Three Critical Minerals in One Deposit - Our New Addition

A maiden heavy rare earth resource, gallium, scandium, and a partnership with a US nuclear laboratory. Here’s why we’re backing Mount Ridley Mines at $31.9 million

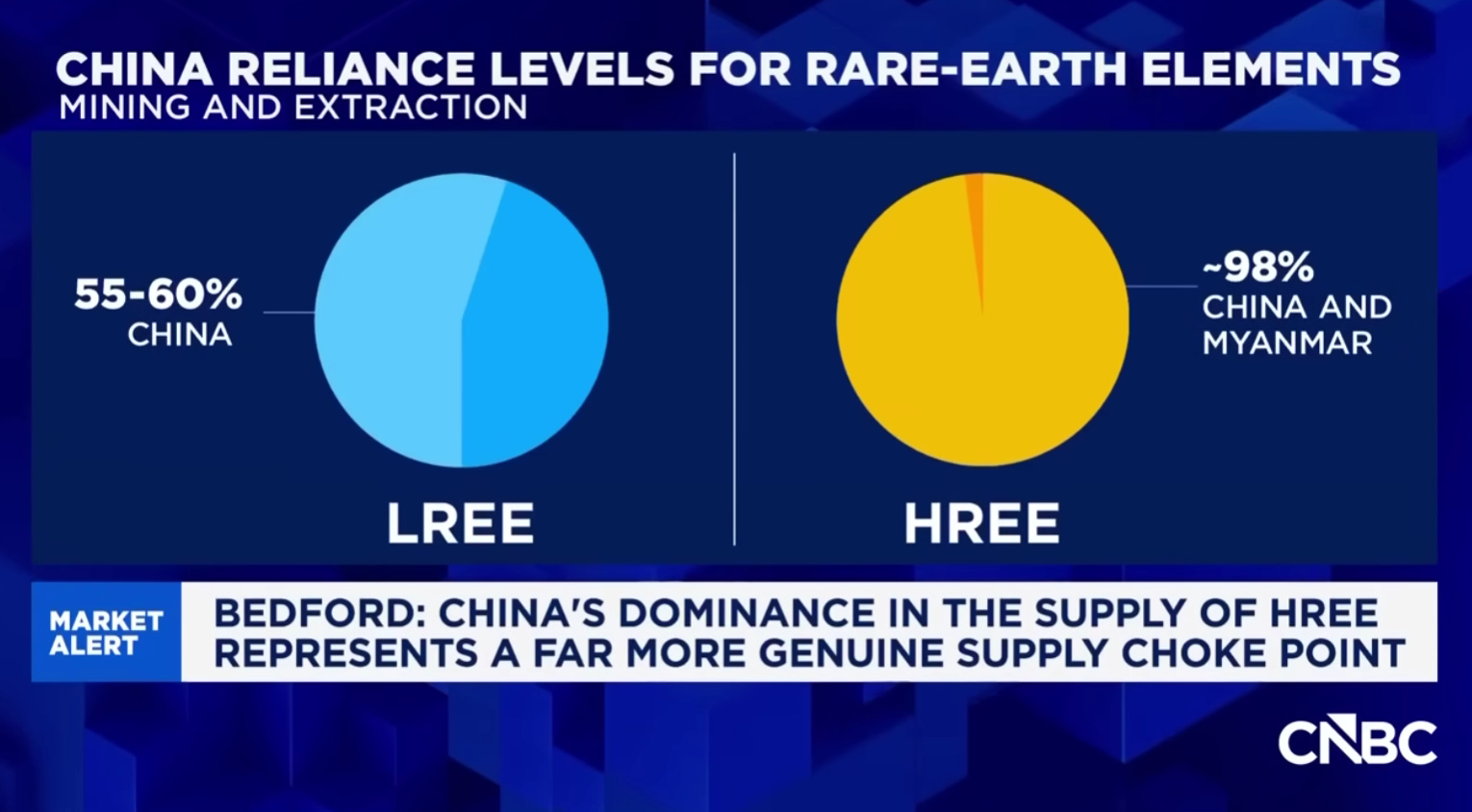

China controls the processing of almost every heavy rare earth element the western world needs.

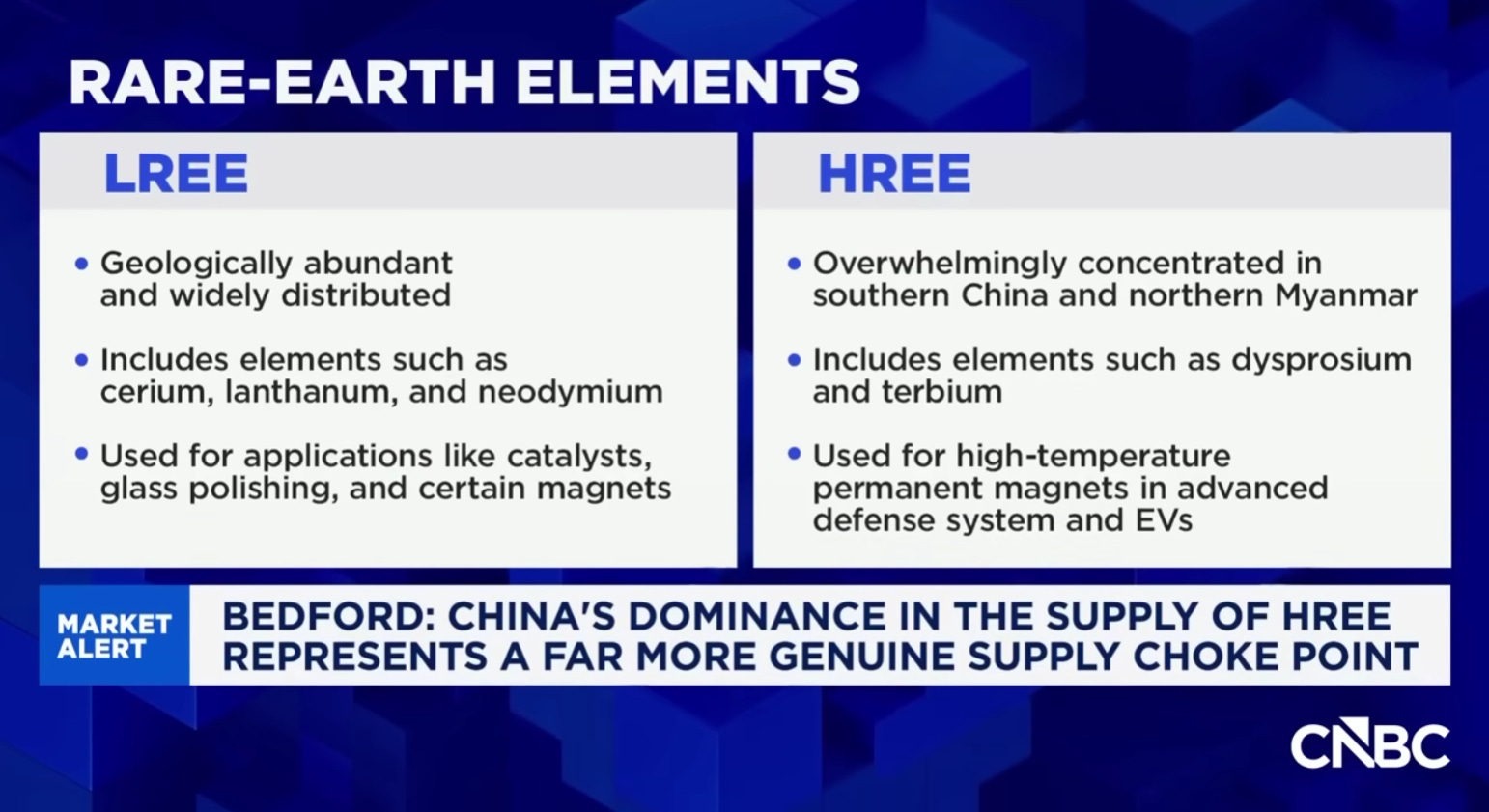

There are seventeen rare earth elements, but two matter more than the rest right now: dysprosium and terbium. The magnets inside every EV motor, every wind turbine, every military actuator, every industrial robot - they all need these two elements to function at operating temperature.

There is no substitute for either element.

In April 2025, Beijing imposed export controls on both. European dysprosium prices have since quadrupled relative to Chinese domestic prices. Terbium oxide is up over 100% year-to-date.

The Pentagon is stockpiling both elements. The US Department of Energy has been handing out hundreds of millions to anyone with a non-Chinese source, and the Australian and US governments signed a formal framework in October 2025 to fast-track mining and processing in allied jurisdictions.

Meet Mount Ridley Mines (ASX: MRD), our latest portfolio addition.

MRD has just delivered a maiden JORC rare earth resource, and all of that mineralisation sits in the same ground as the company’s existing scandium and gallium resources.

Three critical minerals, one deposit, all from surface.

Each one has its own supply crunch. China controls the rare earths and the gallium. Scandium barely has a supply chain at all - global production is 25 tonnes a year against forecast demand of 117 tonnes.

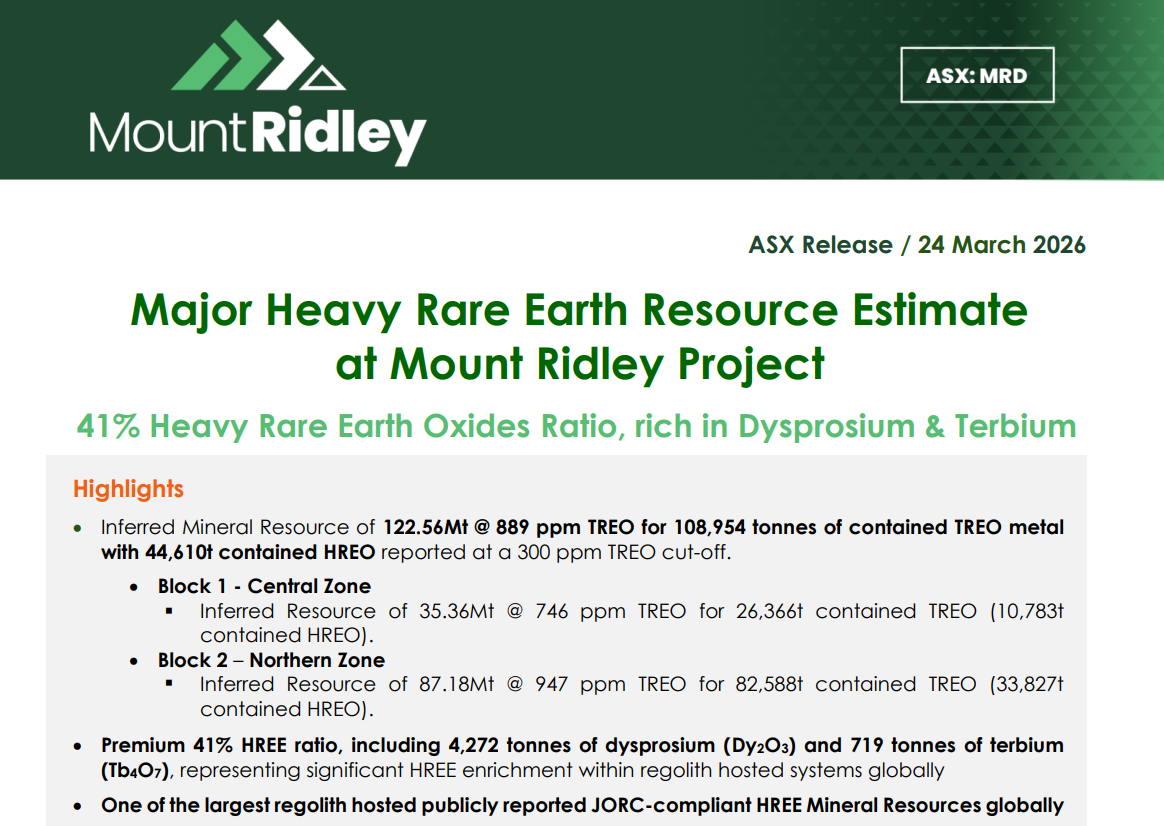

MRD's numbers are worth sitting with for a $31.9 million market cap. 122.56 million tonnes of mineralised material, containing just under 109,000 tonnes of rare earth oxide, including 4,272 tonnes of dysprosium and 719 tonnes of terbium - the two elements driving the supply panic.

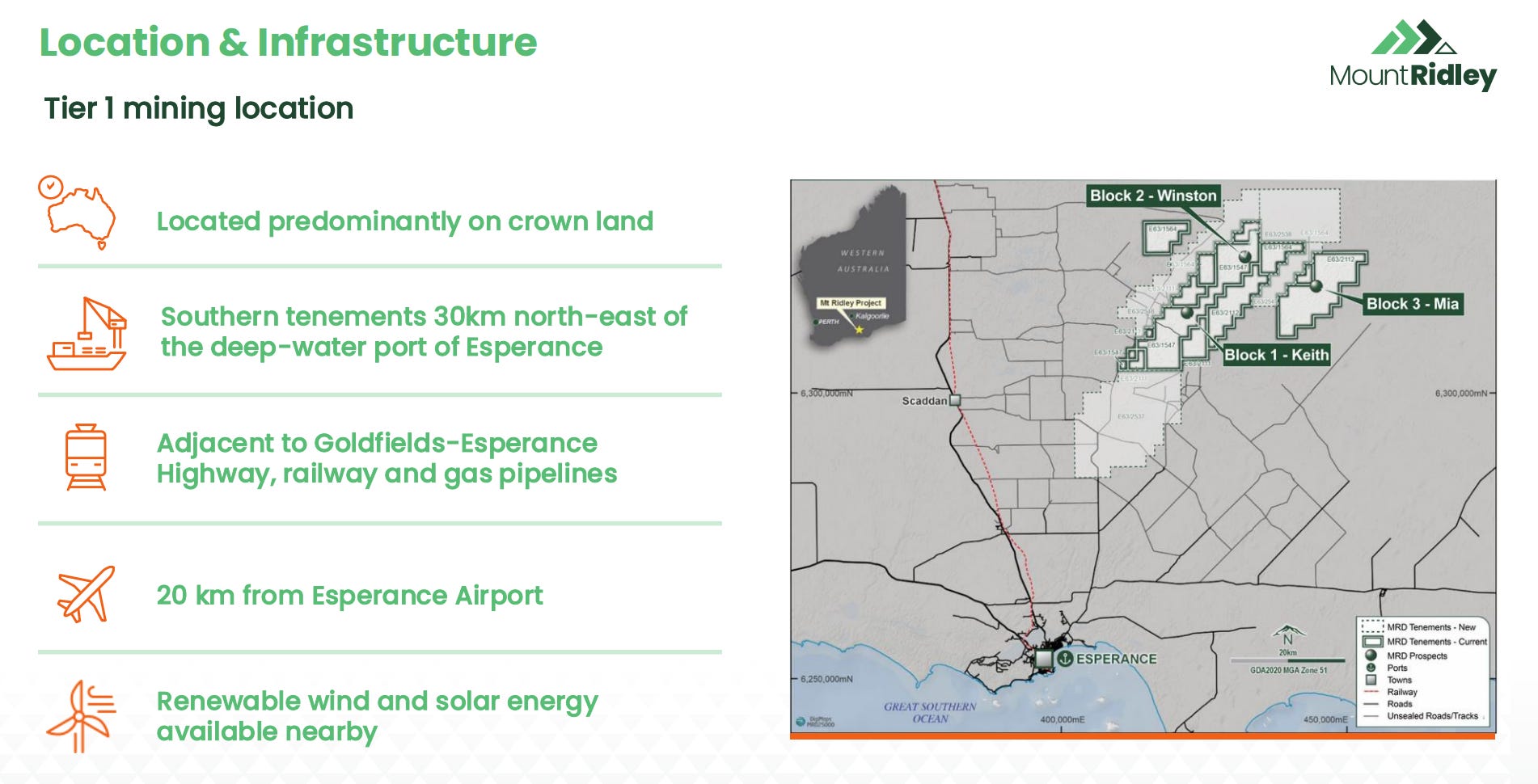

The project sits in Western Australia, 25 kilometres from the deep-water port at Esperance. It’s a tier-one jurisdiction with real infrastructure.

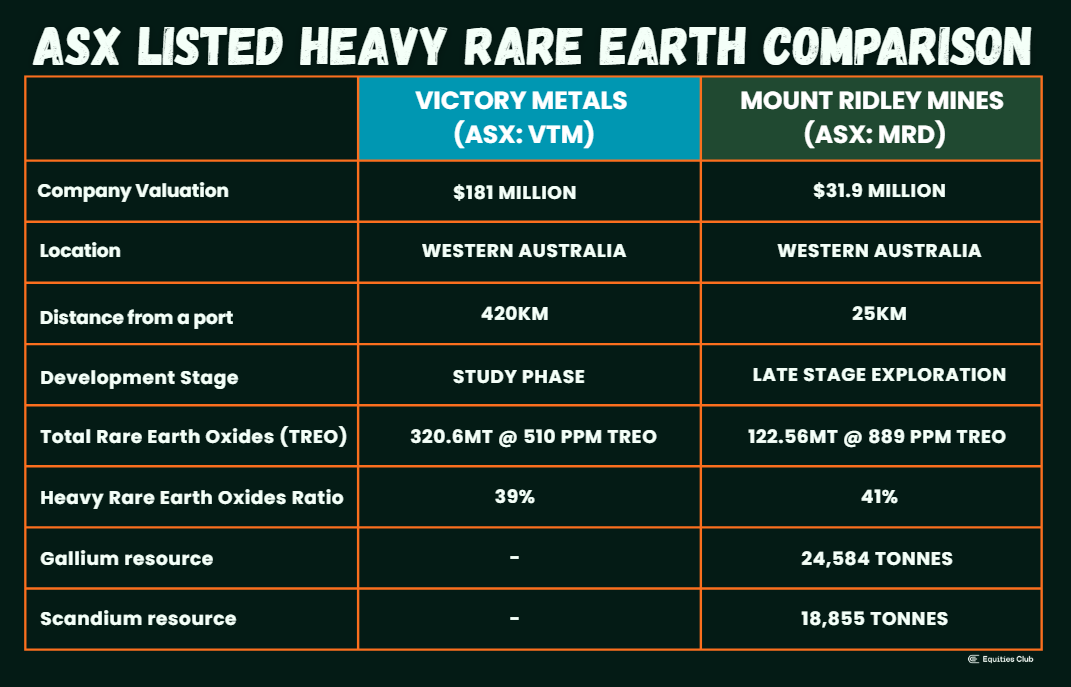

The nearest comparable is Victory Metals (ASX: VTM), a single-commodity clay-hosted rare earth play in WA trading at roughly $180 million. MRD sits at less than a fifth of that, with two additional strategic commodities and over 80% of its 63km mineralised corridor still untested.

That’s the mismatch that caught our eye.

With a stacked catalyst pipeline through 2026 and a bilateral partnership with Lawrence Livermore National Laboratory - one of the US government’s three nuclear security laboratories - we reckon MRD has the setup to close that gap quickly.

The Maiden Resource - What Landed Today

Today’s Mineral Resource for MRD of 122.56Mt @ 889 ppm contains about 109,000 tonnes of rare earths overall, including roughly 45,000 tonnes of the more valuable heavy rare earths.

Rare earths split into two groups: lights and heavies. The heavies are where the money is.

MRD’s resource has a 41% heavy rare earth ratio. Victory Metals at North Stanmore runs about 39%. That puts MRD at the top end for this style of deposit on the ASX.

Dysprosium and terbium are what stop permanent magnets from demagnetising at high temperatures. Without them, the motor in your EV overheats and the generator in your offshore wind turbine shuts down.

Beijing knows that, which is why they’ve kept a chokehold on processing and slapped export controls on both. If the West wants to build anything with a permanent magnet in it, the supply has to come from somewhere else.

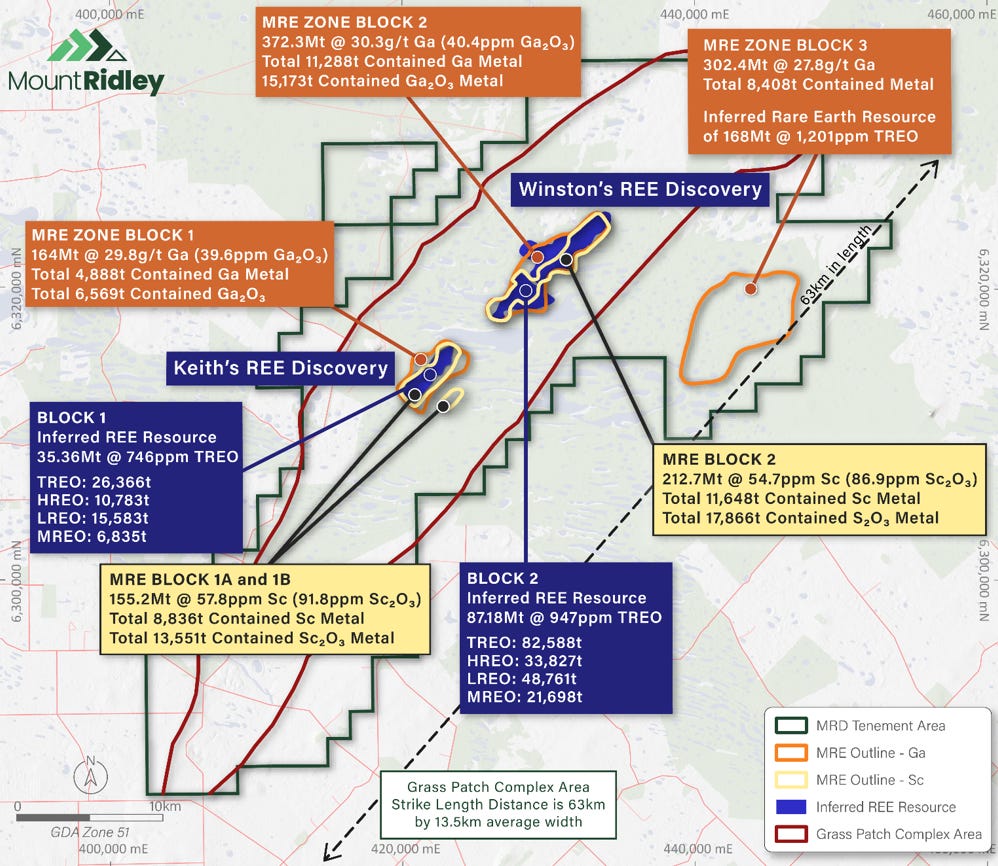

The resource is split across two blocks within the Grass Patch Complex.

Block 2, the larger of the two, hosts 87.18 million tonnes at 947 ppm TREO. Block 1 carries 35.36 million tonnes at 746 ppm.

Both are shallow, flat-lying and continuous from surface to about 52 metres depth.

Shallow is good - it means you can excavate with standard earthmoving gear. No drill and blast. No underground development. This is the same deposit style that has made Chinese ionic clay operations the cheapest rare earth producers on the planet.

The resource also carries roughly 23,500 tonnes of combined neodymium and praseodymium - the light rare earths that form the base of every permanent magnet. The heavies get the headlines, but the lights add real tonnage underneath.

Scandium is basically a steroid for aluminium. Add a tiny amount to an aluminium alloy and it gets dramatically stronger, lighter and more resistant to fatigue.

The aerospace industry has used it for years. More recently, humanoid robot manufacturers have started building frames with scandium-aluminium alloys.

MRD holds 18,855 tonnes of contained scandium. That’s one of the largest JORC-compliant endowments in the world, in a market where global production sits at 25 tonnes a year and 95% comes from China, Russia and Kazakhstan.

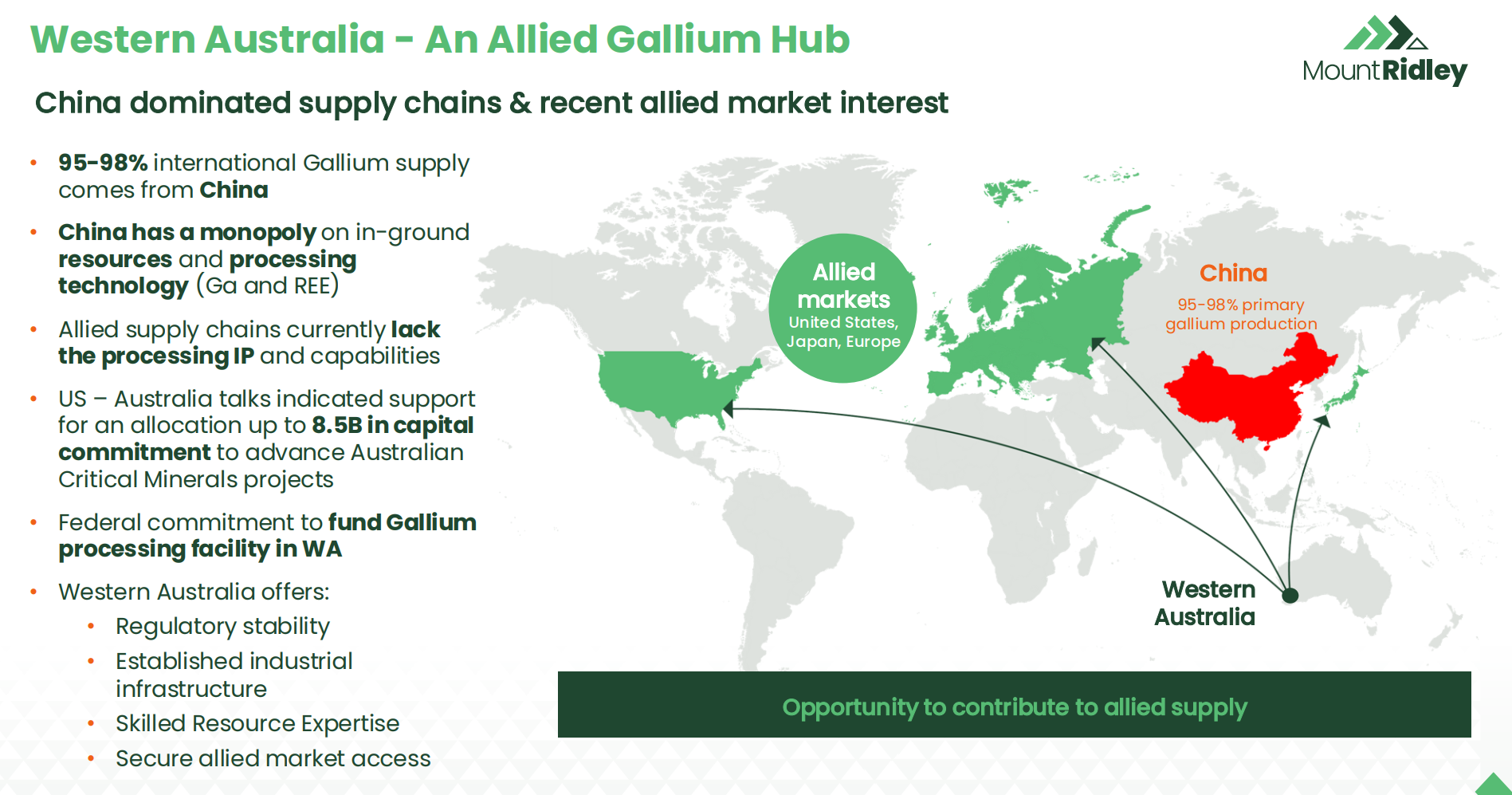

Gallium is the metal behind compound semiconductors - the chips powering 5G networks, EV fast chargers and military radar systems.

It’s another commodity where one country controls almost all of the refined supply. MRD’s 24,584 tonnes of contained gallium across 838.7 million tonnes represents roughly 34 years of current world production.

Three critical minerals, same deposit, same ground. Every dollar MRD spends on development has the potential to unlock value across all of them.

Why This Resource is Likely the Starting Point

The Grass Patch Complex runs for 63 kilometres along strike. Today's resource covers about 15 kilometres of that. The other 80% is untested.

The ground either side of the resource blocks shows the same geological signatures - the same gravity anomalies, the same structural controls - as the ground that just produced a 122 million tonne resource. Which is either a coincidence or a much bigger deposit (we know which way we're leaning).

MRD’s geophysics review has identified seven primary gravity targets totalling 33km of untested strike, with the highest-priority area being a 12.8km trend sitting immediately east of the existing blocks.

Between Block 1 and Block 2 sits a 3km zone that has never seen a drill bit - the exact geological setting where thicker, higher-grade heavy rare earth clay zones tend to develop.

MRD's entire rare earth discovery came from going back through old nickel-copper exploration data and recognising what earlier explorers had missed.

About 22,000 archived drill pulps are still sitting in storage, never assayed for rare earths, scandium or gallium.

If even a portion come back with decent grades, the resource grows without a single new hole in the ground.

The cost of sending those to a lab is a fraction of a new drilling campaign, and the company has already proven that approach works.

Drill planning and permitting is underway, with the 2026 targets set to be tested throughout the year. Most juniors at this stage have a maiden resource OR walk-up exploration upside. MRD has both.

Why These Commodities Matter Right Now

Each of these minerals has its own supply crisis, and MRD sits across all three. The detail on China’s controls and the price moves is covered above.

Here’s what sharpens the picture even further:

Heavy Rare Earths

From January 2027, US defence procurement rules tighten so that permanent magnets used in defence systems cannot contain material mined, refined or processed anywhere in a restricted supply chain, effectively forcing contractors to verify the origin of elements like dysprosium and terbium.

The scramble for non-Chinese supply has a tight deadline.

There aren't many ASX-listed names with a JORC heavy rare earth resource in a tier-one jurisdiction. When that deadline lands, the pool of projects that Western governments can actually back is a lot smaller than most people think

Scandium

Aerospace modelling suggests scandium-aluminium alloys could deliver around US$9 million in lifetime fuel savings for a narrow-body aircraft, based on higher-loading alloy scenarios.

At CES 2026, humanoid robot manufacturers debuted platforms built on scandium-aluminium frames. The use cases are expanding while global supply sits at 25 tonnes a year.

And yet almost nobody produces the stuff. The entire world makes 25 tonnes a year. MRD is sitting on 18,855 tonnes.

Gallium

At US$300 per kilogram with the GaN semiconductor market growing at 27% a year, gallium carries real by-product value on top of MRD’s rare earth and scandium economics.

MRD’s contained gallium of 24,584 tonnes represents about 34 years of current world production.

MRD's contained gallium of 24,584 tonnes represents about 34 years of current world production. Canberra has already put A$200 million behind a gallium processing plant at Alcoa's Wagerup refinery in WA, backed by Washington and Tokyo.

Gallium is near the top of every allied government's shopping list right now.

Five Reasons We’re Backing Mount Ridley Mines (ASX: MRD)

1. Three Strategic Commodities at $31.9 Million

We can’t find another ASX-listed company with JORC resources in heavy rare earths, scandium and gallium from the same deposit. If one exists, we haven’t seen it.

At $31.9 million, the market is barely paying for one of these commodities, let alone all three.

The heavy rare earth resource alone - 44,610 tonnes of contained HREO including 4,272 tonnes of dysprosium and 719 tonnes of terbium at a time when European prices have quadrupled - would justify exploration interest as a standalone project.

Then you add a scandium resource at ~US$3,500 per kilogram oxide and 24,584 tonnes of gallium. The combined in-ground value dwarfs the current market cap, even if you apply heavy discounts for stage and recovery.

We’re always looking for companies where the market is pricing one commodity and missing the rest. MRD has three commodities and the market seems to be pricing none of them properly.

2. VTM at $180 Million vs MRD at $31.9 Million - Where Is the Upside?

This is the comparison that got us over the line.

Victory Metals (ASX: VTM) operates the North Stanmore project at Cue in Western Australia. They describe it as Australia’s largest clay-hosted heavy rare earth project and carry a market capitalisation of roughly $180 million.

Here’s how they stack up against MRD’s maiden resource and what MRD has in the ground:

VTM currently has a larger tonnage in its rare earth resource at 321 million tonnes. But MRD’s maiden resource covers roughly 15 kilometres of a 63-kilometre corridor with 80% of the tenure untested.

Seven primary gravity targets are already defined, covering 33 kilometres of untested strike. The resource has clear room to grow and the company is funded to begin testing it.

On the HREE ratio, MRD’s 41% compares well with VTM’s 39% average. And MRD carries gallium and scandium on top - two strategic commodities VTM has not reported - plus a bilateral partnership with a US nuclear laboratory.

At $31.9 million versus $180 million, MRD trades at about 18 cents in the dollar relative to its nearest comparable, before adjusting for gallium, scandium or the Livermore partnership.

Even applying a 50% discount for MRD’s earlier stage and smaller current REE resource, the implied market cap sits around $90 million.

The upside from here comes down to two things: growing the resource and proving you can get the minerals out of the ground. MRD will be working on both throughout 2026, and if the results land, $31.9 million is going to look cheap in hindsight.

3. Lawrence Livermore - A Partnership With No ASX Peer

Lawrence Livermore National Laboratory (LLNL) is one of three US nuclear security laboratories. It was founded in 1952 and runs on a US$3.7 billion annual budget with 9,340 staff.

In December 2022, it achieved the first demonstration of nuclear fusion ignition in a laboratory. It is one of the highest-credentialed scientific institutions on the planet.

MRD signed a Material Transfer Agreement (MTA) with them in late 2025. Under the MTA, MRD shipped Block 1 core rejects to the laboratory.

A follow-up batch of approximately 200 kilograms has been prepared. The full Cooperative Research and Development Agreement (CRADA) is being drafted now. The scope covers working out exactly how to extract MRD’s rare earths, scandium and gallium efficiently, tailored to the specific chemistry of this deposit.

That kind of tailored process engineering would normally cost anywhere from $5-20 million through commercial consultants. And under the CRADA, MRD owns all the IP that comes out of the program.

That matters because China doesn’t just control the rare earth deposits - they control the processing. Even projects sitting on US soil still ship their ore to China to get it refined. Developing your own extraction flowsheet, outside that supply chain, is the whole game.

MRD is the only ASX-listed critical mineral company progressing toward a CRADA with Livermore. In FY2024, LLNL had 59 active CRADAs across the entire laboratory, out of 9,340 scientists and engineers. Livermore picked MRD’s ore because it contains the exact heavy rare earths the Pentagon is stockpiling.

LLNL has committed to advocate to the US Department of Energy for funding on MRD’s behalf. The precedent is Lynas Rare Earths (ASX: LYC), which received approximately US$250 million in US government support for its Houston heavy rare earth processing facility.

Lynas got that money because its supply chain fed directly into US defence contractors. MRD’s HREE resource, rich in dysprosium and terbium, sits in the same lane, at a time when the Australia-US Critical Minerals Framework is funnelling money into exactly these kinds of projects.

4. The 2026 Calendar Is Stacked

MRD has more near-term catalysts than most juniors at this stage get in years. Here's what we're watching:

The maiden resource itself is the first catalyst. Today’s JORC-compliant heavy rare earth resource of 122.56 million tonnes with a 41% HREO ratio, landing at a time when dysprosium and terbium are under Chinese export controls and European prices are at multiples of domestic, gives the market a concrete number to value against peers.

Re-assay of some 22,000 archived drill pulps - the cheapest way to grow a resource without drilling a metre. MRD's entire rare earth discovery came from re-examining old data, and the same approach across the broader tenure could define new targets at minimal cost.

Resource expansion drilling across seven gravity targets covering 33 kilometres of untested strike. The 3-kilometre gap between Block 1 and Block 2 - a structural dilation zone where thicker, higher-grade heavy rare earth clay zones tend to develop - is a particularly interesting target.

The CRADA with Lawrence Livermore is being drafted. Once executed, expect an ASX announcement. The 200kg follow-up sample batch is already prepared.

Metallurgical testwork on combined recovery of rare earths, scandium and gallium from the same process. Early testwork has shown that heavy rare earths leach more strongly than light rare earths in MRD’s regolith, which is just what you want to see - the highest-value elements come out first. Strong met results here would be a major value catalyst. The goal by year-end is a proof of concept - a mixed rare earth carbonate or individual metal oxides that demonstrate the process actually works.

Permitting is underway with a year-end 2026 target. The near-surface, free-dig nature of the deposit means a simpler approvals path than a hard-rock project.

All of this is landing in a market where heavy rare earth prices are surging under Chinese export controls and Western governments are throwing money at securing new supply.

5. The Policy Tailwinds are Real and Getting Stronger

MRD’s timing lines up with a wave of government money flowing into just the kind of project it’s building.

The US and Australia have committed up to US$8.5 billion between them to back Australian critical minerals projects. The Australian government has already backed a A$200 million gallium plant at Alcoa’s Wagerup refinery, with US and Japanese money alongside it.

The US Defence Production Act Title III - the same funding mechanism used to fast-track supply chains during wartime - is open to critical mineral projects, and MRD's CEO Allister Caird has flagged it as a viable route for the company.

A WA-based project that’s 25km from the deep sea port at Esperance with a resource spanning the exact heavy rare earths, scandium and gallium that both governments have identified as strategic priorities fits the framework like a glove.

And the pressure from China's side keeps building. The gallium export ban suspension expires in November 2026. Heavy rare earth export controls were added in April 2025. The trend is one-way, and every escalation from Beijing makes projects like MRD more important to Washington and Canberra.

The board has also recently strengthened with the appointment of experienced chairman David Wall, who brings the corporate experience to help take MRD from explorer to the next stage.

Our View

We spend a lot of time looking at small-cap resource companies. Many of them have one commodity and a market cap that already reflects the best-case scenario. MRD is the opposite.

Three critical minerals from the same deposit, a maiden resource that covers barely a quarter of the corridor, a partnership with one of the most serious laboratories on the planet, and a $31.9 million price tag. At a time when Western governments are falling over themselves to fund non-Chinese supply of exactly these materials.

We’re in because this looks mis-priced to us. The nearest comparable trades at $180 million with one commodity. MRD has three.

The risk with any junior is that the story sounds better than the ground delivers. We know that. Early-stage exploration can disappoint, met work can throw up problems, and timelines always slip. That’s the game.

But we like what we’re looking at. The catalysts are lined up, the commodity tailwinds are blowing hard, the Livermore partnership has no ASX peer, and $31.9 million looks light for what's in the ground.

We're backing MRD and we'll be all over this one throughout 2026.