The Quiet Money: How ASX Dividends Work and Who Paid Well in 2025

A practical guide to the best ASX dividend stocks, franking credits, and income strategies for Australian investors

Nobody brags about dividend stocks at a barbecue. You never hear someone lean over the esky and say “mate, you should see my franking credits.”

But the people who’ve been collecting dividends from the same handful of companies for a decade tend to be the calmest investors in any room, and 2026 has given everyone plenty of reasons to want to be calm.

We love the stories about the 10-bagger. The IPO that made early believers rich. The explorer that hit copper and ran 400% in a week. Nobody wants to hear from the bloke who bought BHP in 2009 and just kept reinvesting the dividends. He’s boring.

He’s also rich.

If you'd gone camping for all of 2025, come back and checked your portfolio, you'd assume you missed a quiet year. You didn't.

Tariffs, a federal election, Trump moving markets via Truth Social, a new war in the Middle East, and AI advancing fast enough to make half the country nervous about their careers.

Yet the ASX 200 finished 2025 up more than 6% and pushed toward new highs in 2026. And the dividend cheques kept arriving.

We spend most of our time at the smaller end of the market. Early-stage companies, drill results, the kind of stocks that can move 50% on a single announcement. This piece is about the other end entirely.

The end where companies make money, pay tax on it, and send you a cheque twice a year.

What follows is the top 10 ASX-listed dividend payers to start 2026, the best from 2025, and the top 10 from mining and energy of 2025. We've also pulled apart how dividends actually work and whether the good ones are likely to keep paying.

First though, the basics.

What is a Dividend?

A dividend is simply a company sharing part of its profits with shareholders. You own a slice of the business, and when it makes money, you get a cut.

Most companies that pay dividends do so twice a year: an interim dividend partway through the financial year (February/March) and a final dividend (August/September).

There’s no minimum shareholding required to qualify. Even a small holding entitles you to your proportional share of the payout.

In Australia, dividends also come with a tax angle worth understanding: they’re either franked or unfranked.

Franked and Unfranked Dividends Explained

Franked dividends

Franked means the company already paid tax on the money before it reached you. Australia's company tax rate is 30% for most listed companies, so a franked dividend comes with a credit for that 30%.

What happens next depends on your tax bracket. If you're on 30%, you're square. The company already covered it. If you're higher, say 37%, you pay the difference. If you're lower, you might get a refund. That last bit is why retirees love franking credits.

Unfranked dividends

Unfranked dividends don’t carry a tax credit. The full amount hits your taxable income and gets taxed at your marginal rate.

Franking credits are one of the biggest advantages of investing in Australian shares. You don't get the same deal from interest, rent, or most overseas income.

Understanding Dividend Dates (and When You Need to Own the Shares)

There are four dates that matter when a dividend gets paid. Only one of them determines whether you actually get the money.

Announcement date

This is when the company tells the market a dividend is coming. They'll disclose the amount, whether it's franked or unfranked, and lay out the ex-dividend, record, and payment dates. Owning shares on this date alone doesn't mean you're getting paid.

Ex-dividend date

The ex-dividend date is the cutoff: to receive the dividend, you need to own shares before this date. Buy on or after it, and the payout goes to whoever held the shares before you. This trips people up more than anything else in dividend investing.

Record date

The record date is when the company reviews its official list of shareholders to confirm who gets paid. If you bought before the ex-dividend date and you’re on the register at close on this date, you qualify.

Payment date

This is when the money actually lands - either in your bank account or reinvested through a dividend reinvestment plan if you’ve opted in.

If you take one thing from this section: buy before the ex-dividend date. Everything else is plumbing.

The Case for Dividends

When markets are running hot, nobody’s thinking about dividends. Growth stocks grab the headlines. But growth stocks also get smashed when expectations shift, and as we’ve seen recently, a war on the other side of the world can rattle the entire ASX.

Dividend payers tend to keep sending cheques through all of it. That’s the bit most people underestimate. Over time, that reliability compounds in ways that are hard to appreciate until you see it in your own portfolio.

Australia also has a feature most other markets don’t: dividend reinvestment plans, or DRPs.

These let you automatically reinvest your dividends into more shares, usually without paying brokerage and sometimes at a small discount to the market price. The dividends are still taxable income, but reinvesting instead of pocketing the cash means your position quietly compounds without you lifting a finger.

Who Dividend Investing Suits (and When It Matters Most)

How you think about dividends depends on where you’re at.

If you’re 23, dividends aren’t paying your rent. Most people at that stage reinvest them and let compounding do the work over decades. The money is almost irrelevant. What matters is that your shareholding is quietly getting bigger every six months.

Mid-career, it shifts. Some keep reinvesting. Others start redirecting dividends toward a mortgage, school fees, or that renovation that's been on the list since 2019. It becomes more about flexibility than a single strategy.

Closer to retirement, dividends start doing what most people assume they always do: providing income. Consistent payouts can cover living expenses without having to sell down your portfolio, which matters when you're no longer earning a wage.

A 25-year-old and a 65-year-old might own the same stock for completely different reasons. Neither is wrong.

The Market Backdrop From 2025

For anyone unfamiliar with the index, the ASX 200 tracks the 200 largest listed companies by market cap. There are more than 2,000 companies on the exchange, but those top 200 account for roughly 80% of its total value. The market's now worth more than $2.6 trillion.

What keeps pushing it higher is fairly simple: bank profits, commodity prices, and the relentless flow of superannuation money into large caps. Every pay cycle, 12% of every wage in the country gets funnelled into super, and most of that ends up in the biggest, most liquid stocks on the board.

Those tend to be the same companies paying dividends.

The ASX has long had a reputation as one of the more income-friendly exchanges going around. It's well-regulated, liquid, and tends to attract capital when investors want somewhere reliable to park their money.

2026 has seen commodity prices bounce around and the property market keep the big banks happy, but the super money flows in on autopilot regardless.

High Yield Does Not Always Mean High Quality

Picture two stocks on a screen. One yields 4%. The other yields 10%. A reasonable person picks the 10. A reasonable person would also be walking into a trap that catches thousands of investors every earnings season.

Because yield is just the dividend divided by the share price, and when a share price drops 40% while the dividend stays the same, the yield looks incredible right up until the board meets and slashes the payout to match reality.

Profits can be massaged with accounting, but dividends are paid from cash, and when payouts consume most of a company’s free cash flow, there’s not much left in the tank if conditions turn.

This matters most in cyclical sectors like resources, where dividends can be generous when prices are high but thin out quickly when they’re not.

The companies that pay reliably for years tend to be the ones nobody gets excited about at barbecues. Steady earnings. Conservative management. The kind of businesses that would rather protect the balance sheet than make a yield table.

They rarely top the rankings in any given year. They rarely blow up either.

How to Assess a Dividend Stock

Start with the business, not the yield. A bank collecting mortgage repayments every month has a very different dividend profile to a gold miner whose cash flow swings with the spot price. Both might show the same yield on a screen. The story underneath is completely different.

Pay attention to how management treats the dividend. Some companies aim to smooth payouts over time, keeping them steady even when profits dip. Others let dividends ride with conditions, paying big when times are good and pulling back when they're not.

Neither approach is wrong, but you want to know which one you own before conditions change.

Then zoom out. Mining dividends track commodity prices. Bank dividends track credit growth and interest rates. Retailers follow consumer spending. If you can read what's driving earnings in a sector, you can usually see a dividend cut coming well before it arrives.

Common Dividend Mistakes New Investors Make

Two traps catch people that we haven’t covered yet.

The first is buying shares right before the ex-dividend date, expecting easy money. The dividend lands in your account, but the share price usually drops by a similar amount the morning it goes ex-dividend. If you factor in tax you might’ve gone backwards.

The second is concentration. Australian dividend portfolios have a habit of drifting heavily into banks and resources, because that’s where income has historically been highest. It works fine for years, but when those sectors turn at the same time, the whole portfolio feels it at once.

How Often Should You Review Dividend Stocks?

Less often than most people assume.

Most dividend-paying companies are fairly predictable beasts. They’re established businesses doing much the same thing year after year, and checking the share price every morning doesn’t change that.

Pay attention when new information lands. Financial results, dividend announcements, anything that could knock earnings around. Those are the moments that matter.

If your miner’s commodity price collapses, that’ll flow through to the dividend. If your bank’s mortgage defaults start ticking up, same deal.

Short-term noise rarely changes the story. Structural shifts can change it permanently. Learning to tell the difference takes time, and it’s one of the more valuable skills a dividend investor can develop.

The hardest part for most people is doing nothing when nothing needs to be done.

What to do Next

If you’re new to dividend investing, the best thing you can do is pick a handful of dividend-paying companies and follow them for a few months.

Watch when dividends get announced, how the share price moves around the ex-dividend date, and whether payouts stay steady or jump around.

You’ll learn more from observing a full dividend cycle than from chasing a headline yield.

After that, the rest comes down to your own situation. How much volatility you’re willing to stomach. Whether you need income now or you’d rather let it compound for a decade.

There’s no single right answer, and the bloke at the barbecue who never brags about his dividends worked that out a long time ago.

Highest paying Dividend stocks to start 2026

Earnings season has just wrapped up on the ASX, and with it a fresh round of half-year results covering July to December.

This is where you find out whether companies met the market's expectations. Stronger profit usually means a bigger dividend. Disappointing results, and the payout's usually the first thing to get trimmed.

We've gone through the reports and pulled out the companies that are off to a good start. Below are the top 10 dividend payers to start 2026, ranked by yield.

The ex-dividend dates have passed on these, but with another payout due after full-year results, it gives you a read on who's tracking well.

(Note: Past dividend payments are not indicative of future payments. The rankings reflect payouts recorded for the interim 2026 dividend. The final dividend is unknown and to be calculated at a later date)

Top 20 Dividend-Paying Stocks of 2025

Here are the top 20 ASX dividend payers from 2025, ranked by total payout and yield.

This list reflects what happened in 2025, not a prediction for 2026. Profits change, and dividend policies follow. Think of it as a snapshot of who was paying well, and not a guarantee they'll keep doing so.

(Note: Past dividend payments are not indicative of future payments. The rankings reflect payouts recorded across the 2025 financial year and may differ in 2026. Yield has been calculated based off the closing price 31 December 2025)

How Commodity Prices Shaped Dividends in 2025

Dividends in 2025 tracked where the money was being made in commodities. Gold led the way, iron ore held up, and coal quietly kept rewarding shareholders without making much noise.

Gold was on a tear through 2025 and into early 2026, hitting record after record as central banks loaded up and inflation worries kept buyers coming.

The war in the Middle East has pulled it back roughly 15%, but at around US$4,750/oz it's still well above the levels that have producers swimming in cash.

That's flowed straight through to dividends. If gold holds anywhere near here, expect that to continue.

Iron ore held firm around US$100/t despite the China slowdown. The massive cheques from a few years ago have eased, but the majors are still paying well.

Lithium has had a shocking run. Oversupply and weak demand crushed prices for the best part of two years. There are signs that’s turning, with several analysts expecting a stronger 2026.

Prices settled from their peaks, but disciplined producers kept paying, and some of the highest yields on the ASX came from names most people weren't watching.

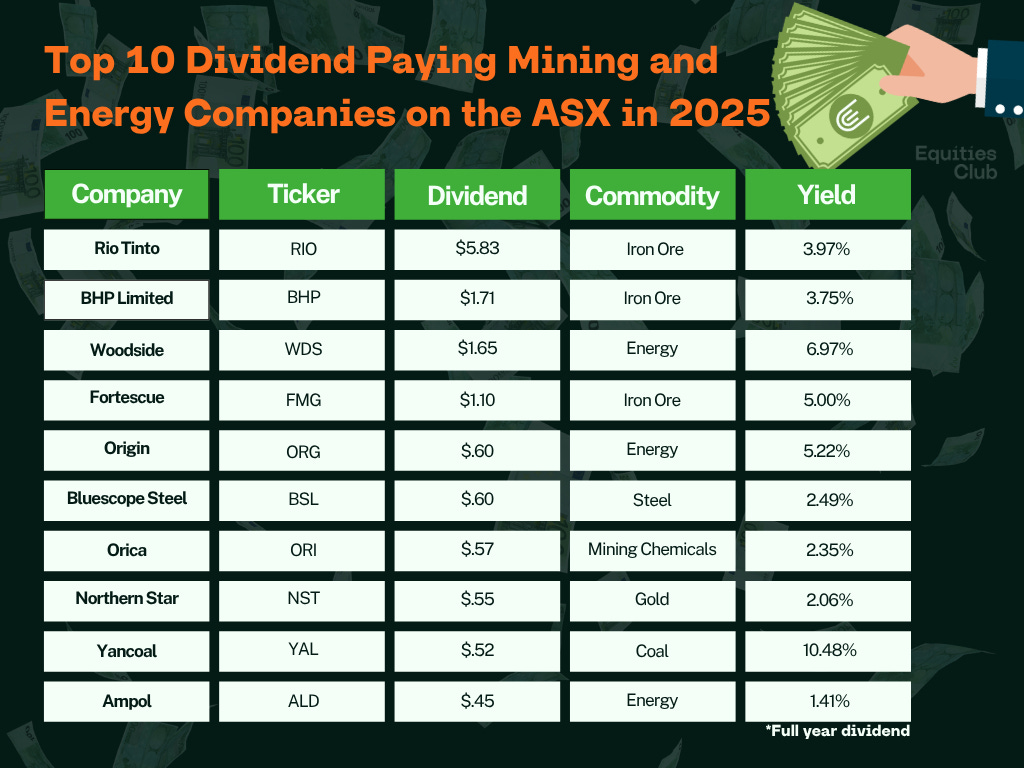

Top 10 Dividend-Paying Mining and Energy Stocks of 2025

Here are the top ten ASX-listed mining and energy companies from 2025 based on dividend payments.

(Note: Past dividend payments are not indicative of future payments. The rankings reflect payouts recorded across the 2025 financial year and may differ in 2026. Yield has been calculated based off the closing price 31 December 2025)

The Superannuation Tailwind

Australia’s population has passed 27.7 million and keeps growing faster than most developed economies.

Every new job, every pay rise, every employer contribution tips more money into the super pool. Right now, 12% of every wage in the country gets funnelled into the system automatically.

Most of that money ends up in large, liquid ASX-listed companies that have been paying dividends for decades.

Think BHP, Woolies, Commonwealth Bank. The names everyone knows.

Super funds buy them because they generate cash and return it to shareholders. They keep buying them regardless of what the broader market is doing.

Most funds also operate under mandates that cap how much they can put into smaller stocks until a company hits a certain size and liquidity threshold, often around ASX 200 inclusion.

Once a company enters the index, it becomes a natural destination for those inflows.

In practice, Australia's compulsory super system is a constant buyer of dividend-paying large caps.

That buying pressure is there whether markets are up, down, or sideways.

Will 2026 Repeat The Returns Of 2025?

Probably not, and expecting it to would be a mistake.

The list of top dividend payers shifts every year. A gold miner paying record dividends at the top of the cycle can look very different twelve months later. Same company, different commodity price, different size cheque.

Dividends move with profits, and profits move with conditions nobody can predict 12 months out. The companies paying well today may look different by December.

The best you can do is understand what’s driving the earnings behind the payout. The tables in this piece are a snapshot of 2025 only.

If you take one thing from this piece, it's that last year's top payer isn't guaranteed to be next year's.

The Final Step When Investing

Payouts rise and fall with profits, and even the most reliable payers are influenced by forces outside their control. A war can eat into margins overnight. A rate move can shift the maths on a bank’s lending book. Commodity prices don’t ask permission before they turn.

None of that changes the basic proposition. Companies make money, they share it with the people who own them, and over time that adds up to something worth having.

The bloke who bought BHP in 2009 and kept reinvesting the dividends didn’t time anything perfectly. He just kept showing up.

Patience isn't exciting. But the patient investors tend to be the ones still standing when the dust settles.

Glossary of Regularly Used Financial Terms

ASX (Australian Securities Exchange) – Australia’s main stock exchange, where shares in publicly listed companies are bought and sold.

ASX 200 - An index tracking the 200 largest companies listed on the ASX by market capitalisation and liquidity. Commonly used as the benchmark for the Australian share market.

Announcement date - The date a company formally announces it will pay a dividend, including the amount, whether it is franked or unfranked, and the key dates that follow. Owning shares on this date alone does not guarantee you will receive the dividend.

Assessable income – Income the ATO counts when calculating your tax, which can include dividends.

Benchmark – A reference point used to measure market or portfolio performance, such as the ASX 200.

Biotech – Short for biotechnology. Companies developing medical or science-based products, often with higher risk and less predictable profits than mature dividend payers.

Blue-chip stocks – Large, established companies with long operating histories, strong balance sheets, and regular dividend payments.

Brokerage – A fee charged by a broker when you buy or sell shares.

Capital – Money invested or available to be invested.

Capital growth – An increase in a company’s share price over time, separate from dividend income.

Cash flow – The actual cash a business generates from its operations. Dividends are paid from cash, not accounting profits.

Central bank – A country’s main monetary authority (such as the RBA in Australia) that influences interest rates and financial conditions.

Compounding – Earning returns on your returns over time. With dividends, this often occurs when payouts are reinvested to buy more shares.

Consumer spending – Household spending across the economy, which can influence company profits, particularly for retailers and banks.

Credit growth – Growth in borrowing and lending across the economy, which can impact bank earnings and dividends.

Cyclical sectors – Industries whose earnings rise and fall with economic or commodity cycles, such as mining, energy, and resources.

Dividend – A payment made by a company to shareholders as a share of its profits.

Dividend history – A company’s track record of paying dividends over time. Useful for context, but not a guarantee of future payments.

Dividend income – The cash an investor receives from dividends over a period of time.

Dividend-paying stocks – Companies that regularly distribute part of their profits to shareholders as dividends.

Dividend policy – A company’s approach to paying dividends, including how stable or variable payouts are through different market conditions.

Dividend payout ratio – The portion of a company’s profits or cash flow that is paid out as dividends.

Dividend reinvestment plan (DRP) – A program that allows shareholders to automatically use dividends to buy more shares in the same company, usually without brokerage and sometimes at a discount. Dividends remain taxable income.

Dividend yield – The annual dividend paid by a company divided by its current share price, expressed as a percentage. It shows income relative to price, not total return.

Earnings – A company’s profit after expenses.

Economic conditions – The broader environment affecting businesses and markets, including growth, inflation, interest rates, and employment.

Employer contribution – The percentage of wages paid into an employee’s superannuation account under Australia’s compulsory system.

Equities – Another term for shares or stocks. The "equity market" is simply the market where shares are traded.

Essential services – Products or services people continue to pay for in most conditions, such as utilities or major financial services, often supporting steadier earnings.

Ex-dividend date – The most important dividend date. To receive a dividend, an investor must own the shares before this date. Buying shares on or after this date means the upcoming dividend will not be received.

Federal election – Australia’s national election that determines the federal government and can influence markets through policy expectations.

Final dividend – A dividend paid at the end of a company’s financial year, usually larger than the interim dividend.

Franked dividend – A dividend that includes a tax credit for company tax already paid, which can be used to offset an investor’s personal tax.

Franking credit – The tax credit attached to a franked dividend, reflecting the 30% company tax rate already paid in Australia.

Free cash flow – Cash remaining after a company covers its operating costs and capital spending. A key measure of dividend sustainability.

Headline yield – The stated dividend yield without considering sustainability, risk, or future earnings.

High yield – A relatively large dividend yield compared to other companies or the broader market.

Inflation – A general rise in prices over time, which can influence interest rates, company costs, and investor behaviour.

Index – A basket of shares used to track the performance of a market or group of companies, such as the ASX 200.

Index provider (S&P Global) – The organisation responsible for maintaining and setting the rules for indices such as the ASX 200.

Interest rates – The cost of borrowing money or the return earned on savings, influenced by central bank policy.

Interim dividend – A dividend paid partway through a company’s financial year.

Liquidity – How easily shares can be bought or sold without significantly affecting the price.

Low-cost mining assets – Mining operations that can remain profitable even when commodity prices fall, often supporting more resilient dividends.

Marginal tax rate – The tax rate you pay on your last dollar of income, which determines how dividends are ultimately taxed.

Market capitalisation (market cap) – The total value of a company, calculated by multiplying its share price by the number of shares on issue.

Mining majors – Large, established mining companies, often global operators and regular dividend payers.

Mining discovery – A new mineral find that can drive speculative share price moves, often unrelated to dividends.

Monetary policy – Actions taken by a central bank to influence interest rates and money supply, affecting markets and economic activity.

Oversupply – A situation where supply exceeds demand, often putting downward pressure on prices.

Part-owner – When you buy shares, you own a small piece of the company and may be entitled to dividends.

Payout – The amount of money a company pays out to shareholders as dividends.

Payment date – The date a dividend is actually paid to shareholders, either in cash or via a dividend reinvestment plan.

Personal tax bracket – The tax rate you pay based on your income level.

Portfolio – A collection of investments held by an individual or fund.

Property market – The market for buying and selling real estate, which has a significant influence on banks and the broader economy.

Record date – The date a company checks its shareholder register to determine who is entitled to receive the dividend.

Resources sector – Industries involved in extracting natural resources such as metals, minerals, coal, and energy.

Sector – A group of companies in the same industry, such as banks, resources, retailers, or healthcare.

Sector exposure – How much of your portfolio is concentrated in one part of the market, such as banks or miners.

Sentiment – How optimistic or pessimistic investors feel, which can influence prices in the short term.

Settlement (T+2) – The standard ASX settlement cycle, where a share trade is finalised two business days after the transaction occurs.

Share price – The current market price of a company’s shares.

Shareholder – A person or entity that owns shares in a company.

Small-cap stocks – Smaller companies listed on the ASX, often with higher growth potential but higher risk.

Speculative stocks – Higher-risk investments where outcomes depend on future events or developments.

Superannuation – Australia’s compulsory retirement savings system funded by employer contributions.

Tariffs – Taxes imposed on imported goods that can affect trade, costs, and company profits.

Tax credit – A credit that reduces the amount of tax you owe, such as franking credits attached to franked dividends.

Taxable income – Income used to calculate your tax. Unfranked dividends are generally added to taxable income.

Term deposits – Bank savings products offering a fixed interest rate for a set period, generally lower risk than shares.

Total return – The combined return from both share price movement (capital growth) and dividends.

Unfranked dividend – A dividend paid without a tax credit, meaning the full amount is taxed at the investor’s marginal rate.

Volatility – The degree of price movement in markets or individual shares over time.

Yield – A percentage measure of income relative to a share price, most often referring to dividend yield.

Yield chasing – Focusing solely on high dividend yields without considering sustainability or risk.