Weekly Wrap: $100 Billion Gone, the Strait of Hormuz Shut, and Oil at US$92

Markets whipsaw as geopolitical risk returns, sending petrol prices higher and shaking commodities

If you haven't filled up the car yet, brace yourself.

Brent crude surged roughly 28% this week to around US$92 a barrel. Some servos in Sydney jumped nearly 60 cents a litre in the space of a few days, and economists reckon the full impact of the oil price move hasn't hit the pump yet - saying another 36 cents a litre could be days away.

The war in Iran has done what wars in the Middle East always do to commodity markets - made everything move at once. Everything except the Strait of Hormuz.

The ASX lost $100 billion in five days, gold spiked and gave it back, and oil posted its biggest weekly gain in the history of futures trading.

Away from the chaos, FMR is drilling again in Chile, a new Perth Basin gas play we like has listed quietly on the ASX, and lithium has taken another hit.

What caught our eye this week:

The ASX takes its worst beating in over a year, $100 billion wiped off

Gold steadies after rocketing then pulling back

Oil and gas markets come back to life, what it means for Australians

A small-cap gas play with big potential in the Perth Basin

FMR turns the drill bit in Chile as the hunt for copper continues

Weak EV sales send another jolt through lithium

The ASX’s Worst Week in Over a Year

The S&P/ASX 200 fell roughly 3% for the week, finishing around 8,850 points. It was the market’s biggest weekly loss in recent memory as investors looked to cut risk, and nobody was spared - BHP was down over 7%, RIO down 5%, and ANZ down 5%.

It wasn’t just the ASX. London’s FTSE copped the worst of it globally, down over 5% for the week, while in the US, the S&P 500 fell around 2%.

The one that raised eyebrows was Woodside, which barely moved despite oil surging 28%. In a normal week, crude at US$92 would have energy producers flying. Right now, investors are selling first and asking questions later, regardless of what’s sitting on the balance sheet.

The ASX was hitting record highs week on week before bombs started falling on Tehran. A quick return to those levels looks unlikely while the Strait of Hormuz is shut and Trump is demanding unconditional surrender from Iran. Reports are shifting by the hour, and until there’s more clarity, expect the volatility to stick around.

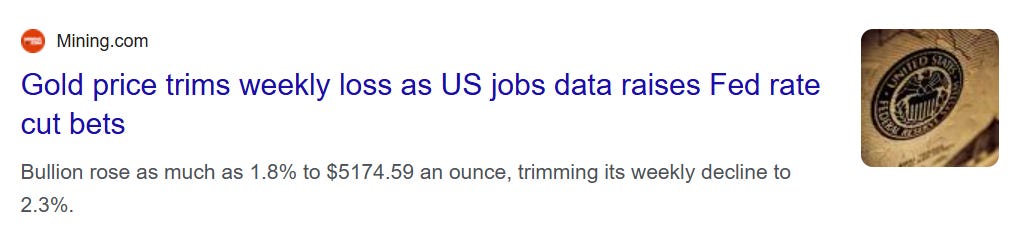

Gold Spikes, Then Gives it Back

Gold briefly punched above US$5,400/oz early in the week as safe-haven buying kicked in.

It didn’t last. Profit-taking pulled the price back to around US$5,037/oz within a couple of days, with stronger US inflation expectations and the prospect of higher-for-longer rates keeping a lid on the bounce.

The ASX producers copped it both ways - up on Monday, hammered by Friday:

Northern Star (ASX: NST) hit an all-time high of $31.95 before closing the week down 13%

Evolution Mining (ASX: EVN) touched $17.75, also a record, before finishing down 13.5%

Perseus Mining (ASX: PRU) held up slightly better, down 9%

After a run that’s taken gold from US$2,600 to above US$5,000 in about 18 months, plenty of investors used the spike as a chance to lock in gains. We don’t blame them.

Gold finished the week lower for the first time in five weeks, but still sits near US$5,200/oz. At that level, it's still one of the strongest gold markets in history.

J.P. Morgan's US$6,300 target from a few weeks back looked ambitious at the time. With a war in the Gulf, it might start to look conservative soon.

When the big producers sell off like this while the underlying commodity stays strong, capital tends to eventually find its way into the juniors as investors look for cheaper leverage to the gold price.

We’ve backed Black Horse Mining (ASX: BHL), which is waiting on results from its maiden drill campaign at a historic Victorian gold mine, and Exultant Mining (ASX: 10X), who is drilling in the coming weeks.

Both are drilling into a gold market that keeps rewarding anyone with ounces in the ground.

Oil and Gas Back in the Spotlight

We wrote last week that oil closed Friday at US$73 and wouldn't open there on Monday. It didn't. Brent posted its biggest weekly gain since the pandemic, finishing up 28% at around US$92/b. WTI went further, up 36% for its biggest week since futures trading began in 1983.

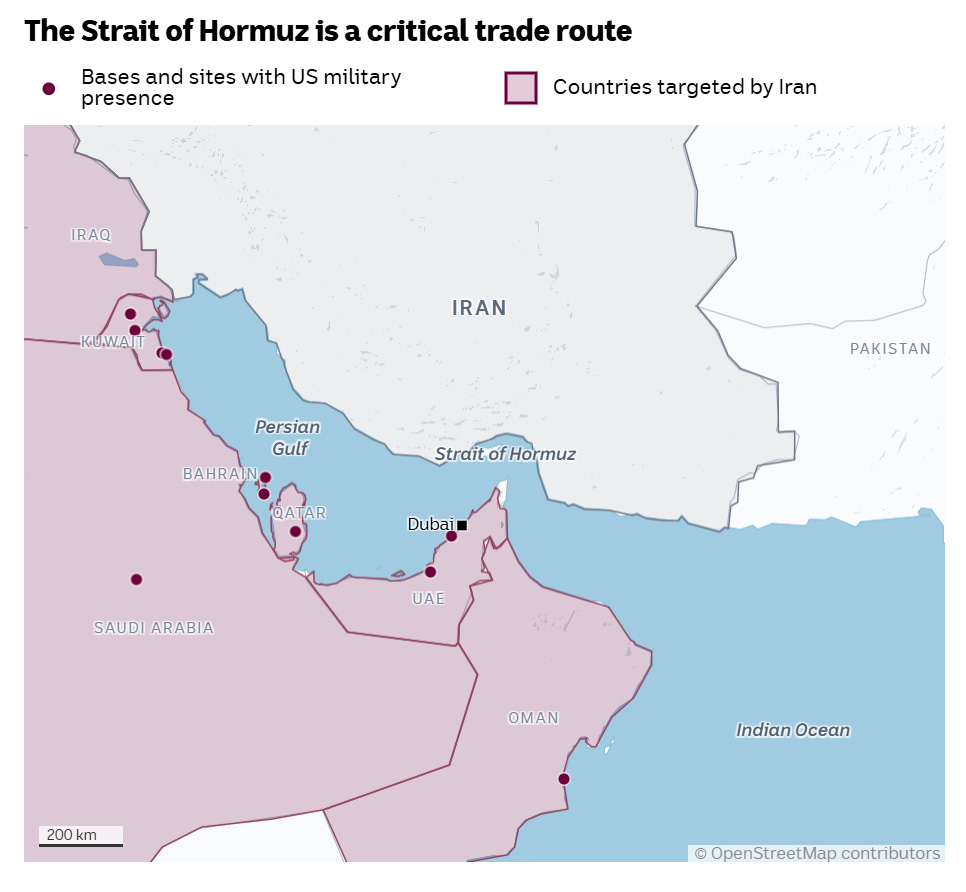

The Ayatollah is dead, his son is the frontrunner to replace him, and Iran's ability to fire back is fading fast. But the IRGC is still intact, and nobody in Washington seems sure whether the endgame is destroying Iran's missiles or changing the regime (or both).

For commodity markets, the military detail matters less than one simple fact: the Strait of Hormuz carries roughly 20% of the world's oil and LNG, and right now almost nothing is moving through it. The US is saying the strait is open. Iran is saying it isn't. Ship movements have reportedly all but stopped. Somewhere in the middle is the actual situation, and markets are pricing in the worst case.

Qatar shut down its main LNG export hub after Iranian drone strikes hit the facility, declaring force majeure (essentially pausing contractual deliveries because of the war).

That single plant accounts for about 20% of global LNG supply. European gas futures have roughly doubled in a week.

Iraq has started shutting in production at Rumaila, its biggest oil field, because there’s nowhere to send the crude that was supposed to leave through Hormuz. Those cuts have already passed 1.5 million barrels a day, with more fields expected to follow.

Overnight, Kuwait has declared force majeure on oil sales after running out of storage space - the second Gulf producer this week to tell buyers it can't deliver.

Polymarket is pricing a 54% chance of oil passing US$110/b this month, which would be the first time since 2022.

We said last week we weren't going to pretend we know how this plays out, and that still holds. Iran's missile stocks are reportedly running low, but there's no sign the US or Israel are slowing down. Israel struck fuel depots around Tehran overnight, and Netanyahu says there are "many more targets" to go.

But the shooting stopping and oil flowing again are two very different things, and the second one is what matters for prices.

Every day the Strait stays shut, the pressure on oil, gas and shipping compounds.

For Australian LNG producers, higher prices mean bigger margins on the roughly 70% of our gas that gets exported. For everyone else, it means higher bills - our domestic gas market has been tied to international pricing since the export boom of the 2010s, so when global prices spike, we cop it too.

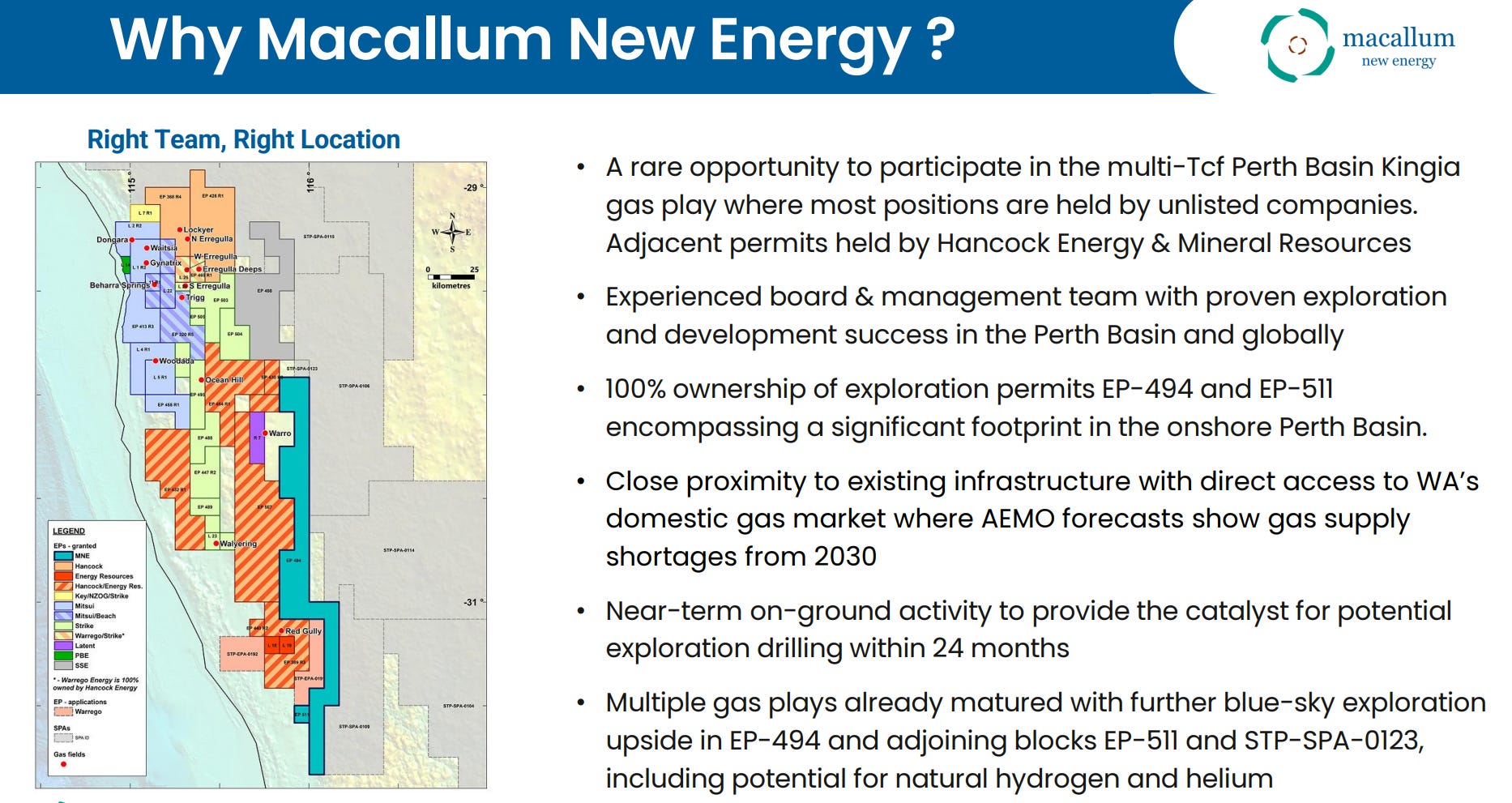

A New Small-Cap Energy Play in the Right Place

You’d be hard-pressed to pick a better couple of weeks to bring a gas company to market.

Macallum New Energy (ASX: MNE) hit the ASX last Wednesday IPO-ing at 20 cents a share with a $28 million market cap, with over $7 million cash. Just over a week later and the share price is sitting at 21.5 cents.

MNE holds two exploration permits, EP-494 and EP-511, in the Perth Basin, the same patch of ground that serious money has already been thrown at:

Mitsui paid $600 million for the Waitsia gas project in 2018

Hancock Prospecting dropped $1.13 billion on two permits in 2024

That’s just over $1.6 billion of corporate money chasing gas in a basin that already has pipelines and processing infrastructure sitting there waiting.

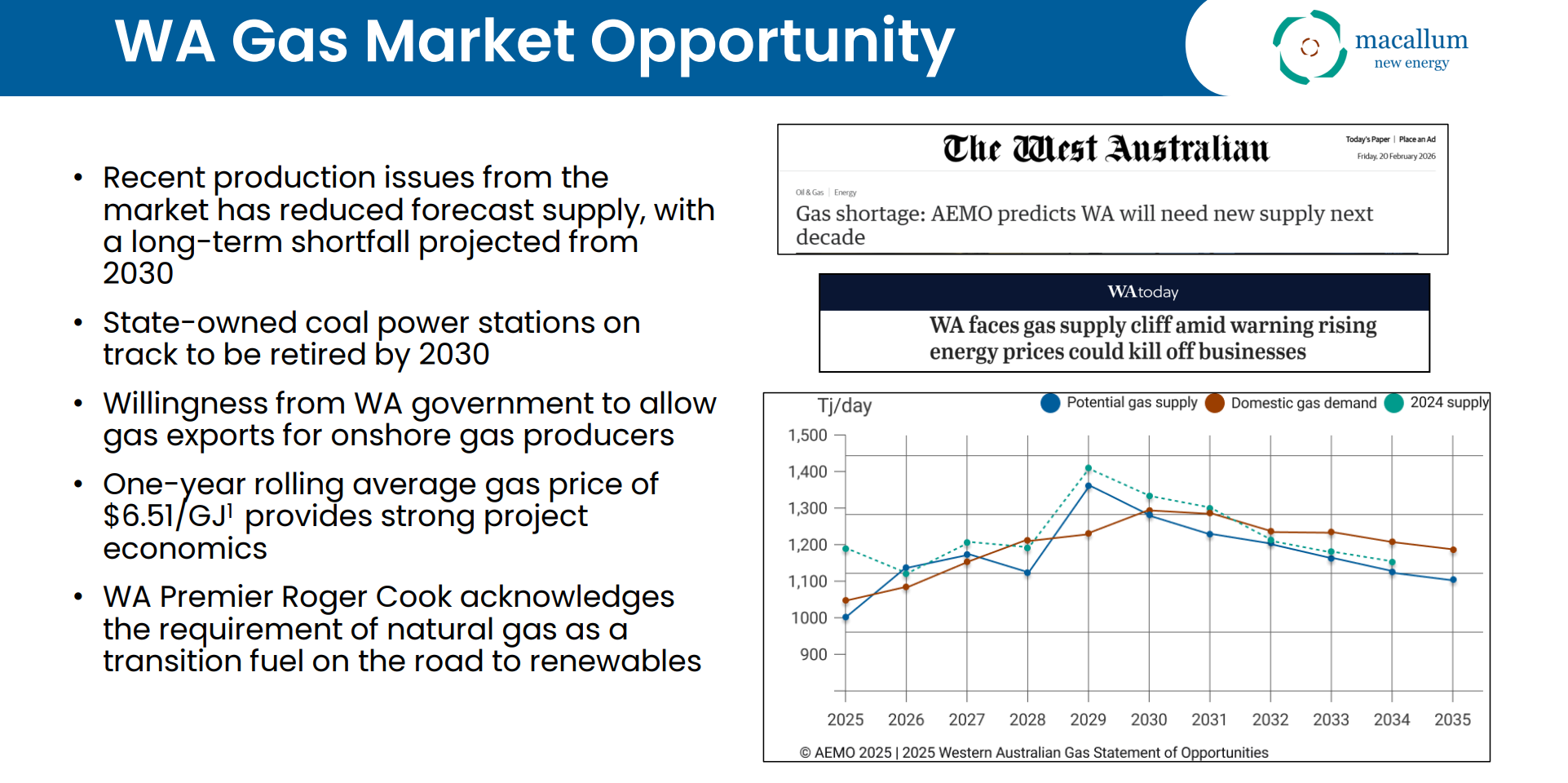

The Perth Basin has delivered some of the country’s most important onshore gas discoveries in recent years, and bigger players keep circling as Western Australia’s domestic supply tightens.

MNE CEO Andy Furniss was part of the AWE exploration team behind the Waitsia gas discovery in the Perth Basin, one of Australia’s largest onshore gas finds in recent decades. He spent over two decades between Chevron, AWE and Mitsui before taking the CEO role on at MNE, and chair Phil Thick came through Shell. It’s a deep bench for a $28 million micro-cap.

MNE is pure exploration at this stage, and a long way from proving anything up. But the basin has form, the people running it have found gas here before, and the impending energy crunch will continue to highlight LNG demand for years to come.

FMR Back Drilling in Chile

FMR Resources (ASX: FMR) has kicked off its fourth drill hole at the Southern Porphyry target in Chile, going after Target L within the Llahuin corridor.

This one is aimed at what FMR believes is the core of the copper-molybdenum porphyry system.

Earlier drilling confirmed the company is already within the broader mineralised footprint, hitting multiple porphyry phases with quartz-sulphide veining and disseminated chalcopyrite and molybdenite.

Each hole has helped narrow down where the heart of this system sits, with structural and geochemical data now pointing south and east.

Target L is planned to around 1,200 metres and is the next step toward testing the main porphyry source within a six-kilometre mineralised corridor.

FMR has a management team that is better qualified than almost any comparable small-cap on the ASX.

At the end of the day though, the drill bit will do the talking.

If the results come back the way the geology suggests they should, the share price at sub-30 cents will be a distant memory.

Lithium Takes Another Hit

Lithium copped it again this week. China’s lithium carbonate futures dropped nearly 13% in a single session after weak EV sales numbers out of major manufacturers landed below expectations, and geopolitical tension clouded the demand outlook.

BYD, the world’s largest EV maker, posted combined January and February sales down roughly 36% year-on-year, which is a big miss for what has been the sector’s strongest growth story.

Then there's Stellantis. The parent company of Jeep, Ram, Peugeot, and Chrysler, reported a US$37 billion loss for 2025 after writing down its EV investments and rethinking its electrification strategy.

Stellantis had offtake agreements in place with a number of ASX-listed lithium companies, so the ripple effects from their pivot are real.

On the ASX, Pilbara Minerals (ASX: PLS), Liontown (ASX: LTR), IGO (ASX: IGO) and Mineral Resources (ASX: MIN) all finished the week down more than 5%.

We see this as a rough patch rather than the wheels falling off. The longer-term demand case for lithium is increasingly tied to battery energy storage systems, where analysts are forecasting strong growth over the next decade.

And if you drove home from the servo this morning $180 lighter and found yourself looking enviously at electric cars for the first time, you're probably not alone. If the war in Iran drags out and petrol stays anywhere near these levels, EV adoption gets a shove that no government subsidy could match. Funny how that works.

Where to From Here

It's been a rough week for the ASX, but the damage has been concentrated at the top.

The big end of town has copped the worst of it, and that probably continues while the Strait stays shut and headlines keep shifting. But small-cap trading volumes have held up reasonably well through the week, which tells us this is a sell-off driven by macro fear at the top rather than panic across the board.

Our portfolio companies are all mid-program or approaching catalysts. FMR is drilling in Chile, BHL and 10X are both approaching results, and FUN is building toward a maiden resource. None of that changes because of what’s happening in Tehran.

We’ll be watching the oil price closely when markets open Monday (and Trump’s Truth Social feed). If crude pushes past US$100 as forecasted, this stops being a short-term disruption. Sustainably high oil prices reshape energy markets and inflation expectations for months.

Till next week.