The Heavy Rare Earth Story Worth Watching

MRD's heavy rare earth project just took its next step. It still trades at a fifth of its closest comparable

The gap between a resource and a producer is where most junior critical mineral stories get stuck. Mount Ridley Mines (ASX: MRD) has spent the past eight weeks moving through that gap.

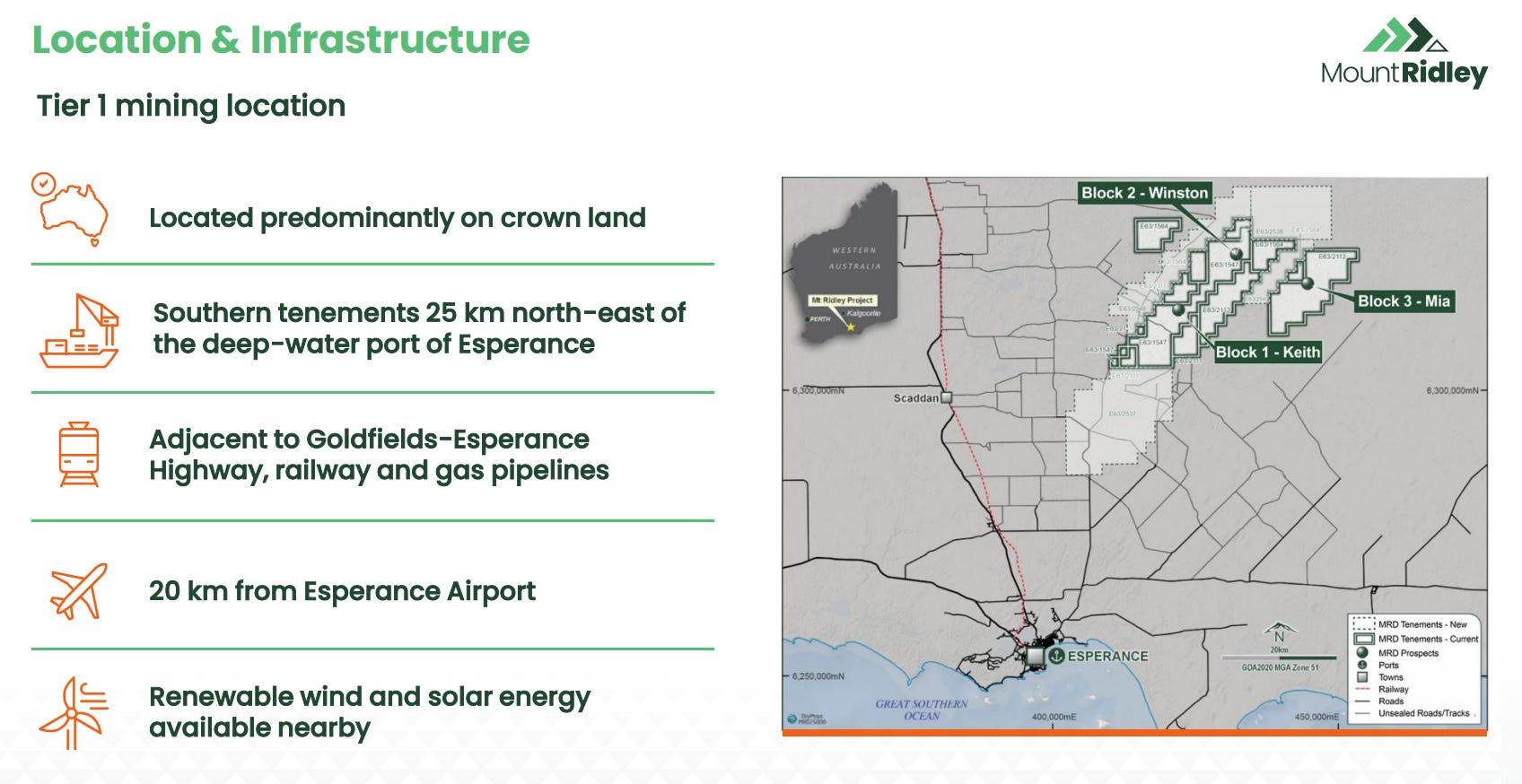

This morning the company kicked off Phase 1 metallurgical testwork at Perth lab Nagrom, on the heavy rare earth, scandium and gallium mineralisation at the Grass Patch project, 25 kilometres north of Esperance in WA.

It’s the first stage of the work that decides whether the rocks at Grass Patch become a mine or a footnote.

Chris Larder is running the program. He’s spent 30 years on WA flowsheets, including spells at Alcoa’s Wagerup gallium plant and Lynas’ Mt Weld rare earth separation facility.

Those are the two WA operations that MRD’s basket could realistically feed into.

We wrote about Larder joining MRD three weeks back. The program kicking off this morning is the one he's been designing since.

MRD trades at 2.7 cents, valuing the company at around $36 million.

Victory Metals (ASX: VTM), the closest comparable on the ASX, trades at around $180 million.

That’s roughly five times what MRD trades at, on the same style of deposit in the same state.

What’s In The Ground

Back in March, MRD’s maiden resource came in at 122.6 million tonnes grading 889ppm total rare earth oxide, and 41% of those rare earths sit in the heavy basket.

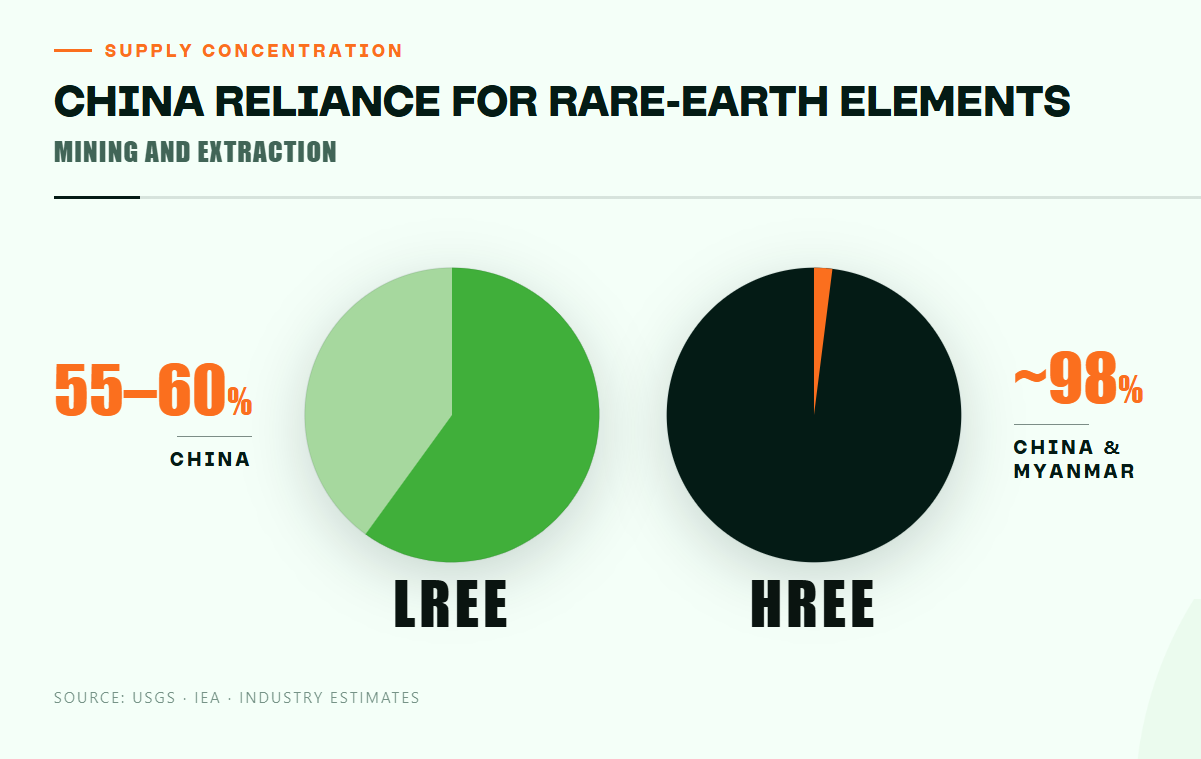

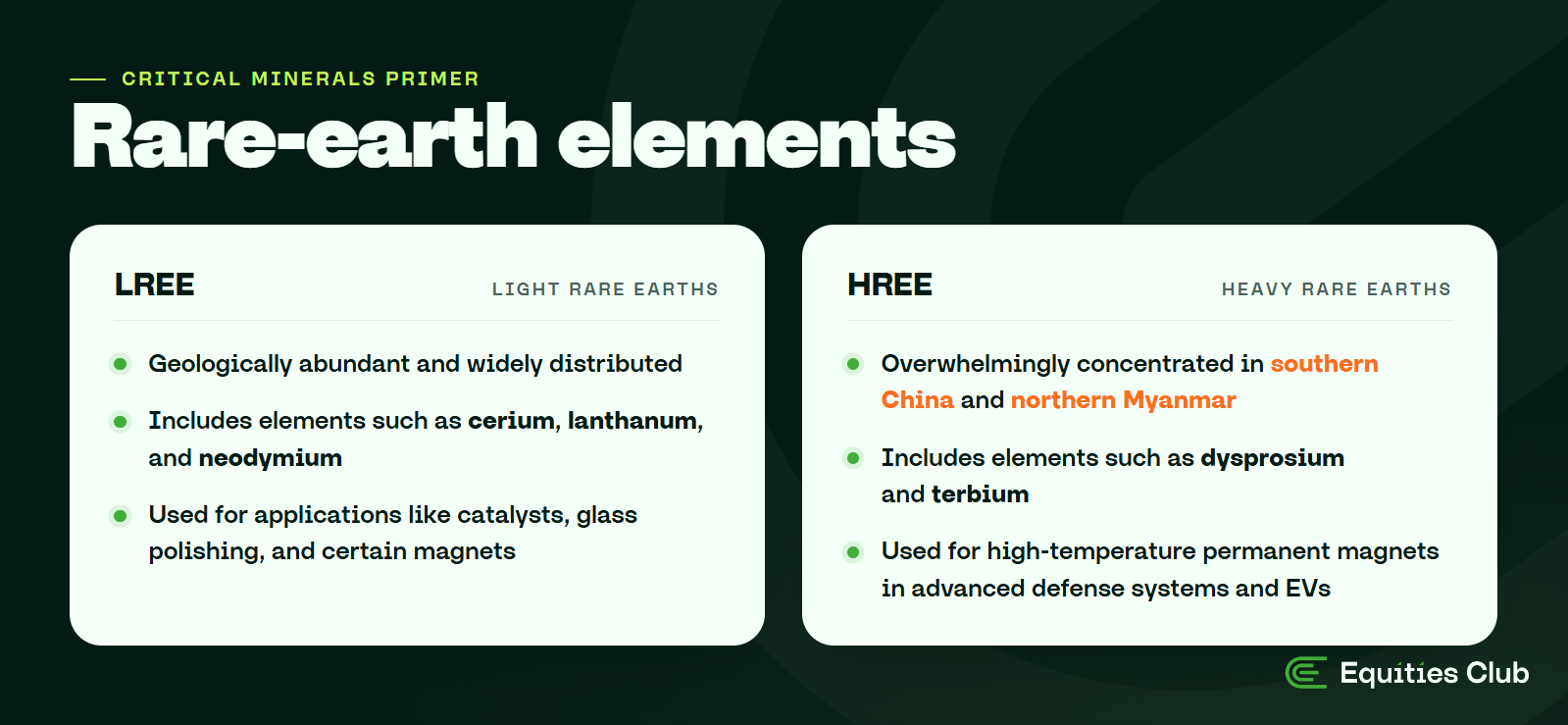

The heavies are the part of the periodic table driving the current critical mineral supply panic, and prices have been running hard while Western governments throw money at projects outside Chinese supply chains.

Inside the same deposit, MRD also holds 18,855 tonnes of contained scandium and 24,584 tonnes of contained gallium.

To put the scandium in context, the entire world produces around 25 tonnes a year, and China controls more than 95% of the world’s gallium.

Both metals are on every allied government’s shopping list, and MRD gets exposure to all three from a single project.

We covered the geology properly when MRD joined the portfolio, so we won’t redo it here. The short version is that the rocks are there in the right mix, in a jurisdiction the West actively wants to be buying from.

What the resource doesn’t tell you is whether the metals can actually be pulled out of the clay at a price that makes a project work.

That’s the question Phase 1 is built to answer.

Why The Heavies Are Running

There are 17 rare earth elements, and most of them are nowhere near as rare or valuable as the name suggests.

The ones the West is currently losing sleep over are dysprosium and terbium.

Both go into permanent magnets in tiny amounts, and they’re what keeps the magnet working when it gets hot.

That’s why you find them inside every EV motor, every wind turbine, every guided missile and every industrial robot that needs to keep running under load.

There’s no substitute for either element, and China controls almost all the global supply.

Last year, Beijing imposed export controls on both. By the time the controls bedded in, Western prices had started running well away from Chinese domestic prices, and they’ve been climbing ever since.

Dysprosium oxide for Western buyers is sitting at around US$930 per kilogram, and Terbium oxide is at around US$4,000 per kilogram

China's export licensing on the heavies has been tightening since it came in last year, which means the setup behind those price moves isn't going anywhere soon.

MRD’s resource holds 4,272 tonnes of contained dysprosium and 719 tonnes of contained terbium. Those are the two metals doing most of the work on the basket value, and they’re the two that Phase 1 is being designed around.

Grass Patch is one of a small group of ASX-listed names with a JORC heavy rare earth resource in a tier-one jurisdiction. Most other WA projects are light-dominant, where the metals trade at a fraction of dysprosium and terbium prices.

But all of that only matters if you can get the heavies out cleanly, and early testwork has already shown the heavies in MRD’s regolith leach more strongly than the lights.

That’s the recovery curve you want, because the highest-value elements come off the clay first.

Phase 1 is the program that puts proper numbers on how cleanly that split can scale.

What Phase 1 Decides

Grass Patch is what’s called a regolith-hosted deposit, which is a fancy way of saying the rare earths sit in soft weathered clay near the surface.

You can mine it with an excavator, which is a big head start on cost.

It’s also the same style of deposit China has built its heavy rare earth dominance on. The ionic clay operations in southern China produce the cheapest dysprosium and terbium on the planet, and the geology at Grass Patch is the western hemisphere’s version of that.

With this style of deposit, everything rides on the leach. The metals are loosely stuck to the clay, and a mild acid wash is supposed to pull them off cleanly.

When that works, the economics look beautiful.

When it doesn’t, recoveries collapse. The graveyard of junior rare earth stocks is full of companies that had a resource and couldn't crack the chemistry.

Larder's team has four jobs at the Winstons and Keiths prospects, both of which sit inside MRD's defined resource:

Characterise the clay so the underlying chemistry is fully understood

Test beneficiation, which is the step that strips out the waste and concentrates the good stuff before the main leach

Develop and optimise the leach itself, which is the chemical step that pulls the rare earths off the clay

Produce a clean batch of conditioned feed for the next stage of testwork

Get those right and MRD has a baseline the rest of the metallurgical pathway can build on, including the work flowing into the CRADA framework still being drafted with Lawrence Livermore National Laboratory in the US.

What MRD's Got That VTM Doesn't

Victory Metals (ASX: VTM) is the closest comparable project on the ASX. Same clay-hosted, heavy-loaded deposit style, same WA jurisdiction.

VTM has been at North Stanmore since 2022 and they’re well into pre-feasibility work, with strategic partners on the books. That’s most of why they trade at around $180 million and MRD trades at $36 million.

MRD isn’t trying to leapfrog VTM. The work happening at Grass Patch right now is the same work VTM was doing a couple of years back, and the comparison only gets interesting if you ask what MRD has that VTM hasn’t.

Two things stand out.

The first is gallium. VTM’s resource carries heavy rare earths and scandium. MRD’s carries all of that plus gallium, the only critical mineral in the basket VTM doesn’t have on its books.

The second is the CRADA framework still being drafted with Lawrence Livermore National Laboratory. We’re not aware of any other ASX rare earth junior with that kind of US lab partnership in flight.

Once it’s signed, it opens up US government funding pathways most juniors at this stage don’t have access to.

Phase 1 is the program that starts building MRD’s technical case toward the kind of dataset VTM has already put together.

The valuation gap is what it is. The question worth watching is how fast MRD closes it.

“This new phase of test work sets the foundation for everything that follows from a processing standpoint.”

Allister Caird - Managing Director & CEO of MRD

What Comes Next

Phase 1 results are the first deliverable from here. After that, the focus widens to the rest of the development pathway.

The re-assay of historical pulps at Grass Patch should flow into a resource upgrade, partnership agreements are still to be finalised, and a more advanced stage of met work will follow on from this Phase 1 baseline.

Met work is also where junior rare earth projects get validated or quietly fade. Lab recoveries don’t always translate to bulk material, and reagent costs can swing the economics.

We added MRD to the portfolio in March. Phase 1 is the next major test of the case we wrote up at the time.