The Black Book: What Australia’s Stock Brokers Are Backing in 2026

We sat down with some of Australia's best stock brokers and got the inside word on their highest conviction pick of 2026.

Every year we do the hard yards. Last time, we sifted through more than 500 ASX small-caps under $20 million and landed on our own Top 10 small-caps for 2026, one of our most-read pieces to date.

That process meant digging through announcements, balance sheets, drill plans, clinical timelines and management track records until we were confident enough to put our name next to ten companies.

This time, we’ve flipped it.

Instead of asking ourselves which stocks we’d back for 2026, we picked up the phone and asked the people who move capital for a living. Brokers. Advisers. Investor relations firms. The ones who see the placements before they’re public. The ones who sit in the room when deals are structured. The ones who know which boards are sharp and which stories don’t stack up.

We worked the phones. We had the coffees. We chased the follow-ups. Some didn’t reply. Some were happy to go on the record. Others said they’d give us their best idea for 2026, but only if we kept their name out of it. Fair enough.

What we asked for was simple: one stock you believe in for 2026. Not what’s popular. Not what’s liquid. Not what’s easy to sell to retail. Your highest conviction pick.

Size didn’t matter. Sector didn’t matter. We just wanted to know what the so-called smart money is backing as we head deeper into 2026.

None of these are guarantees. Some of them will go sideways. A few might go backwards. That’s investing.

We’ve done the legwork, and now we’re handing it over to you.

Here’s what the pros are backing for 2026, in their own words.

Matt Parker - Euroz Hartleys

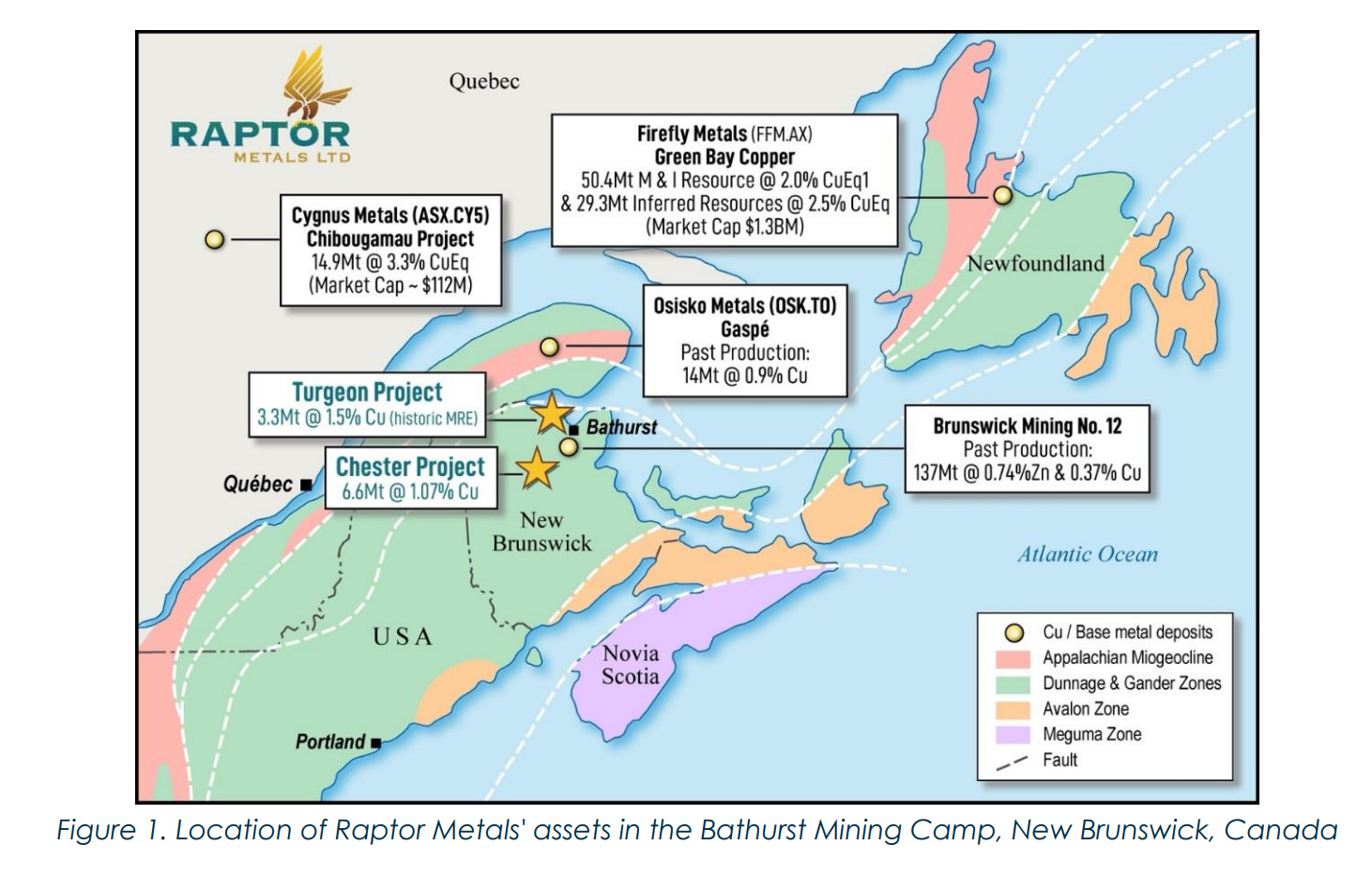

My pick of the year: Raptor Metals (ASX:RAP)

Share price: 5.6c

Company valuation: $23 million

Key assets: New Brunswick, Canada. Advanced exploration: The Chester and Turgeon projects have a combined total resource of ~10Mt at ~1.2% Cu. The initial diamond drilling program at the Chester Project (6.68Mt at 1.1% Cu) is currently testing 1.5km of strike for multiple stacked copper feeder zones, open along strike and at depth.

Why I Like it:

Stable Jurisdiction: Located in New Brunswick, Canada within the Bathurst Mining Camp which has a history of large scale high grade VMS deposits with existing infrastructure present.

Peer Comps: Include Firefly Metals (FFM) and Cygnus Metals (CY5). FFM has been the benchmark of copper plays in the area, New Brunswick is the next province south from Newfoundland (FFM location) with similar geology. FFM has a current market cap of $1.5b with a total resource of ~80mt at 2.2% CuEq. CY5 has a current market cap of $200m with a total resource of 15mt at 3.5% CuEq.

Existing Resource Drill Ready: 2000m diamond drilling program at the Chester Project ongoing, targeting a massive sulphide area from surface, resource infill drilling and deeper met holes with excellent regional potential and geophysical targets generated. Once completed the rig will move to the Turgeon Project.

Matt Parker, Private Wealth Adviser, Euroz Hartleys:

”Copper remains a key pick for 2026 from fund managers, brokers and industry leaders with persisting macro tailwinds largely driven by a supply deficit and surging demand from the AI and green energy sectors.

The spot price continues to trade at all-time highs ( ~US$13K p/t) during a raging commodities bull market. RAP provides portfolios with advanced junior exploration exposure to copper (and silver credits) within a historic proven VMS production area, trading at a fraction of the valuation of peer comps within the region. The company is well capitalised to complete initial diamond drill programs at Chester and Turgeon with the aim of increasing their total current resource.”

Nick Kelso - Rats Rant - Sanlam

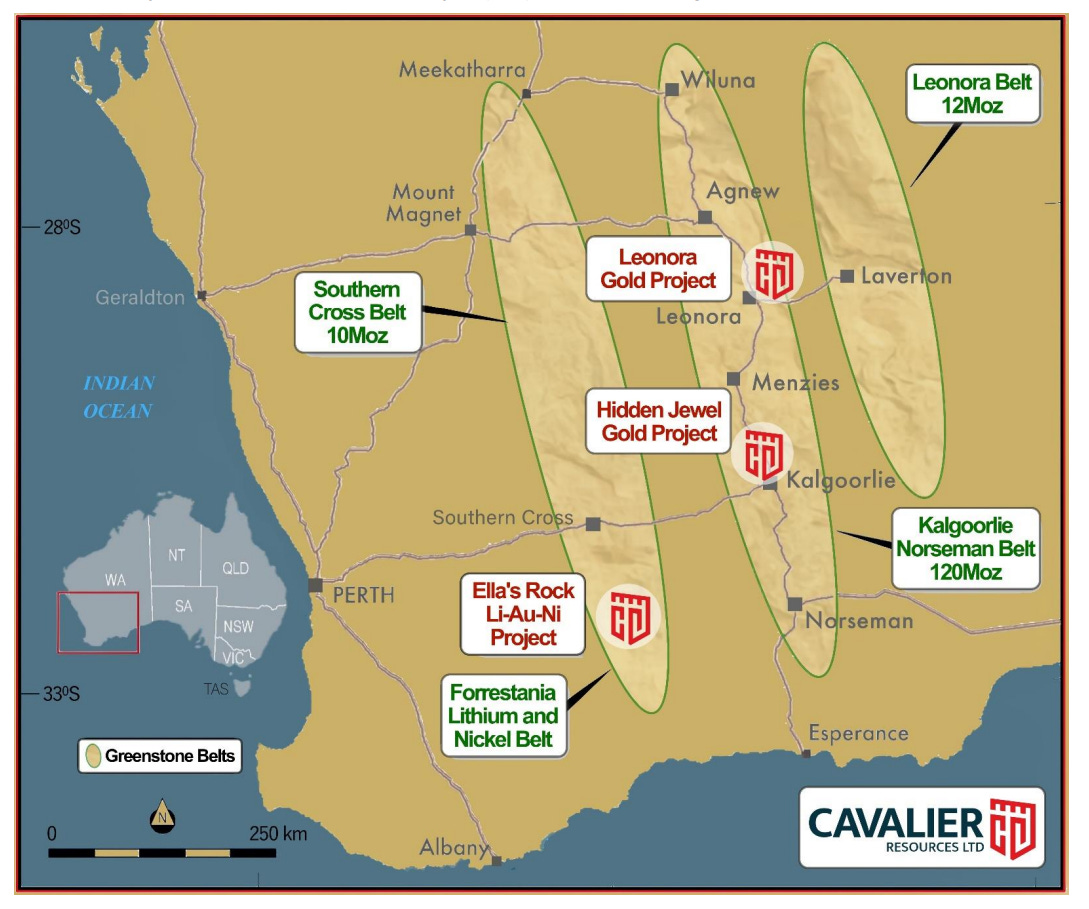

My pick of the year: Cavalier Resources (ASX:CVR)

Share price: 40c

Company valuation: $28 million

Key assets: Crawford Gold Project located in Leonora, WA. Crawford hosts a high-grade, near-surface gold resource with a total JORC (2012) mineral resource estimate of 117.8Koz @ 1.7 g/t Au. CVR has already completed key technical studies, environmental surveys and has the all-important native title approvals done, providing the upcoming heritage survey gets the green light – then it’s mining time.

Why I Like it:

Provides investors exposure to a near-term producing gold company with a valuation of $28m and just 71m shares on issue (top 20 own 60% of paper on issue). The plan is to mine stage one at Crawford, while at the same time drilling to extend the current resource – the idea being that once stage one is mined in an estimated 18 months’ time – stage 2 of the project which will preferably be at the Miranda prospect, where another 30,000+/- ounces lay in waiting.

Crawford’s economics stack up very well: Stage 1 capital costs are extremely low at $9.8m and sits in the lowest quartile C1 (Net Direct Cash Costs) AISC (all-in sustaining costs) of A$1,574/oz; C3 (Fully Allocated Costs) AISC of A$1,793/oz. With gold at over $6,500 an ounce it provides an attractive margin. Gross revenue at Crawford alone is A$103.6M.

The boss Dan Tuffin is a mining engineer by trade, he’s been in the region all his life so knows the ground well and although the initial deposit isn’t massive, it will spit out plenty of cash for CVR shareholders with a very competitive AISC. Expect plenty of news flow throughout 2026 with construction and production at Crawford along with extensional drilling results which will hopefully help increase overall resource and life of project.

Nick Kelso, Wealth Management Advisor at Sanlam:

“Tight share structure, near term producer, under the radar type stock that if all goes to plan may well be paying out dividends in the not-too-distant future.”

Anonymous Broker

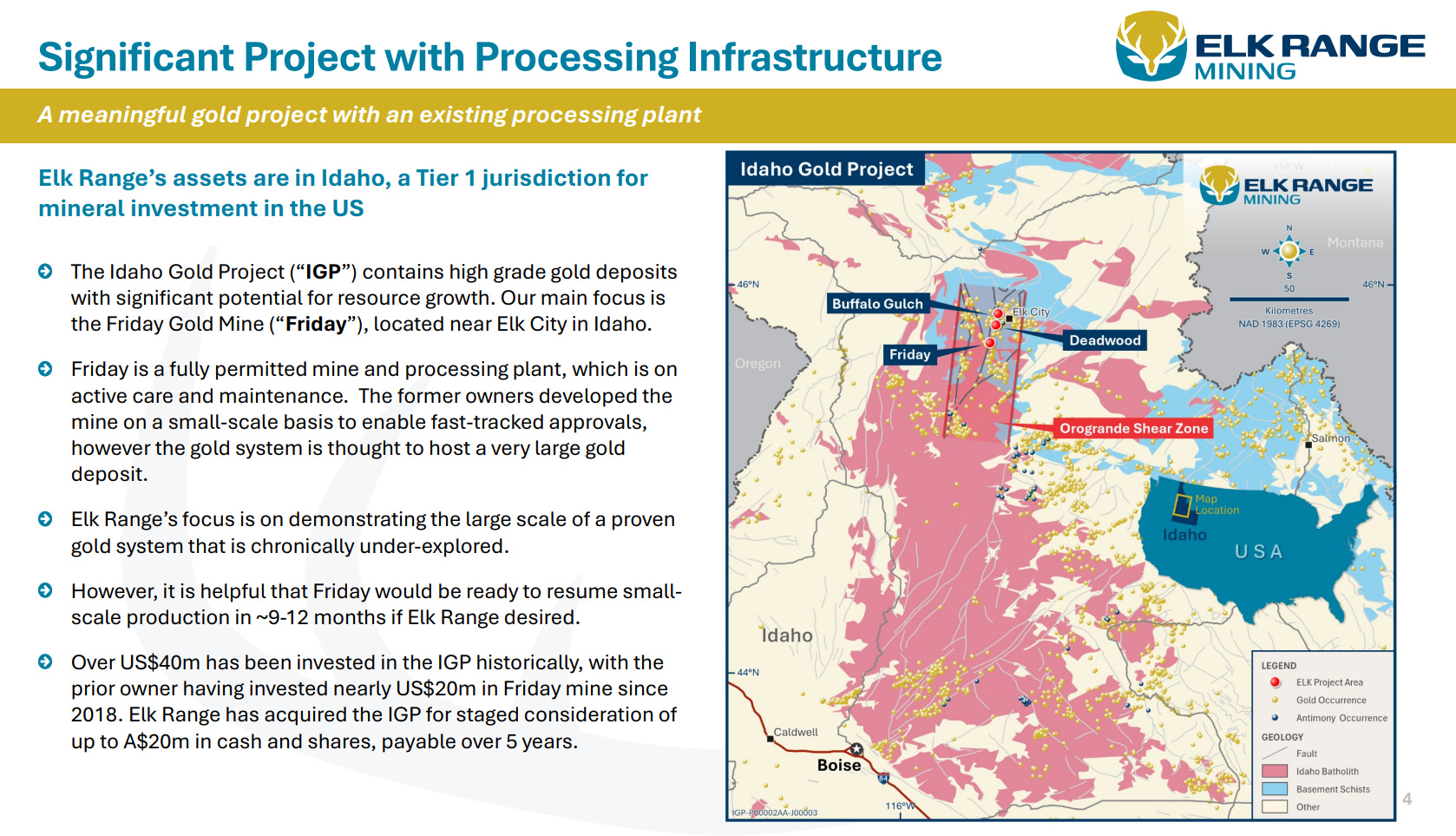

My pick of the year: Elk Range Mining (Not yet listed, expected April 2026)

Share price on listing: 20c

Company valuation on listing: $20 million

Key Assets: Elk Range Mining controls the Idaho Gold Project in Idaho, USA, centred on the Friday underground gold mine, the Orogrande processing plant and the Buffalo Gulch and Deadwood deposits along the Orogrande Shear Zone. The project hosts a combined historical foreign resource of 343,000 ounces of gold, including 144,000 ounces at 5.91g/t Au at Friday. Friday is a fully permitted underground mine with a 135tpd processing plant now on care and maintenance, placing it at an advanced exploration to restart-ready stage, while Buffalo Gulch and Deadwood are earlier-stage exploration assets with defined historical resources.

Why I Like it:

Substantial sunk infrastructure capital – more than US$40 million invested historically across the project, including an estimated ~US$20 million replacement value for the processing plant alone.

High-grade core with broader system scale – Friday hosts 144,000oz at 5.91g/t Au historically, within a larger 343,000oz district position that remains open and under-explored.

Fully permitted mine in a Tier 1 US jurisdiction – existing approvals, underground development and plant infrastructure materially reduce the pathway to restarting production.

Anonymous broker quote:

“ELK is an advanced-stage gold project in a Tier 1 US jurisdiction with 144,000 high-grade ounces already defined at 5.91g/t Au at Friday. The project has a fully permitted underground mine and processing plant in place, and more than US$40 million historically invested. That gives it both scale upside and a far shorter pathway back to production than a typical early-stage explorer.”

Robert Williams - FCR Relations

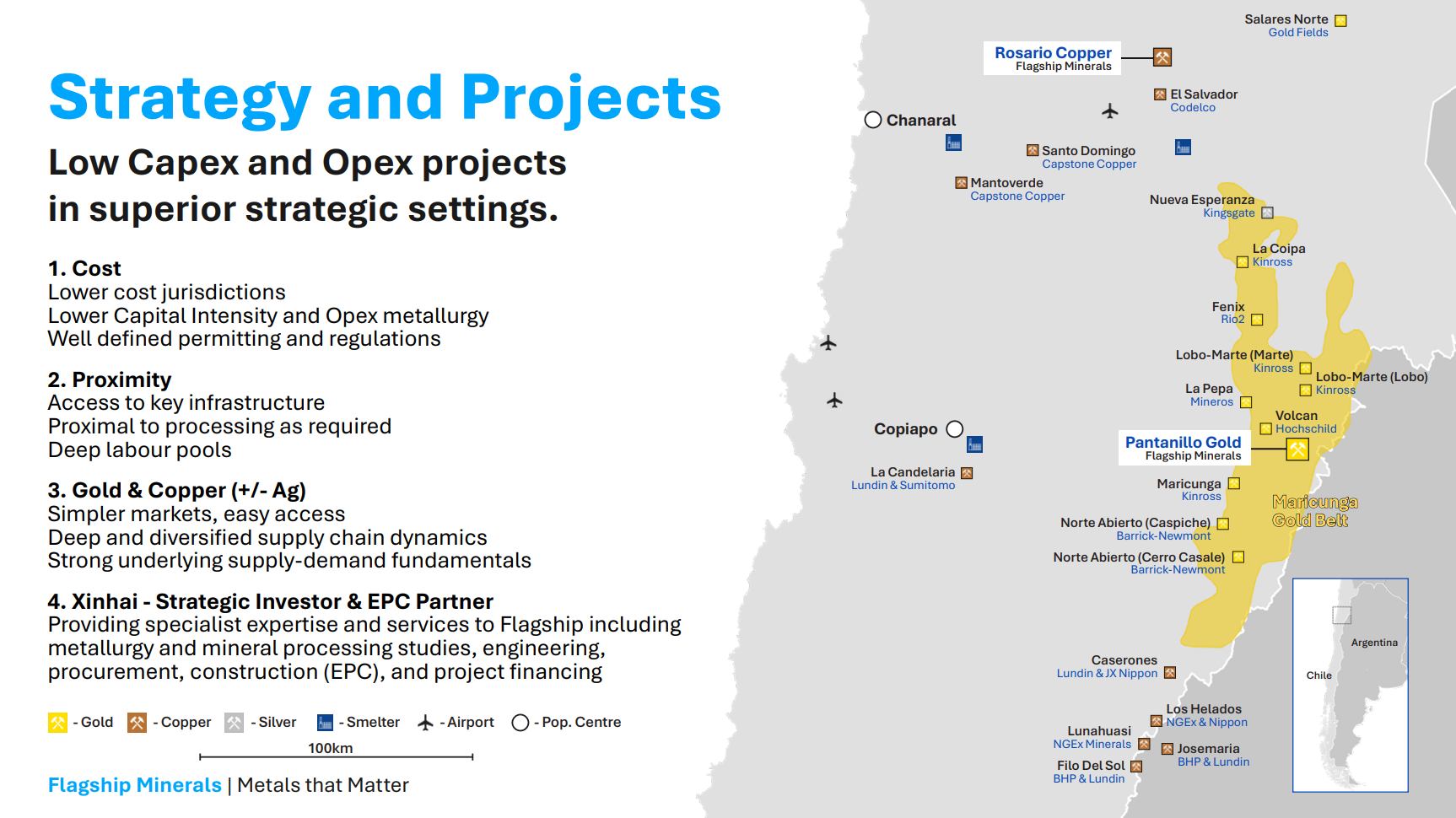

My pick of the year: Flagship Minerals Limited (ASX:FLG)

Share price: 26.5c

Company valuation: $83 million

Key Assets: The Pantanillo Gold Project – oxide gold system with 1.05 Moz Au (historic NI 43-101); moving toward JORC MRE in Q1 2026. It is a gold project with copper upside in the Maricunga Gold Belt, Chile. Pantanillo is currently an advanced exploration project with baseline EIA studies underway and major metallurgical testing program in progress

Why I Like it:

Strategic backing from China-based EPC and processing group Xinhai, now a cornerstone shareholder and board participant.

Positioned in a Tier-1 gold district surrounded by 60–100Moz of regional gold resources (including Rio2, Hochschild, Newmont/Barrick).

Clear and accelerated development pathway: JORC MRE pending, strong technical team, ESG momentum, and near-term drill targets.

Robert Williams, Head of IR at FCR:

“We see Flagship as one of the best-positioned gold development stories in Chile - high-grade oxide gold in a proven jurisdiction, now backed by strategic capital and capability from Asia. The team has a clear plan, and investors are starting to take notice.”

Executive Director - GBA Capital

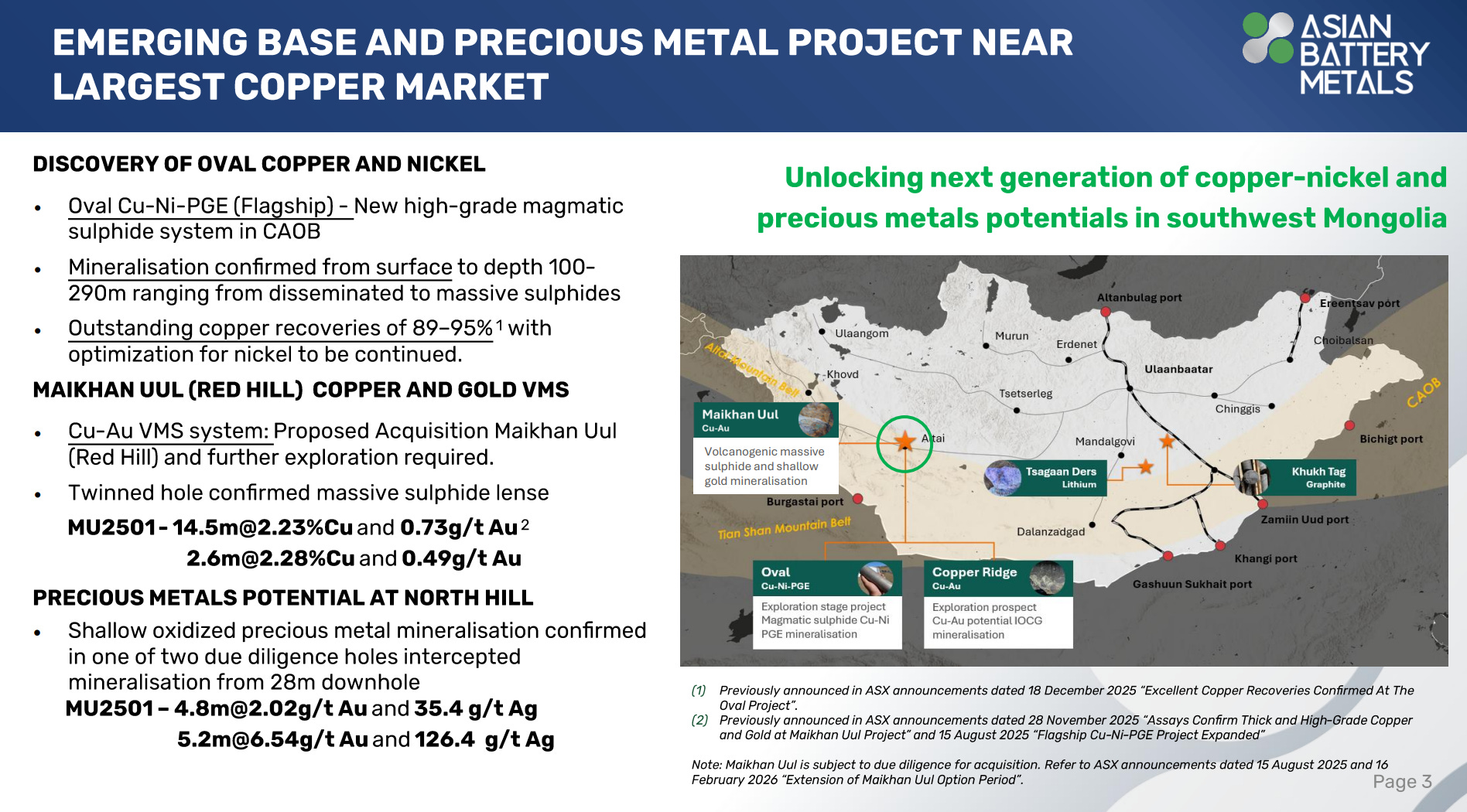

My pick of the year: Asian Battery Metals (ASX:AZ9)

Share price: 2.8c

Company valuation: $22 million

Key assets: AZ9 is advancing the high-grade Oval copper–nickel discovery in southwest Mongolia, where drilling has confirmed mostly continuous mineralisation over ~880m of strike from surface to ~290m depth. Massive sulphide hits include grades up to 6.08% Cu and 3.19% Ni, with copper recoveries of ~95%.

Beyond Oval, AZ9 is progressing the Maikhan Uul (Red Hill) Cu–Au VMS project, which has returned 14.5m @ 2.23% Cu and 0.73g/t Au, along with shallow gold mineralisation at North Hill across a 600m by 100m anomalous trend.

Why I Like it:

Genuine high-grade Cu-Ni discovery: Provides exposure to a genuine high-grade Cu–Ni discovery at a time when copper supply deficits are front of mind globally. AZ9 is the only ASX-listed junior with a new high-grade copper-nickel discovery in Mongolia, sitting on China’s doorstep, the world’s largest consumer of copper and battery metals.

Maikhan Uul adds both copper-gold VMS and shallow high grade gold, with confirmed massive sulphide for the copper, including 14.5m @ 2.23% Cu and 0.73g/t Au, as well as highly encouraging initial gold hits of >6g/t Au from near surface.

Early validation is already there, alongside emerging cluster-style regional potential. Metallurgy at Oval has delivered copper recoveries of 89–95% with a relatively simple flow sheet, and the system is showing camp-scale potential with multiple magnetic targets beyond the initial discovery. Oval is also the first magmatic sulphide discovery of its type in this region, a style of deposit often found in clusters, with scout drilling providing early encouragement of additional nearby potential planned for testing in 2026. A maiden JORC resource in 2026 would be a clear valuation catalyst.

Executive Director at GBA Capital:

“Everyone loves a comeback story and AZ9 is poised for a re-rate in 2026 with drilling in

March focused on shallow, high grade gold in addition to copper in massive sulphide at RedHill, which is on a granted mining lease. Combined with the already discovered Cu-Ni resource at Oval, only 8kms away, it won’t take much to achieve a maiden resource that crosses the commercial threshold for a copper development.”

Anonymous Broker

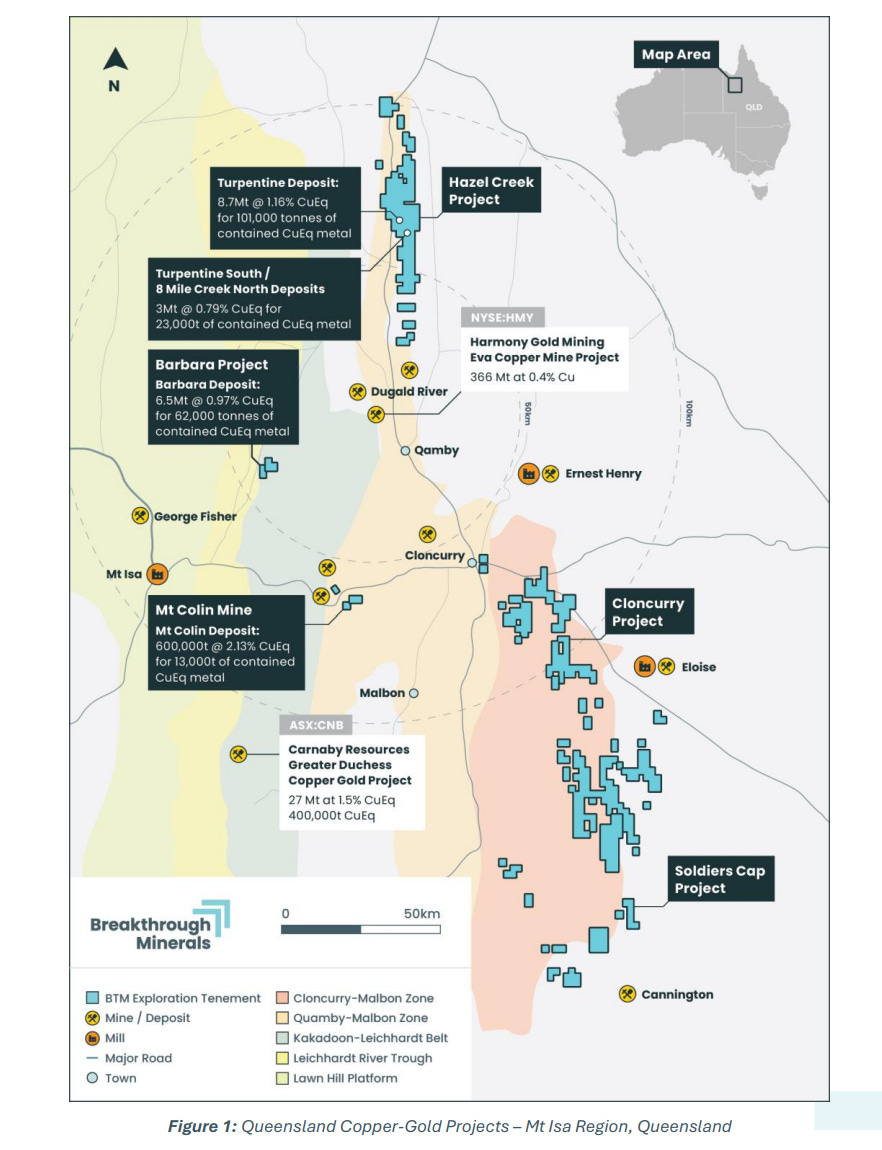

My pick of the year: Breakthrough Minerals Ltd (ASX:BTM)

Share price: 25c

Company valuation: $33 million

Key Assets: Copper/Gold, Mt Isa copper region, Queensland, brownfields exploration

Why I Like it:

Undervalued – Substantial Global JORC (2012) Minerals Resource, 18.8Mt @1.07% CuEq2 for 200Kt of CuEq

Significant resource and exploration upside - numerous untested copper and gold targets across four projects

Strategically located close to third party processing infrastructure

Mt Isa (Glencore)

Eva (Harmony Gold)

Eloise (AIC Mines)

Stuart Veron - Rats Rant - Sanlam

My other pick of the year: Pivotal Metals (ASX:PVT)

Share price: 1.9c

Company valuation: $26 million

Key assets: Flagship “Horden Lake” project which has a current resource of 37mt @ 1.1% Cu eq, almost all open pittable and open in multiple directions with excluded drilling and geophysics supporting substantial resource growth potential. The company will also shortly be drilling its high-grade “Belleterre” exploration projects in Quebec, where prior exploration identified bonanza grades of copper, PGMs and gold yet there has been limited regional exploration to delineate scale potential of the district.

Why I Like it:

Value underwritten by a large, derisked copper resource with expansion upside. Horden Lake contains >400kt CuEq, including ~230kt Cu, ~200koz Au and ~200koz PGMs. Metallurgy is well understood, the deposit is predominantly open-pittable, road-accessible, and located in a Tier-1 jurisdiction with ultra-low-cost power (99% hydro). These factors materially reduce development risk and capex intensity.

High-torque exploration at Belleterre. Drilling is imminent across multiple Belleterre targets, which has the potential to generate extremely exciting drill hits based on what was previously drilled - historic results include 21.1m @ 2.5% Cu, 1.7% Ni and 2.8 g/t 3PGE (Midrim) and 21m @ 2.1% Cu, 2.0% Ni and 2.1 g/t 3PGE (Alotta). Focus has been narrow around existing outcrop, so the district remains largely unexplored - any success in demonstrating scale could be a major re-rating catalyst.

Managing director Ivan Fairhall is an engineer with a private equity background focused on identifying copper projects capable of becoming mines. He previously backed Marimaca Copper at a ~$5m valuation, now a ~$1.4bn company nearing construction. I see parallels between Horden Lake and other advanced copper assets (eg NWC’s Antler) that have strategic value the market has historically under-appreciated - particularly in Tier-1 jurisdictions like Canada.

Stuart Veron, Wealth Management Advisor at Sanlam:

“I could be wrong but there wouldn’t be many other listed ASX companies with a resource the size of the above and a market cap the size of the above. The asset(s) are in Canada not Africa or North Korea as the market cap would suggest, with exploration upside at both projects and over 4,000m of drilling planned for 2026 (all funded). Given asset quality and low market cap, the upside opportunity on a wide range of catalysts is very asymmetric.”

Joel Ridley - Ora Capital

My pick of the year: Trivarx (ASX:TRI)

Share price: 2.1c

Company valuation: $25 million

Key assets: TRI offers exposure to a meaningful CNS oncology platform, but at a valuation more typical of an early diagnostic play. Its lead asset, Stabl-Im, is a non-invasive molecular imaging technology that uses stable isotopes visible on standard MRI machines, initially targeting brain metastases. The program is Phase I–ready and has shown early signs of direct anti-tumour activity, meaning it may sit somewhere between a diagnostic tool and a therapeutic asset rather than being limited to imaging alone.

Why I Like it

This dual diagnostic + therapeutic optionality materially expands both valuation upside and strategic relevance

A CNS oncology platform masquerading as a diagnostic to get into humans faster - that is a very investable narrative.

From a valuation perspective: High unmet need, Existing MRI workflow → zero hardware friction, Repeat-scan use case (monitoring)

Joel Ridley, Managing Director, Ora Capital:

“The size of the prize is enormous with a Telix (TLX - $4B MC) type trajectory into commercialisation. Even base case you could argue a Phase 1 Brain Cancer Diagnostic / Oncology platform would have a comparable implied EV of $250 - $500m. The real benefit in the speed and little capital required to progress through P1 trials given the isotope safety profile (Heavy Water).”

Anonymous Broker

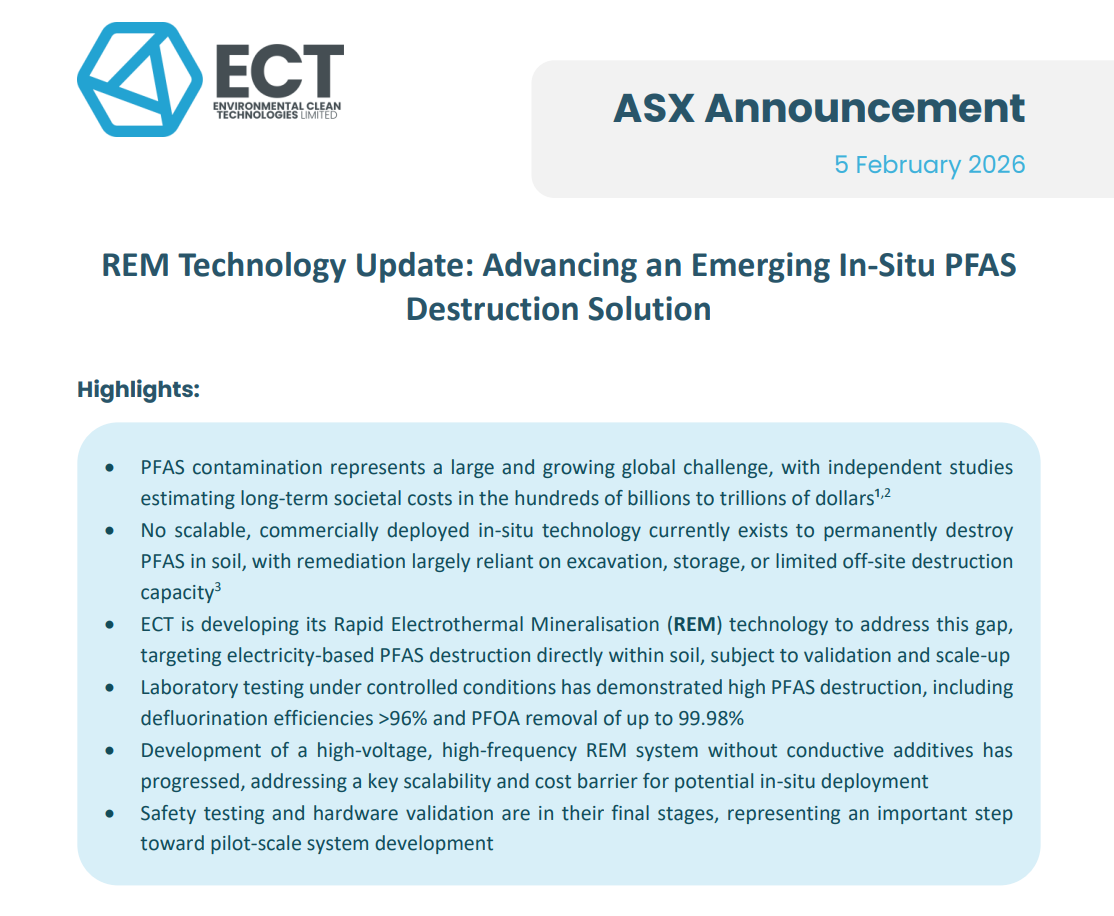

My pick of the year: Environmental Clean Technologies Limited (ASX:ECT)

Share price: 11.5c

Company valuation: $48 million

Key asset: ECT recently acquired Terrajoule Pty Ltd, which holds a licence from Rice University in Houston to develop and commercialise Rice’s proprietary flash joule heating (FJH) technology for the purposes of remediating soil which has been contaminated by PFAS. PFAS are commonly known as “forever chemicals”, and are long-lasting, hazardous chemicals which have historically been used in a wide range of products but have now been found to pose a significant health and environmental risk. PFAS remediation is a large and growing market and is attracting increased interest largely due to numerous successful lawsuits which have been launched by the impacted against large corporations who have been releasing PFAS into the environment for years.

Why I Like it:

Rice and Professor Tour Connection: The FJH technology was invented by Professor James Tour and his team at Rice University in Houston. A number of Professor Tour’s technologies have been successfully spun into companies for commercial development, including market darlings Weebit Nano Limited (ASX:WBT – capped at $968M and focused on developing a semiconductor technology) and Metallium Limited (ASX:MTM – capped at ~$629M and also developing the FJH technology but for the purposes of extracting rare earth elements from waste material). ECT’s FJH technology is the same base technology being developed by MTM (except ECT has licenced it for the purposes of PFAS remediation).

World Renowned Advisory Board: In connection with its acquisition of the licence from Rice, ECT has established a world renowned advisory board comprised of:

Mr Robert Bilott - Partner at US law firm Taft Stettinius and Hollister LLP. He specialises in environmental law and is widely regarded as a subject matter expert in PFAS.

Professor James Tour – inventor of the FJH technology and a globally recognised expert in chemistry, nanotechnology and advanced materials.

Mr Lewis Utting – over 20 years’ experience in the chemical industry, water treatment and mineral processing sectors and was a former BASF minerals processing and speciality chemicals executive.

Mr Hirokazu Minami – Highly respected leader in Japan’s energy and industrial sectors. Mr Minami has a proven track record of introducing advanced technologies, scaling complex businesses, and leading market entry and business development for both domestic and international companies.

Renewed Corporate and M&A Strategy: Prior to its acquisition of Terrajoule in December 2025, the Company was principally focused on the development of its proprietary COLDry technology. The board has been refreshed over the past 12 months, and as part of the Terrajoule acquisition, ECT signalled an intention to implement a revised strategy aimed at building a diversified portfolio of high impact and disruptive technologies through organic and acquisitions growth, with Terrajoule being just the first part of this strategy.

Michael Zollo - AE Advisors

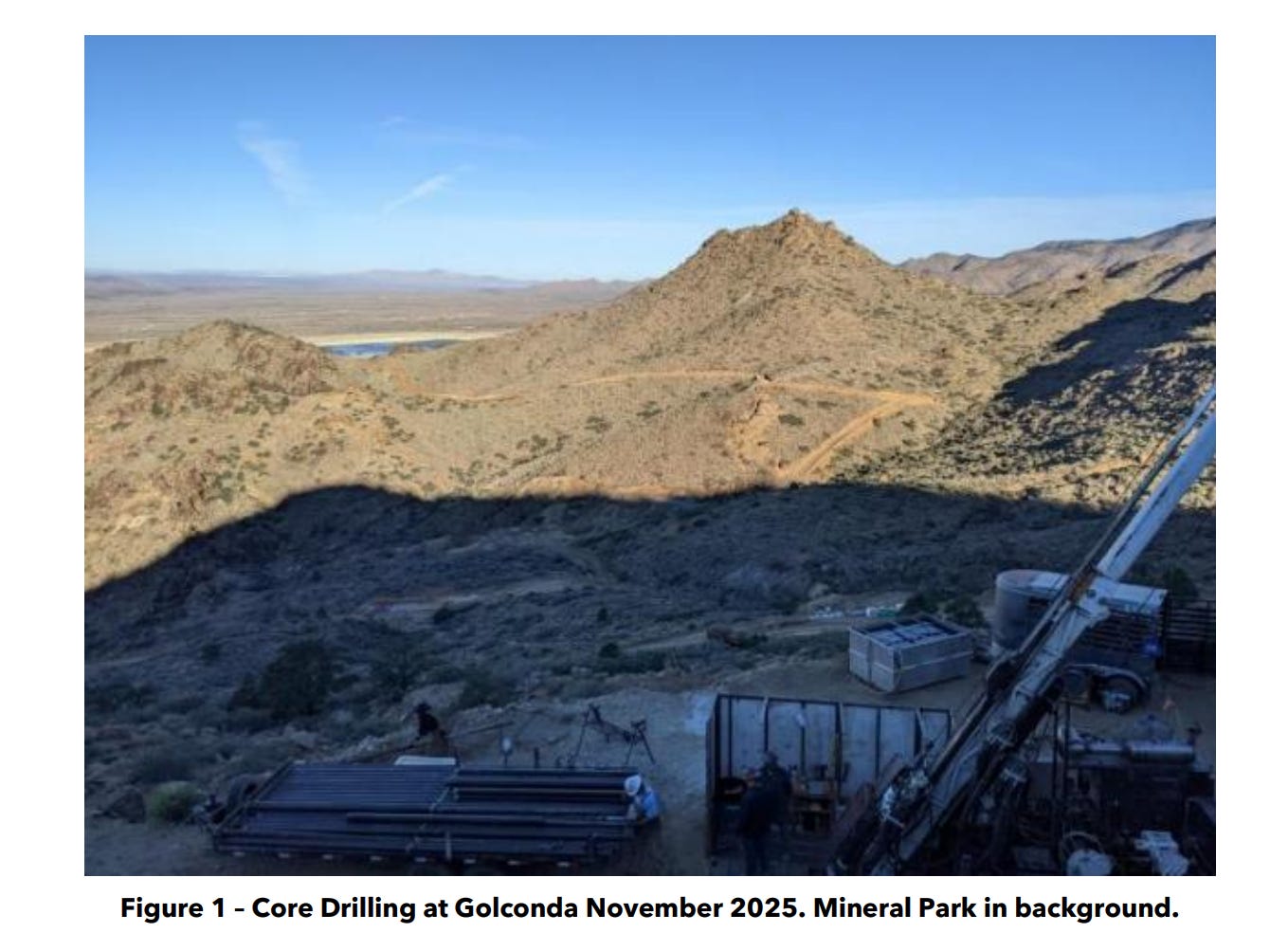

My pick of the year: G50 Corp (ASX:G50)

Share price: 92c

Company valuation: $194 million

Key assets: Exploring for gold, silver, gallium in Nevada

Why I Like it:

Timing is right - The Trump administration has heavily backed the US critical metal industry, creating a large fund for the stockpiling of CMs as well as providing loans, funding and fast tracking approvals for projects which show they can supply CMs within the US. Additionally, precious metals have enjoyed a blistering rally in the past 12 months and will continue to be well bid in the next 12 months. G50 sits perfectly within both of these thematics.

G50 has done what few other critical metals plays have done. They have pursued metallurgical understanding and clarity ahead of a resource. This is because internally, management is confident the resource will be there (currently drilling Golconda and have completed two prior rounds of drilling). Now, when they publish a gallium resource, the market will also have confirmation that they can actually recover the gallium economically.

High Quality Management - G50 Management have all been involved with US exploration for many years. There has been a wave of ASX companies acquiring US-based projects lately, but many have never stepped foot in the US. G50 IPO’d in 2021 with these current assets. One of the NEDs, Bernard Rowe, is also the MD of Ioneer (ASX:INR) which has an advanced US-based project. The team has a deep understanding of operating in the US and has experience in the development of assets toward production.

Michael Zollo, Director at AE Advisors:

“G50 is a classic case of right place, right time, right theme. The US Secretary of Commerce, Howard Lutnick, was recently quoted as saying that his administration wants to see 40% of all semiconductors used in the USA, made in the USA. In the same clip, he goes on to say that you can’t make semiconductors without gallium.

We believe that G50 has the USA’s most advanced gallium project and as such, will shortly come onto the US government’s radar. With large US tech companies recently investing into mining companies for the first time ever (Apple into Mountain Pass, other similar deals likely), we believe that G50 is perfectly placed to get non-dilutive funding from either the US Govt or a large corporate partner at some point this year.”

Paul Hart - Canary Capital

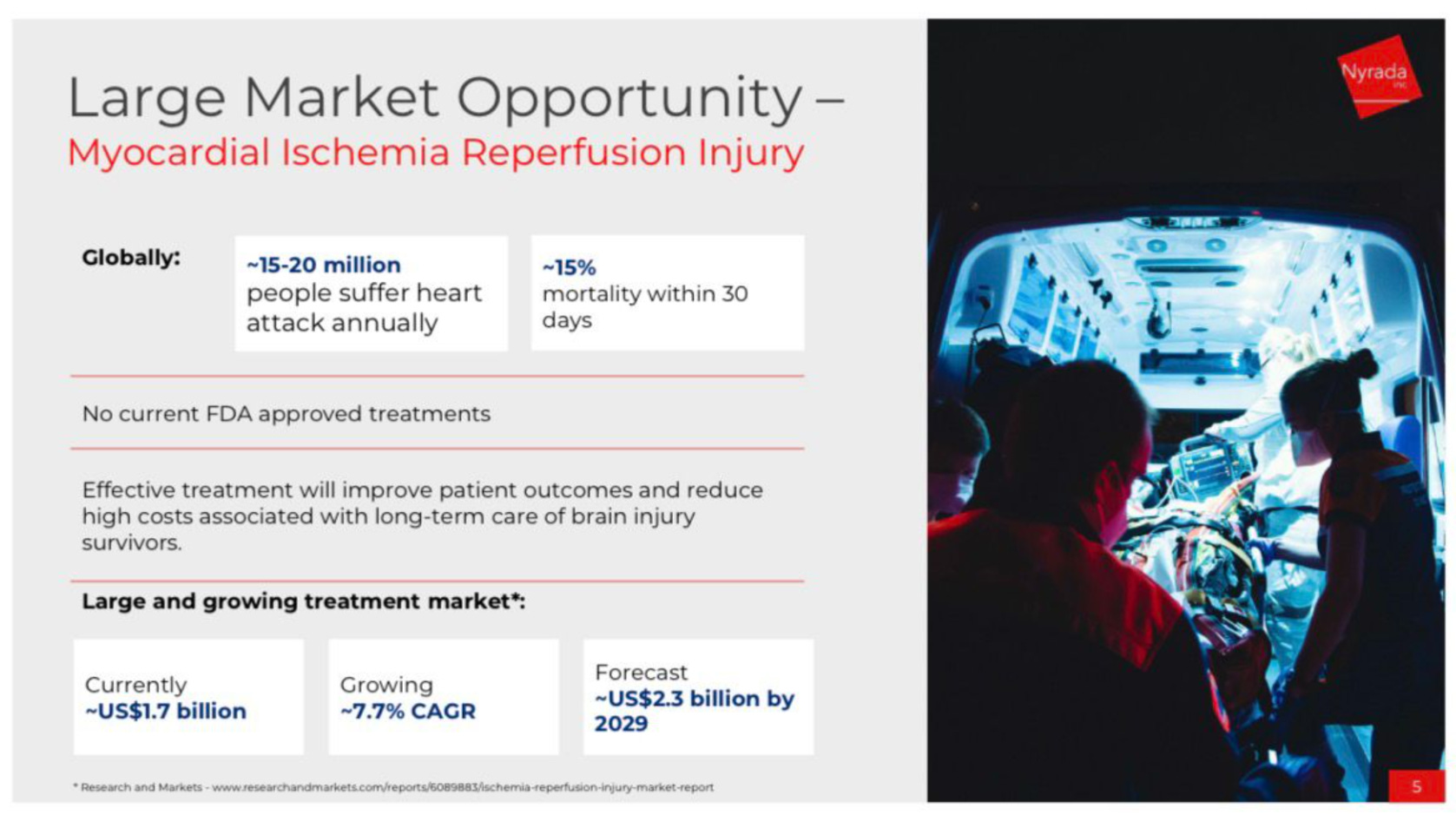

My pick of the year: Nyrada Inc. (ASX:NYR)

Share price: 60.5c

Company valuation: $140m

Key assets: Biotech entering Phase IIa (Q1, 2026) to provide protection to the heart during the insertion of stents to clear blocked arteries following a heart attack (ischemic reperfusion injury).

Why I Like it

Proven safety from Phase I clinical trial in humans;

Mechanism of action validated in Boehringer Ingelheim’s phase II human trial in chronic kidney disease;

This is a platform play which targets many diseases, each with very large market potential

Paul Hart, Executive Director, Canary Capital:

“The science behind Nyrada’s drug, Xolatryp, is already validated in kidney disease through Boehringer Ingelheim’s Phase II study into chronic kidney disease in humans and cancer through Mayo Clinic studies using human cells in the lab.

Xolatryp is looking like a game-changer for many diseases including heart attack, stroke, kidney injury, protection from organ damage during chemotherapy and an adjunct therapy to help treat many aggressive cancers, because it stops calcium overload into cells at the primary entry point by inhibiting TRPC ion channels 3, 6 and 7.

This dramatically reduces toxicity and the resulting death of healthy cells. The drug is safe as shown by a successful Phase 1 study in humans and the mechanism works. It is a true platform play with many potential indications each with massive potential markets.”

Anonymous Broker

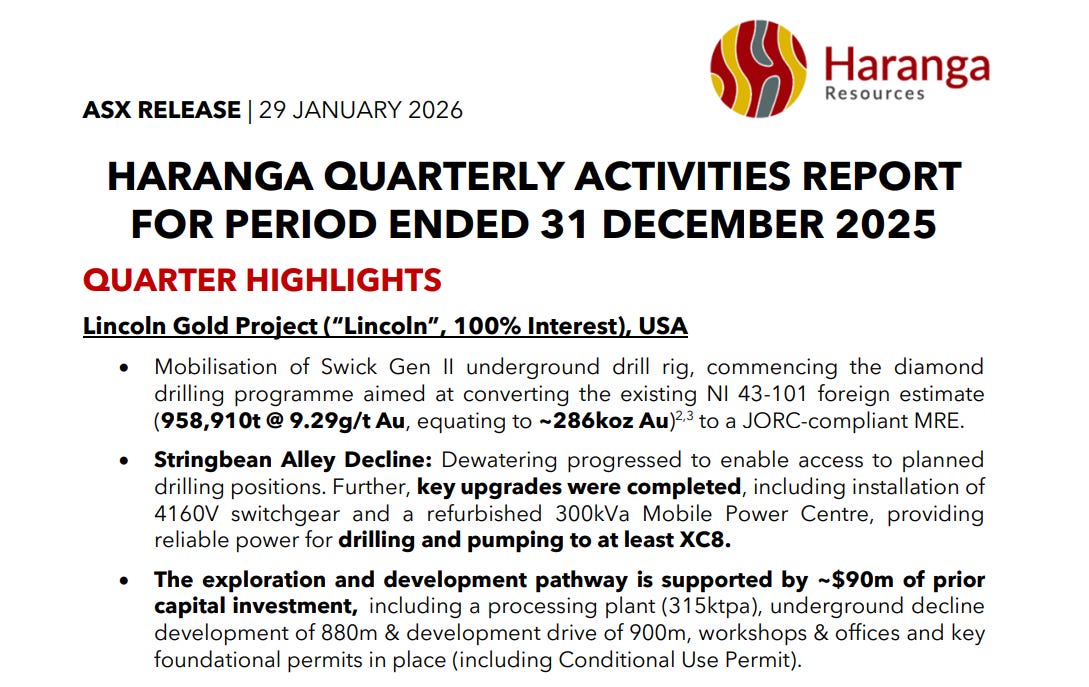

My pick of the year: Haranga Resources (ASX:HAR)

Share price: 13.5c

Company valuation: $62 million

Key asset: Haranga Resources is a gold exploration and development company actively advancing assets across California’s legendary Mother Lode Gold Belt and Senegal’s Kéniéba Inlier. The early stage Lincoln Gold Project in the USA, and the advanced exploration projects Ibel South Gold Project, and the Saraya Uranium Project, both located in Senegal.

Why I Like it:

At Lincoln, Haranga is currently advancing a diamond drilling program aimed at converting the existing non-compliant Lincoln-Comet NI 43-101 foreign estimate (958,910t @ 9.29g/t Au, 4.2 g/t cut-off equating to ~286koz Au) to a JORC-compliant Mineral Resource Estimate.

The exploration and development pathway at Lincoln is supported by ~$90m of prior capital investment, including a processing plant (315ktpa), underground decline development of 880m and development drive of 900m, workshops and offices and key foundational permits for mining (Conditional Use Permit i.e. Mining Licence). The infrastructure in place provides Haranga with the opportunity to fast-track the Project towards production.

At Ibel South two successful Aircore drill programs have led to planning a Phase 3 drill program expected to commence in Q1 CY2026, aimed to target previously identified high grade mineralisation at depth and to test multiple undrilled gold anomalies. To date average hole depths across both Aircore programs was ~30m, with typical deposits in the area known to exist up to depths of a few hundred metres.

Anonymous quote:

“HAR is advancing two highly prospective gold projects in proven gold belts, each with clear pathways to value creation. At Lincoln, the presence of substantial existing infrastructure, permitting and historical resources, provides a significant competitive advantage to early production.

At Ibel South, real exploration upside exists with near-term drilling planned to test known mineralisation at depth and to drill numerous undrilled targets across the existing >5km anomalous corridor.”

Anonymous Broker

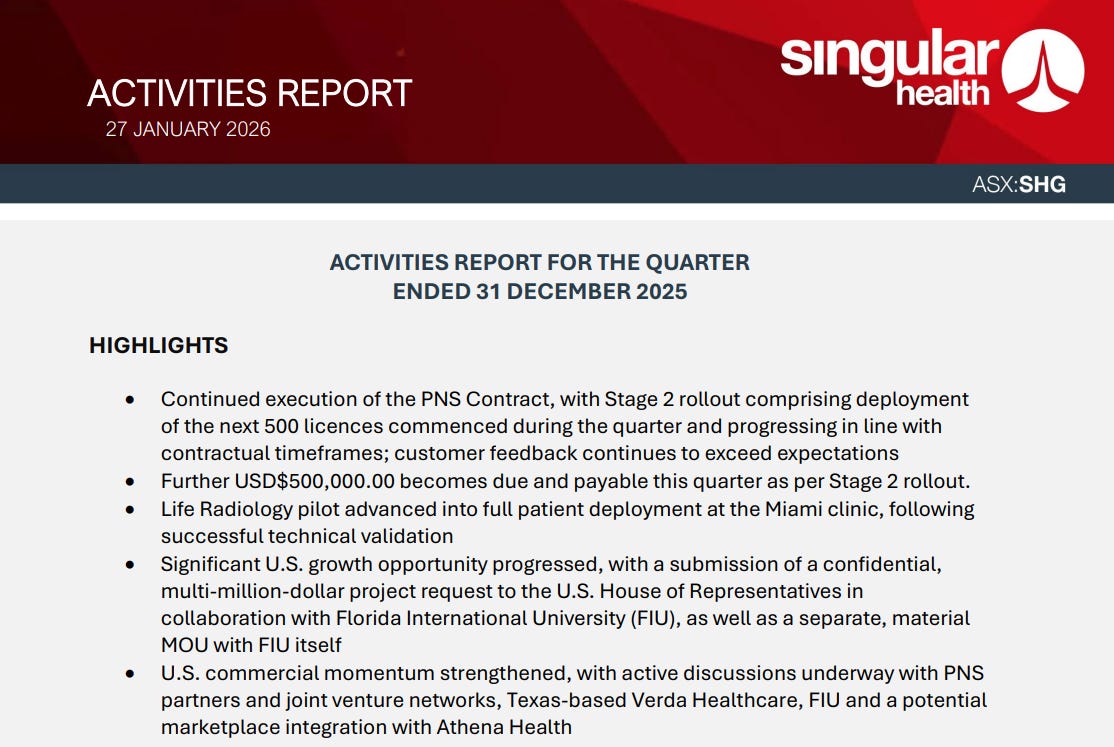

My pick of the year: Singular Health Group (ASX:SHG)

Share price: 26c

Company valuation: $87 million

Key asset: US focused medical imaging SaaS company. Its core platform, 3DICOM™, is FDA cleared and enables the secure sharing and viewing of medical imaging across healthcare networks. SHG’s compression and transfer technology allows these large files to be moved quickly and efficiently, making the solution practical in real clinical settings where time matters.

Why I Like it:

Large, clearly defined addressable market: Duplicate medical imaging is a genuine structural inefficiency in the US healthcare system. It is not a niche issue. It is a multi-billion-dollar cost problem.

Customer-led commercial validation: What I like most here is that this is not technology looking for a problem. PNS saw the platform, recognised it could address a much bigger issue they have, being the cost of duplicate imaging across their network, and engaged SHG in a paid commercial pilot. That tells you the demand is real and financially driven.

Scalable expansion opportunity: If the pilot delivers results, there is a clear pathway to expand across the broader PNS physician network. Beyond that, the model is replicable across other MSOs and healthcare plans.

Anonymous quote:

“What stands out to me is that this is commercially driven from the customer side. When one MSO alone is dealing with roughly US$1.76 billion a year in duplicate imaging costs, the incentive to solve that problem is obvious. If SHG can reduce even a small percentage of that waste, the value proposition becomes very compelling.”

That Was the Inside Look

That’s the lot. Thirteen picks from people who do this for a living, day in, day out.

A few of these names we hadn’t come across before, which is half the point. We spend most of our time in the sub-$20 million end of the market, so getting a look at what brokers and advisers are backing across the full spectrum gave us a few new ones to add to our own watchlists.

We want to thank everyone who picked up the phone, replied to the emails, or sat down for a coffee to share their ideas. Whether you went on the record or preferred to stay anonymous, we appreciate it.

Now comes the fun part. We’ve got our Top 10 picks for 2026, and we’ve got the pros’ picks sitting right next to them. We’ll be checking back later in the year to see how they stack up against each other.

If the pros beat us, we’ll cop it. If we beat them, we won’t be shy about it either.

Until then, good luck out there.

Did anyone mention Chalice?