fluorspar producer. We've just added the ASX small-cap chasing the gap.

The United States hasn’t had a meaningful fluorspar mine since 1990.

In January, the Pentagon handed US$169 million to the only permitted producer left on American soil.

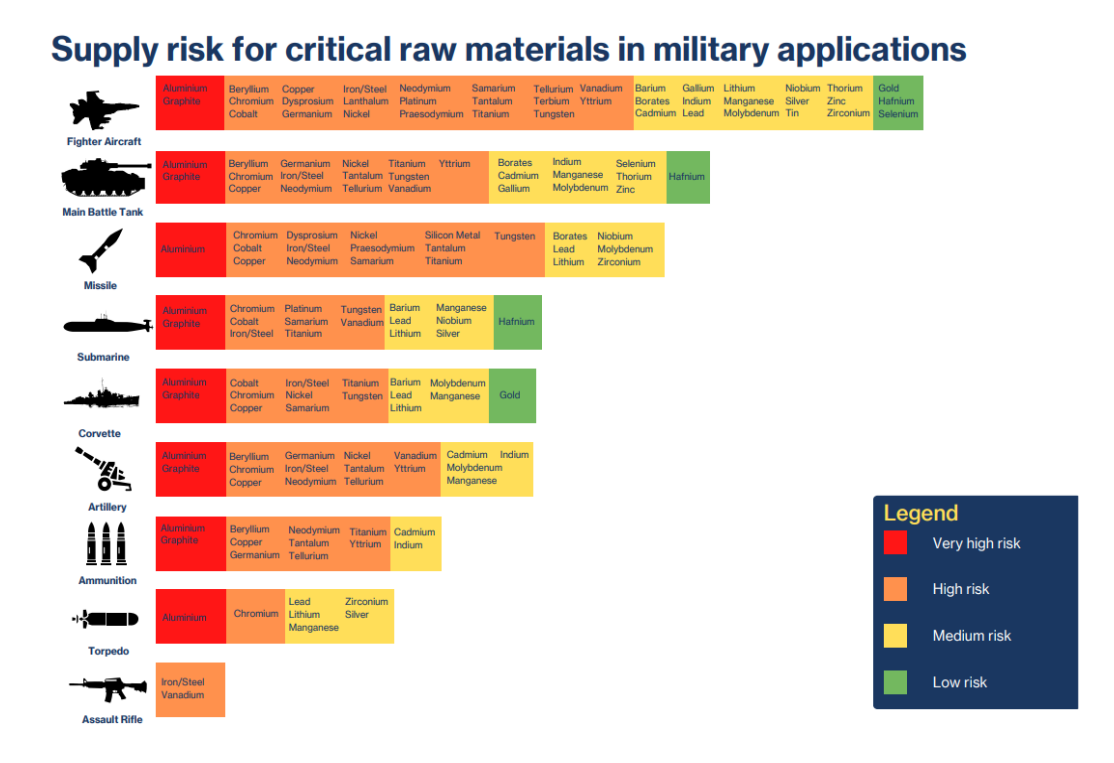

Without fluorspar, the modern world stops working. Lithium-ion batteries. Semiconductor chips. Refrigerants. Jet engine alloys. Uranium enrichment. None of it gets made at scale.

China produces 60% of the world’s supply. The US imports 100%.

Graphite is a similar story. It’s the largest raw material in every EV battery on the planet. The US imports 70% of its supply, and nearly all the battery-grade material comes from Chinese-controlled plants.

As of this week, one ASX-listed company has active projects in both.

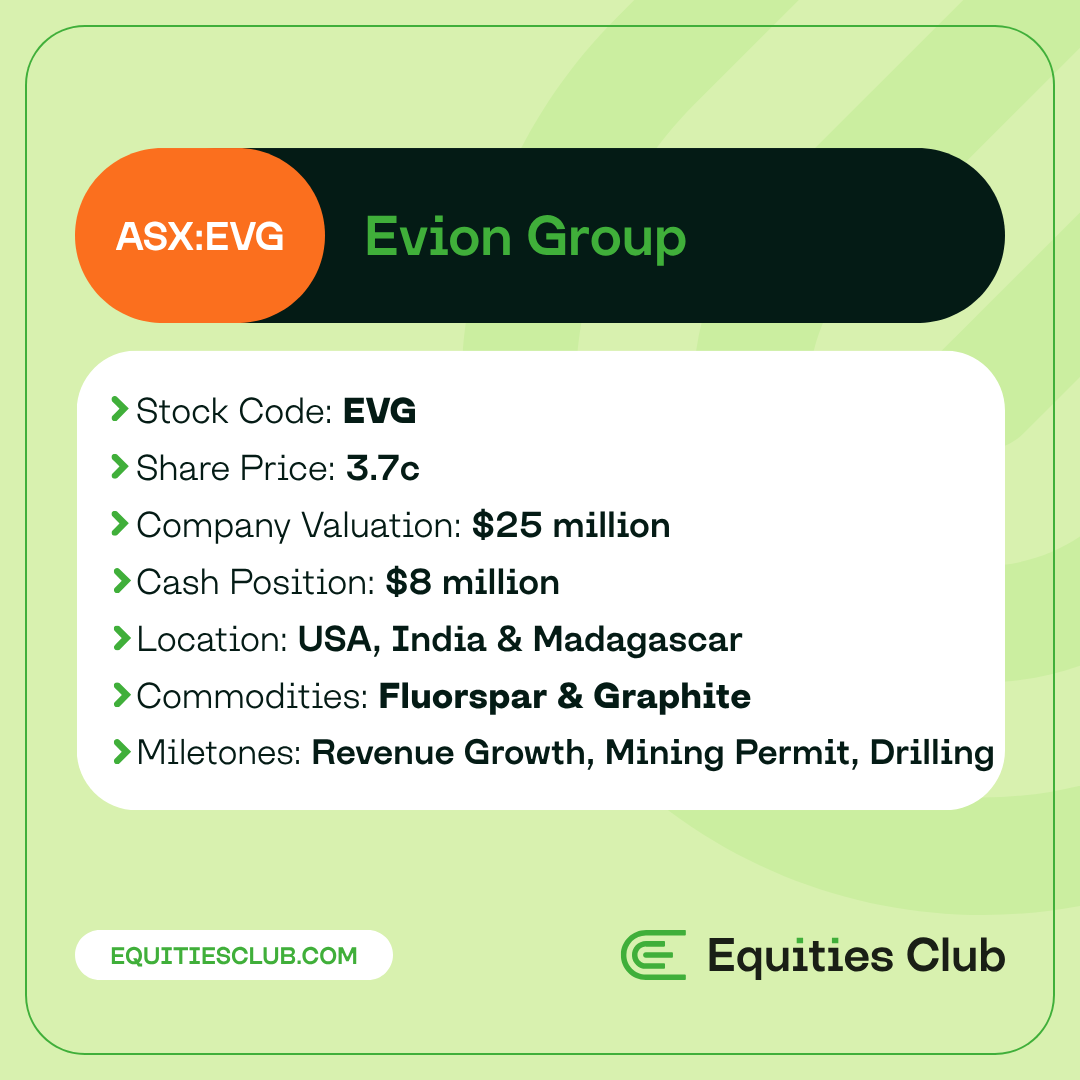

Meet Evion Group (ASX: EVG), our latest portfolio addition.

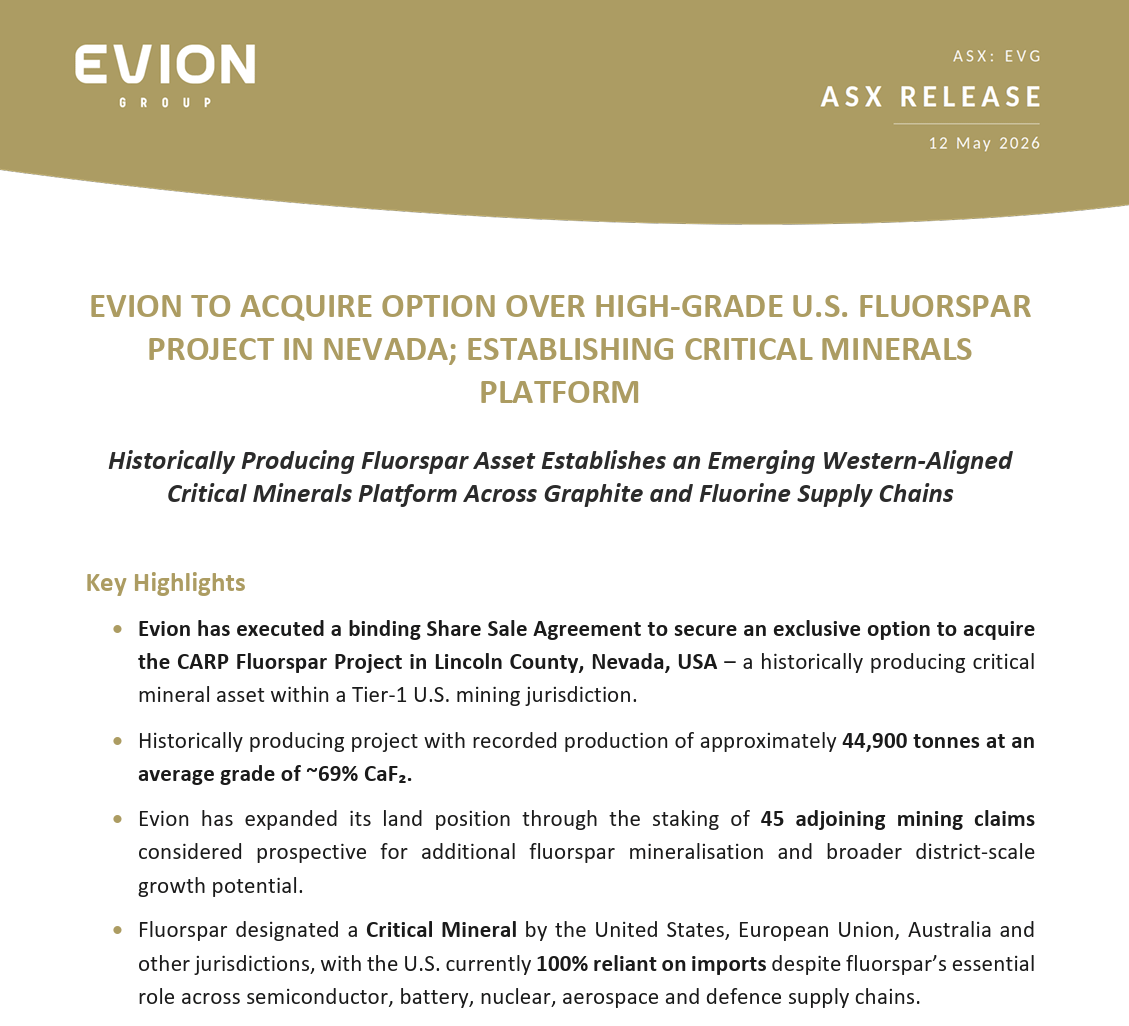

EVG just signed a binding option for 100% of the Carp Fluorspar Project in Nevada, the world’s number one ranked mining jurisdiction. The ground has historic US production behind it, modern sampling has come back strong, and it sits inside a US state already home to plenty of working ASX miners.

It’s the profile Washington is now writing nine-figure cheques for.

In Madagascar, EVG’s flagship graphite project is weeks away from its mining permit. The technical work is signed off. The licensing body has been told to push the paperwork through.

EVG’s Indian joint venture, shipped its first major US order in December: A$1.5 million of expandable graphite to a buyer that needs non-Chinese supply. A second order has followed, with management flagging more soon.

Three legs across three continents, with no Chinese partners anywhere in the chain. The graphite project in Madagascar, the processing plant in India, and now the fluorspar asset in the United States.

Two of the most strategic minerals on the planet, sitting under one ASX ticker.

At 3.7 cents, EVG trades on a $25 million market cap with $8 million in the bank to deliver on all of it.

Let’s dig in.

Why Fluorspar Matters

Most people who’ve heard of fluorspar couldn’t tell you what it does.

That’s a problem, because there’s a decent argument that no industrial mineral on the planet is doing more work right now.

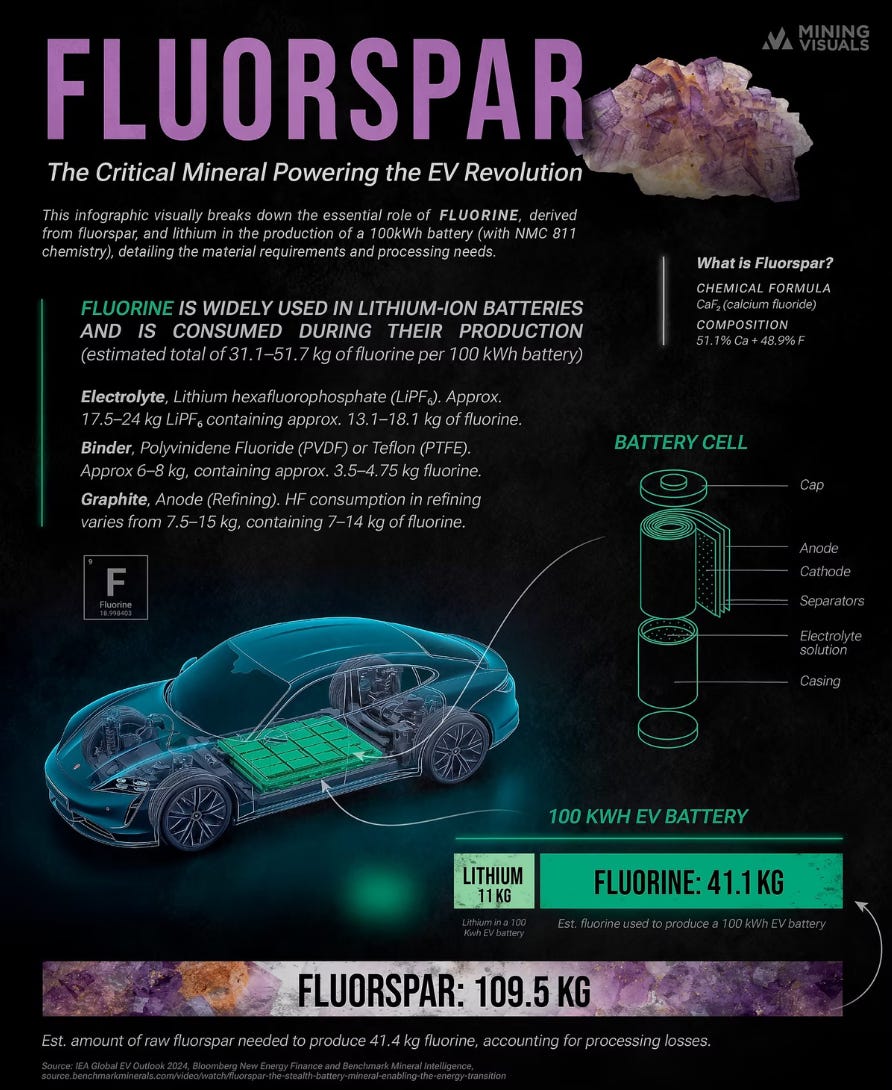

Fluorspar is a calcium fluoride mineral. Refine the high-grade stuff, add water, and you get hydrofluoric acid.

Hydrofluoric acid is the starting point for an entire branch of industrial chemistry that almost everything modern depends on.

Lithium-ion batteries are built around an electrolyte salt called LiPF₆, made with fluorine, sourced from fluorspar. Without it, the modern battery doesn’t exist.

Every advanced semiconductor chip is etched and cleaned with fluorine-based chemistry. NVIDIA's latest AI chips, the silicon inside an iPhone, the processor in a car's brake controller, all made using fluorine.

Enriched uranium runs on uranium hexafluoride. The “hexafluoride” is six fluorine atoms.

Refrigerants, jet engines, pharmaceuticals, Teflon. The list goes on. There’s no commercially scalable lithium-ion chemistry without fluorine, and no fluorine without fluorspar.

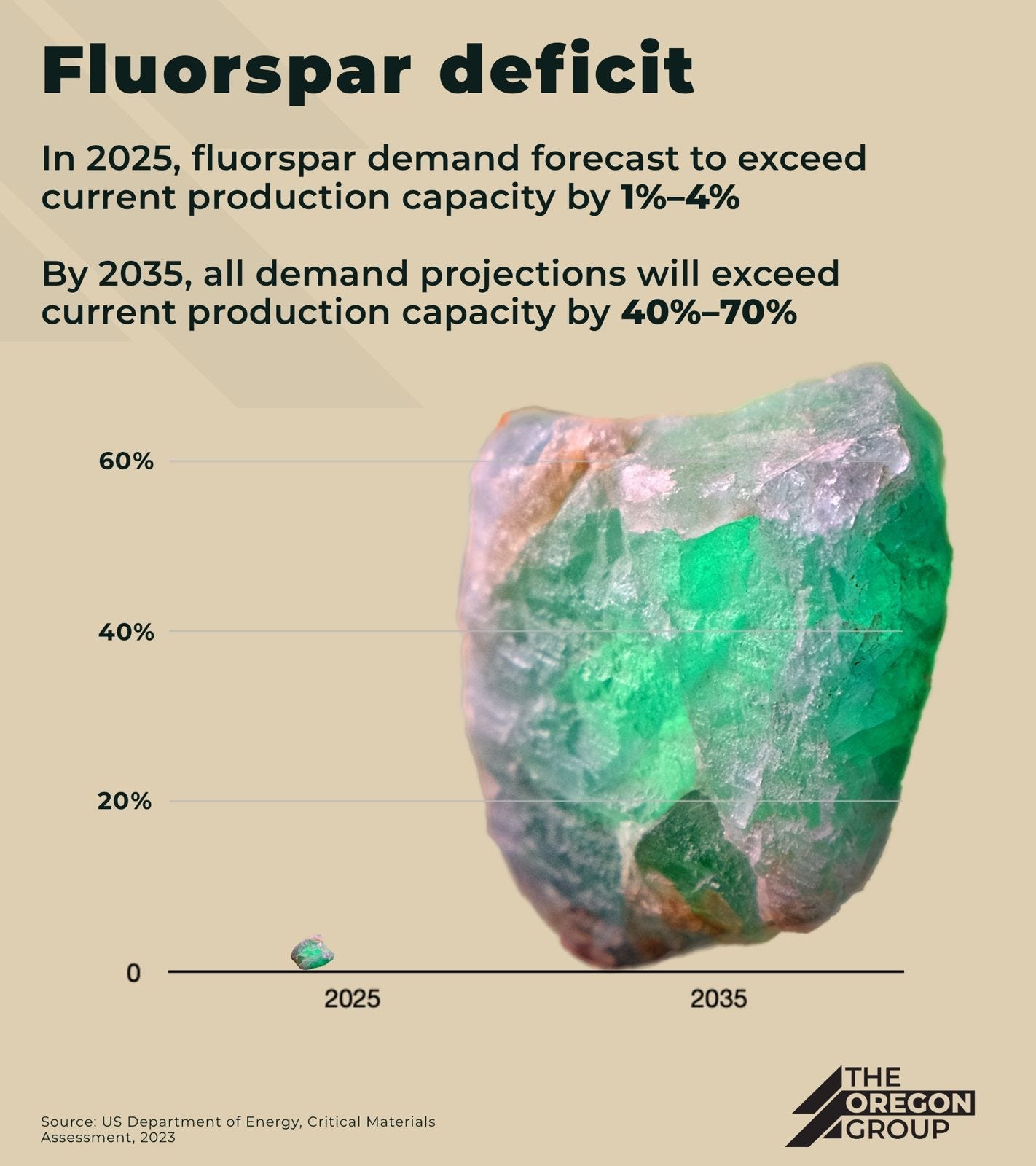

By 2035, industry forecasts have global demand running 40% to 70% above production capacity. Acidspar (the high-grade material) currently trades between US$450 and US$650 a tonne.

Supply has nowhere to go in the short term, and demand is being driven by the four hardest-to-replace use cases on the planet: batteries, chips, nuclear and defence.

That’s the gap EVG has just stepped into.

“In considering this acquisition, we carefully reviewed the economic and geopolitical dynamics that currently exist for this commodity and discovered, as others have too, that the US is a large consumer of this material but has previously relied on imports from China and other parts of the world.”

- Evion Managing Director David Round

The Nevada Deal

In the late 1960s, trucks rolled out of a series of open pits 140km northeast of Las Vegas loaded with high-grade fluorspar bound for California.

The destination was Kaiser Steel Corporation, the west coast's biggest steelmaker at the time and one of the industrial heavyweights of America.

44,900 tonnes came out of the ground at an average grade of 69% CaF₂, crushed and shipped without any further processing.

Production stopped in 1971 when cheap imports flooded the US market and made small American producers uneconomic.

The rock didn't run out. The market just walked away from US fluorspar entirely.

This is the ground EVG has just secured.

The project is called Carp, and it sits in Lincoln County about 140km northeast of Las Vegas.

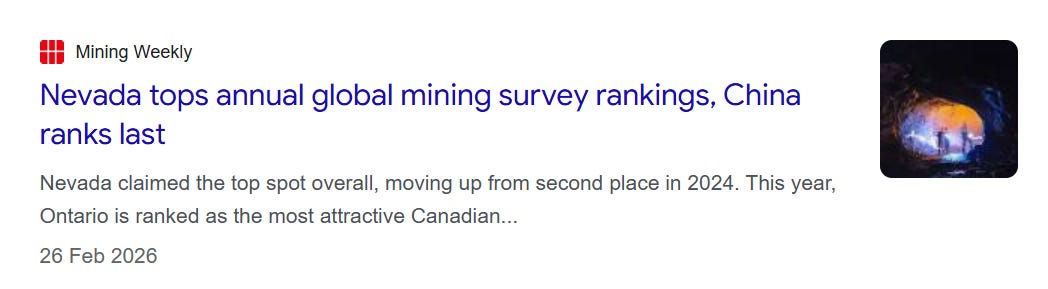

Nevada is the world’s number one ranked mining jurisdiction by the Fraser Institute, and Lincoln County itself has hosted gold, silver and industrial mineral operations for over a century.

Plenty of ASX names are already working in the state, so the regulatory pathways and contractor networks are well understood.

EVG has signed a binding option agreement with Globex Nevada Inc. for 100% of the project. The structure is light upfront with staged payments tied to milestones over the next three to four years.

Around the historic mine, EVG has also staked 45 adjacent unpatented claims, materially expanding the project footprint beyond the original ground.

A 2024 surface program across the project returned grades up to 88.15% CaF₂. Fourteen of 25 samples came back between 49.8% and 88.15%. The widest stretch was 5 metres at over 78% CaF₂ in the West pit.

There are two things to take from that.

At 69%, Carp historically made money. That's metspar grade, sold straight to steelmakers as a flux. The original operation didn't need to upgrade the rock at all, and the metspar market is still alive today.

The modern sampling is coming back much stronger. Samples hitting 88% sit a long way above the historic grade, and they're heading toward the acidspar threshold (97%+) where the real money lives.

Acidspar is the gateway to batteries, chips, refrigerants and uranium enrichment.

The geologist who ran the work also noted the analytical method wasn’t calibrated to high-grade fluorspar standards, so actual grades likely sit higher than reported.

The path from metspar producer to acidspar producer isn’t automatic, and that’s the work EVG has to do from here.

Rock chips and channel samples are selectively taken from the best-looking material on the ground and don’t represent bulk grade. They need to be confirmed by systematic drilling and metallurgical testwork before anyone gets too far ahead of the story.

The floor on Carp is the same business Kaiser Steel was buying in 1968, in a market that hasn’t gone away.

The ceiling is a fluorspar feedstock for the modern battery and semiconductor supply chain.

Both stories are in play.

Five Reasons We’re Backing Evion Group

1. Two Critical Minerals, One Stock

EVG is the only ASX-listed company with active projects in both graphite and fluorspar.

Both minerals appear on the US, EU, Australian, Canadian and Japanese critical minerals lists.

China dominates the production and processing of both. The US imports nearly 100% of its fluorspar and roughly 70% of its graphite (and almost all of its battery-grade graphite).

Western buyers are scrambling for non-Chinese alternatives, and the policy money following them runs to tens of billions.

Most ASX critical minerals stories give you one shot at one commodity. EVG gives you two, across three continents, with no Chinese partners in the chain.

If one of these legs rerates the way comparable single-commodity plays have, the $25 million market cap looks too cheap.

If both rerate, EVG is a different company at a different share price.

2. The US Cheque Book Is Already Open for Fluorspar

We hit on this earlier, but it bears repeating.

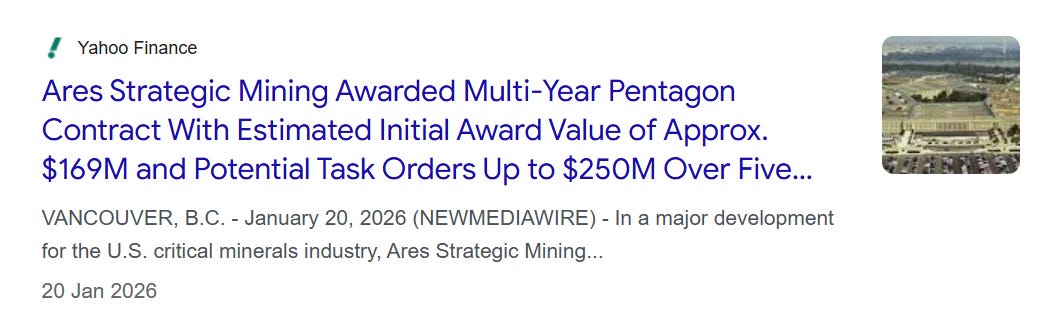

In January 2026, the US Department of Defense awarded a US$169 million fluorspar supply contract to Ares Strategic Mining, for its Lost Sheep mine in Utah.

The deal can scale to US$250 million over five years. Ares is the only fully permitted fluorspar mine in the United States, and the company has been restarting production specifically to meet this contract.

One mine, one contract, US$169 million from the Pentagon up front.

That’s the most direct comparable available for what a US-based fluorspar developer can attract.

Behind that one contract sits a much broader US policy push:

FAST-41 fast-tracks federal permitting for critical mineral projects

Project Vault, launched in February, sets up a US$12 billion strategic mineral stockpile

The Defense Production Act funds domestic processing and manufacturing capacity directly

The DOE Loan Programs Office is sitting on hundreds of billions of dollars of authority for critical mineral projects

EXIM, DFC, CHIPS Act funding for semiconductor inputs, and the FORGE program coordinating supply across 54 allied countries are all backing projects in the profile EVG has just acquired

All of it pointed at moving critical minerals supply out of Chinese hands.

For EVG, the Carp asset sits on BLM (Bureau of Land Management) public land, outside any conservation or wilderness area, in the world’s number one ranked mining jurisdiction.

That puts it inside the US funding architecture from day one.

The path to a meaningful US contract or grant on a fluorspar asset is well within reach for a 3.7c stock. The job from here is execution.

3. Maniry Is A Permit Away from Production

Madagascar sits on one of the biggest graphite endowments outside China, at grades most western producers couldn't dream of.

Maniry is EVG’s flagship project there. The team has been chasing a mining permit for years, and the asset has been the quiet hand behind the share price.

That’s about to change.

Maniry holds Strategic Project status under the EU's Critical Raw Materials Act. In plain English, that means Brussels has formally backed the project as part of Europe's plan to build a non-Chinese battery supply chain.

The designation unlocks EU grants, project finance, and preferred offtake partners. Maniry is the only graphite project in Africa carrying it.

The Definitive Feasibility Study, completed in 2022, has Maniry producing 60,000 tonnes of graphite concentrate per year for 21 years, with a pre-tax net present value of US$263 million.

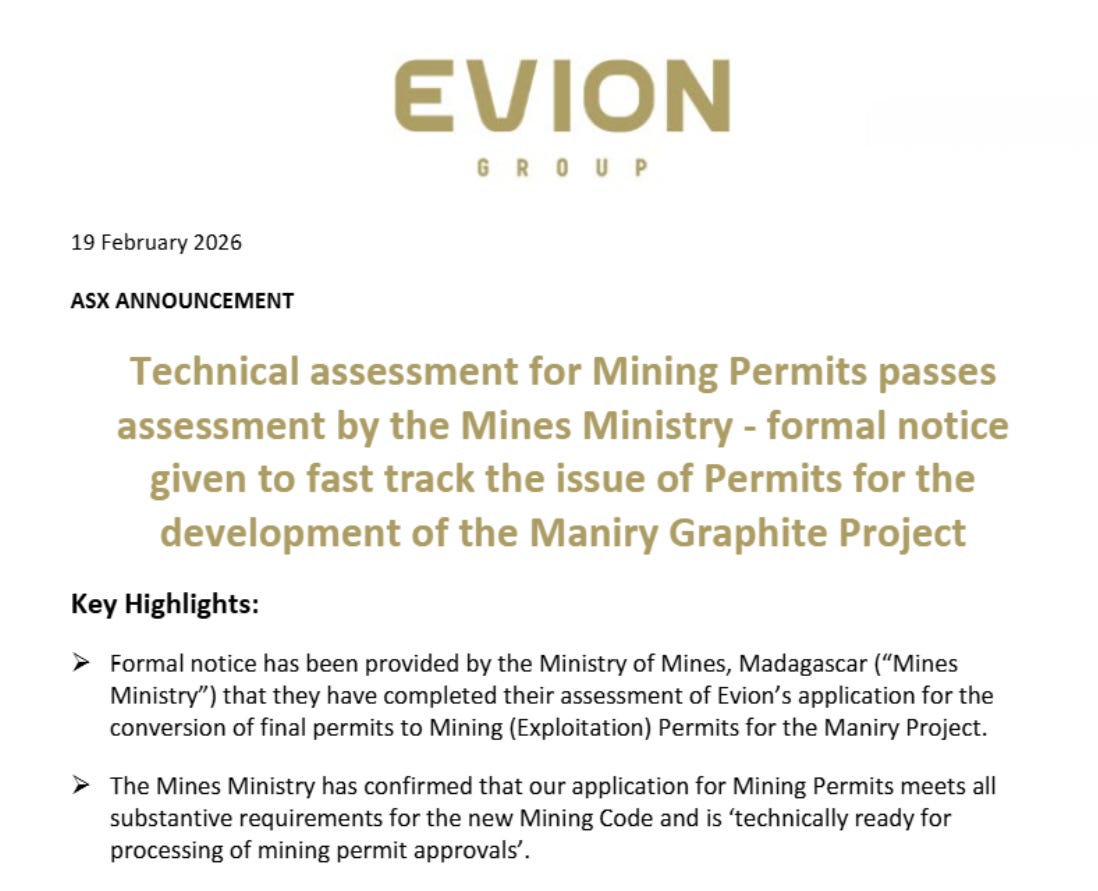

In February, the Madagascar Mines Ministry confirmed EVG’s application meets all substantive requirements of the country’s new mining code.

The technical assessment is complete. The Ministry has formally directed the Mining Cadastre (the body that issues the permits) to process the conversion from exploration to exploitation permit (a mining permit).

When the permit lands, a few things happen at once. Offtake negotiations open. Construction planning starts. A €3 million EU grant EVG has been working toward gets unlocked.

The company is also in advanced talks with the European Investment Bank and KfW Development Bank on project financing. Both are weighing in for the same reason the EU designation exists in the first place.

The EU has separately committed over US$100 million to Madagascar for infrastructure, healthcare, and integration of local resources into global supply chains.

That’s the political backdrop EVG is operating in.

When the permit lands, EVG stops being an explorer with an asset and starts being a developer with a mine to build.

4. The India JV Is Already Generating Cash

This is the piece that gets overlooked. We did a double-take when we got to it.

EVG runs a 50/50 joint venture with Indian operator Metachem Manufacturing, called Panthera Graphite Technologies. The two operate an expandable graphite plant near Pune, already producing and selling product into the US, Europe and Asia.

The plant started shipping in March 2025. Around 120 tonnes went out the door in the March 2026 quarter alone.

Expandable graphite is a higher-margin specialty product. It goes into fire retardants, gaskets, thermal management, defence applications, and increasingly into batteries.

Very few non-Chinese producers operate at scale, and EVG is the only Australian-listed one.

The first major US order landed in December 2025 at A$1.5 million. A second sales order has since followed, with management flagging further orders in the short term.

US buyers are chasing non-Chinese supply, and the Panthera JV is one of the few places they can get it.

Stage 2 upgrades are underway to lift annual capacity to 4,000-4,500 tonnes. At current pricing, that's roughly A$18 to A$20 million in annual sales from the plant, with EVG entitled to half through its stake.

The modifications wrap up this quarter, with materially higher production rates from the June quarter on.

Then there's the IRA angle. Graphite processed by a non-Chinese entity in India and sold to a US battery maker is FEOC-compliant under the Inflation Reduction Act.

FEOC means "Foreign Entity of Concern", and getting around it is worth up to US$7,500 per vehicle in tax credits for the US carmaker buying the material.

Buyers chasing that credit are the same buyers filling Panthera’s order book right now.

For a junior critical minerals company, having real revenue, a growing order book, and a structural tax advantage in one of the most strategic commodities on the planet is extremely rare.

5. Tight Setup, Fully Funded

Alongside the Carp announcement, EVG raised A$6 million at 3 cents per share through a two-tranche placement. Combined with existing cash, the company sits on roughly A$8 million.

That puts the enterprise value at around $17 million.

For $17 million you get:

An EU-backed graphite project with a US$263 million pre-tax NPV from its 2022 DFS

A revenue-generating expandable graphite JV in India, ramping to A$18-20 million in annual sales

A US fluorspar asset with the same profile as the one that just landed a US$169 million Pentagon contract

The cash on hand takes Carp through verification work, pushes Maniry to permit and offtake, and funds Stage 2 at the India JV.

No trip back to the market in the short term, and no dilution event hanging over holders.

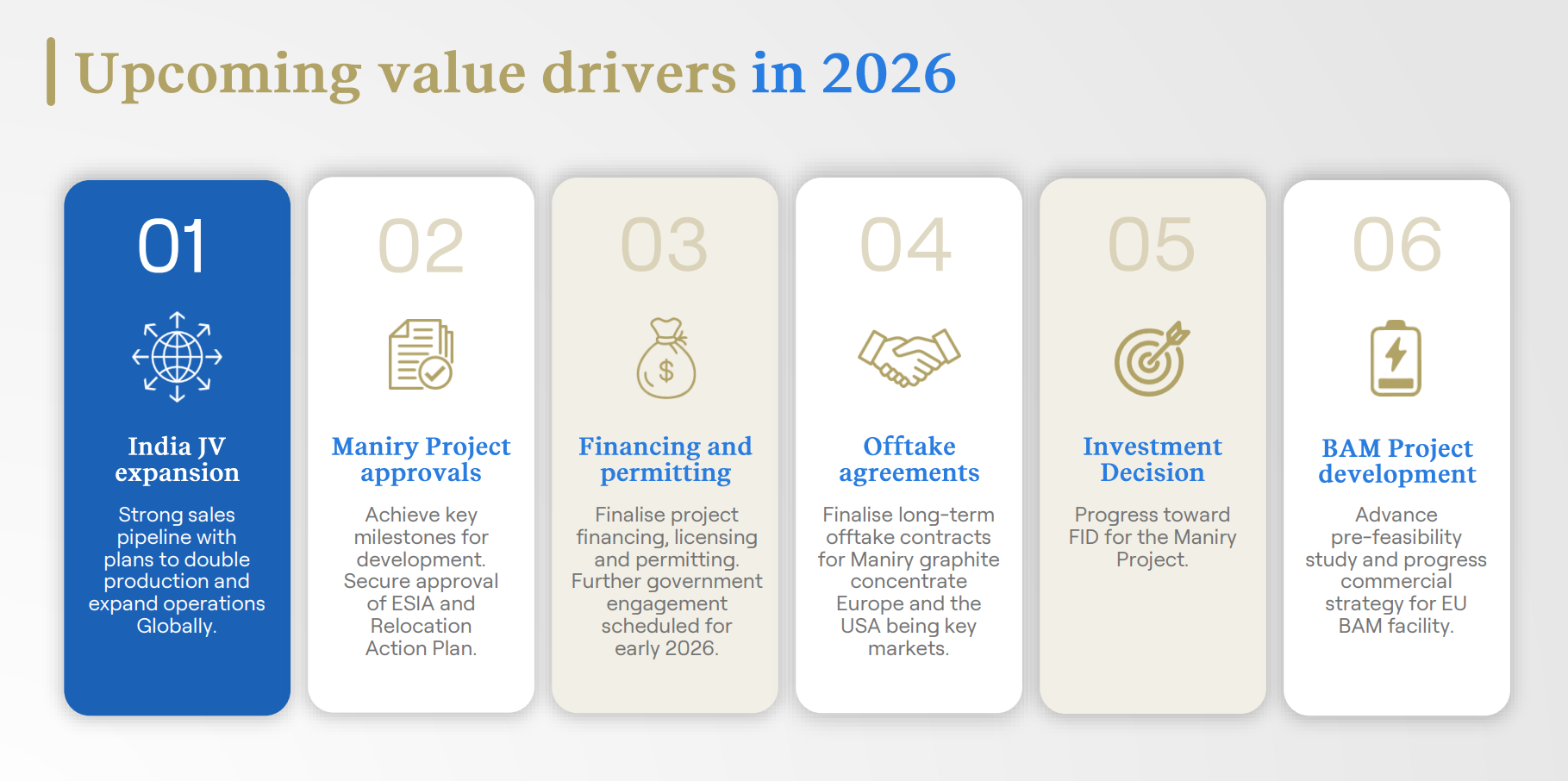

Upcoming Catalysts

Every portfolio addition has to clear the same bar for us: a potential steady stream of news to keep the momentum going. EVG clears it comfortably.

And the next twelve months are loaded with potential share price catalysts:

Maniry mining permit issued in Madagascar

€3 million EU grant unlocked after the permit lands

Stage 2 commissioning at the Panthera JV, lifting production and margins

Confirmation sampling at Carp to verify the 2024 surface results

Drill permitting at Carp ahead of maiden drilling

Maiden drill program at Carp later in the year

Section 232 critical minerals trade decision (covering both graphite and fluorspar), deadline 13 July 2026

Further US sales orders through Panthera as the order book fills up

That’s the beauty of EVG. The company isn’t reliant on one asset or one commodity to generate news flow. Three legs, three jurisdictions, three independent catalyst paths.

Every couple of weeks should bring a discrete news event capable of moving a 3.7-cent share price.

Risks

As always, none of this is risk-free.

Madagascar permits have come close to issuance before, and timelines in-country can slip. The Mines Ministry has done the technical work and the political backdrop is supportive, but until the paperwork is signed, it isn't signed.

On the fluorspar side, Mongolian production has been ramping fast to fill gaps left by Chinese supply tightening. The flip side is that US-produced fluorspar typically commands a premium to Mongolian or Mexican material, and Washington has made it clear it wants domestic supply specifically.

Carp is also still option-stage. The deferred payments and exploration commitments stretch out over three to four years, and the option only converts to full ownership once those milestones are hit.

Surface samples are not drill results. Carp still has to be drilled and tested before the bigger numbers in this article come into reach. That's the work EVG has just started.

The Bottom Line

For 35 years, the West outsourced its critical minerals problem to China. It worked, right up until it didn’t.

The country that supplied the world’s fluorspar, processed the world’s graphite, and the country every Western government is now trying to detach from, is all the same country.

Washington has spent two years and a stack of legislation and Trump Truth Social posts trying to unwind it. Brussels has stamped graphite projects as strategically essential. Canberra has written both fluorspar and graphite into the national reserve.

Underneath all of that policy, somebody has to actually own the mines, run the plants, and ship the product.

EVG owns a graphite project in Madagascar with Europe behind it, a processing plant in India already shipping into the US tax credit that exists for exactly this reason, and a fluorspar asset in Nevada in the shape of the one the Pentagon just funded.

From here it’s the company’s job to deliver.