Weekly Wrap: $500M Gone by Lunch, Mitsui Locks Up Rutile, and NST Cops Another Downgrade

A biotech blowup, a third gold downgrade, and three portfolio companies with news this week

A biotech lost 90% of its value before lunch on Friday. One failed trial result, and half a billion dollars from the company’s valuation gone.

If you’ve been in the market long enough, you’ve watched it happen to someone. Maybe it’s happened to you. It’s the kind of morning that makes you stare at the screen and rethink every position in your portfolio. It’s a brutal reminder of why risk management matters.

It wasn’t the only chaos on the ASX this week. The ASX 200 was down 2%, it then rallied 4%, only to finish roughly where it started. Much of the panic selling washed out last week, but with the war in Iran escalating and the Strait of Hormuz still shut (depending on who you ask), volumes have thinned out. Traders are sitting on their hands while oil stays above US$100 and the next headline could move it $10 in either direction.

Plenty still happened underneath the surface. Fresh drill results from two portfolio companies, a Mongolian copper project quietly changing hands, Australia’s biggest gold producer copping another downgrade, and lithium creeping back into favour.

Here’s what caught our eye:

FUN’s corridor gets another tick as Mitsui locks up SVM rutile offtake

BHL’s maiden drill results confirm gold at Mt Egerton

Oil above US$103 as Strait of Hormuz updates change by the hour

AZ9 locks in 100% of the copper-gold project Maikhan Uul

Immutep drops 89% after scrapping its lead cancer drug

Northern Star cops its third downgrade in six months

Wood Mac are bullish on lithium over the next decade

FUN: The Corridor Gets Another Tick

Over 70% of the world’s biggest rutile deposit just got spoken for, and the mine hasn’t even been built yet.

Sovereign Metals (ASX: SVM) signed an offtake MOU with Mitsui on Thursday for 70,000 tonnes per annum of rutile from its Kasiya project in Malawi, covering roughly 31.5% of planned output. Major share holder in SVM, Rio Tinto, already holds rights to another 40%.

Add in Traxys locking up Kasiya’s graphite last month, and you’ve got three of the heaviest names in global commodities all circling the same patch of Malawi.

Our portfolio company Fortuna Metals (ASX: FUN) sits 20 kilometres south of SVM’s Kasiya on the same geological formation, with the same near-surface rutile mineralisation. SVM is worth around A$540 million. Fortuna trades at roughly A$22 million.

FUN dropped another batch of drill results from Mkanda earlier this week. 40 new holes, high-grade rutile from surface, and most holes still in mineralisation when the drill stopped. Best intercepts included 8m at 1.15% rutile and 10m at 0.89% rutile.

We published a full deep dive on Wednesday if you want the detail.

The drill results are one half of the FUN story. The other half is who’s going to need all this rutile.

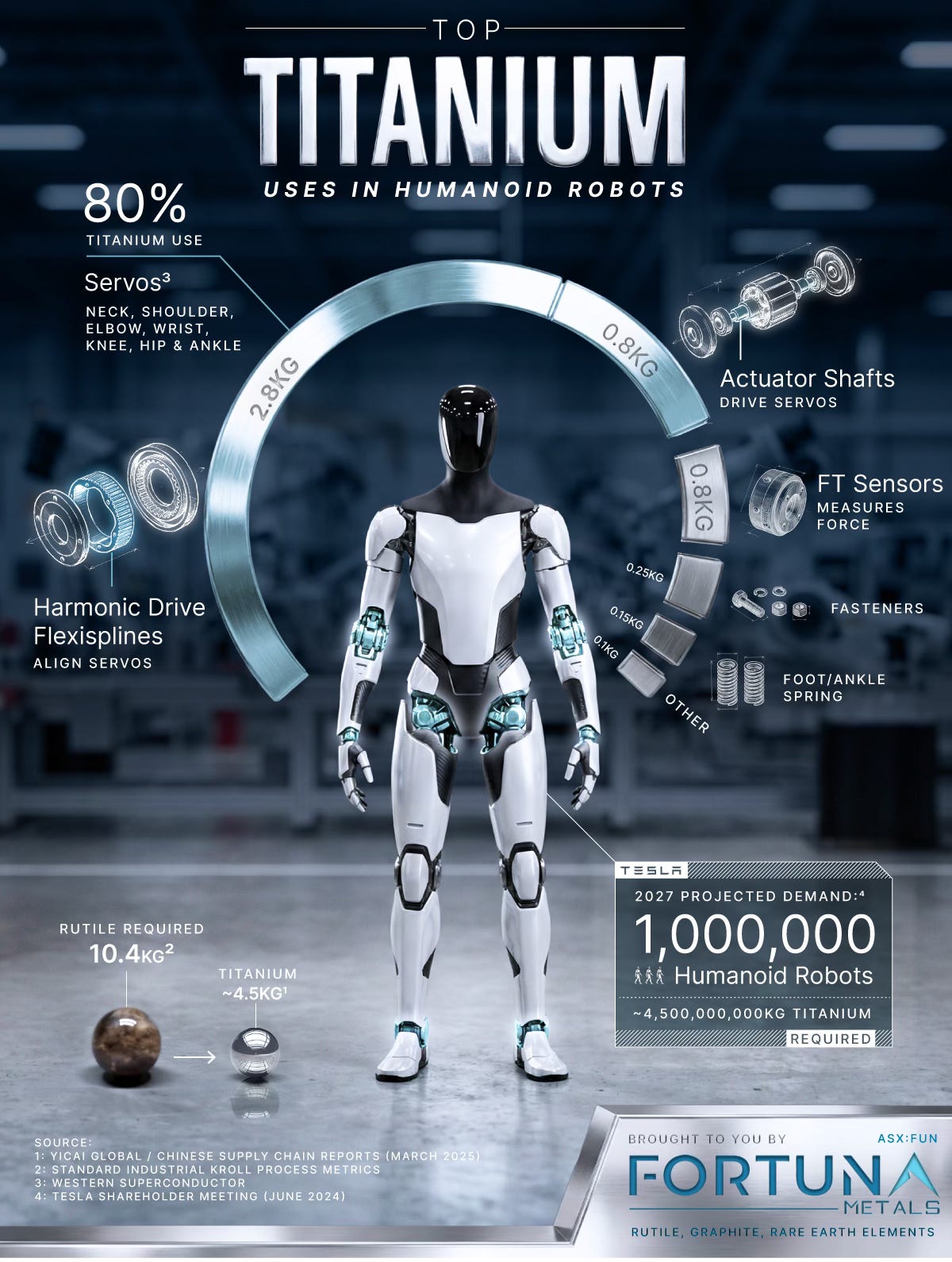

Twelve months ago, humanoid robots on factory floors sounded like science fiction. They’re now assembling cars in Beijing, Leipzig and Fremont.

Elon Musk has been building a humanoid robot called Optimus at Tesla for the past few years. On Thursday he said Optimus 3 is nearly finished and that “nothing’s even close” to what they’ve built.

Production starts within months, with high-volume manufacturing expected by mid-2027. Tesla has already shut down two car lines at its Fremont factory to make room.

He also reckons the market for humanoid robots will exceed 10 billion units, more than the number of humans on earth.

If only one percent of Musk’s predictíon come true, that’s still 100 million robots.

You can’t build a humanoid robot without titanium. The joints and load-bearing components need titanium alloys because nothing else survives the stress at that weight. And the cleanest, fastest way to make titanium is from natural rutile.

Each robot requires an estimated 10.4 kilograms of rutile. The US imports 100% of its titanium and legacy producers are in decline.

FUN has months of newsflow ahead. An exploration target lands by end of month, aircore drilling kicks off in May, and the company is targeting a maiden inferred resource by September. There are still 485 full hole assays and 300 shallow samples sitting in labs waiting to come back.

At A$22 million, with SVM worth A$540 million 20 kilometres up the road, we reckon that gap closes a lot faster than the market expects.

BHL: Maiden Drill Results Confirm the Gold

We called Black Horse Mining (ASX: BHL) our 2025 Small-Cap of the Year in December. The first drill results from Mt Egerton are in, and the gold system is real.

The standout hole hit a mineralised zone over 5.2 metres from 55 metres downhole, with assays returning up to 17.4g/t gold. Core recovery was patchy through the zone, which means the true grade is probably higher than what the lab reported because the gaps were treated as containing zero gold.

Another hole targeted a historic high-grade intercept of 7m at 18g/t and hit a void at the target depth, confirming the old underground workings are exactly where the records say they are. If the old data is reliable, the team can target the next round of holes with real confidence.

We believe the spur veins mentioned deserve a lot more attention. A camera lowered into one of the voids filmed visible quartz veins branching off the main reef structure.

In the Bendigo-Ballarat goldfields, spur veins carry gold, and a nearby historic hole returned 10m at 6.38g/t from the same type of structure. It means the gold-bearing system at Mt Egerton could be much wider than a single reef line. That’s a bigger target than anyone mapped going in.

The share price has pulled back since the results landed. Maiden results from a hyped IPO will almost always get sold unless they’re spectacular, and 17.4g/t is a strong hit but patchy core recovery muddied the headline. The market wants clean numbers it can model.

The results are good for a first pass at a project that hasn’t been drilled in over a century. But “good for a first pass” and “enough to excite a market that priced in a discovery” are two different things.

BHL has drilled about 500 metres so far. Mt Egerton produced 1.29 million ounces at 12 grams per tonne before water shut it down in 1906, and more than 90% of all historic drilling stopped above 150 metres.

A larger rig capable of drilling to 1,000 metres is being mobilised now, with deeper drilling starting by end of March. The bigger core size should also fix the recovery issues from this first program.

At 29.5 cents and a market cap around $25 million we think the sell-off has priced in the disappointment without pricing in what the program actually found. Gold confirmed, old data validated, spur veins opening up a wider target.

The real test at Mt Egerton starts when the deeper holes go in. We’re holding every share.

Oil Above US$103 and Still No Clear End

Two weeks into the Iran war and the Strait of Hormuz is still closed. That single fact matters more than anything else happening on the battlefield.

About 20% of the world’s oil normally passes through that narrow channel between Iran and Oman. Right now, almost none of it is.

Brent crude settled above US$100 a barrel on Thursday. The International Energy Agency called it the largest supply disruption in the history of the global oil market. That’s a sentence worth reading twice.

The war continues to weigh on global markets. The ASX 200 finished the week at 8,617, dragged lower by the same uncertainty that’s kept a lid on equities since the bombs started falling two weeks ago.

People keep asking when the Strait reopens. Iran said this morning it’s open to everyone except the US and Israel, but words are cheap at the moment. Until tankers are actually moving through safely, the blockade is still the blockade.

The longer answer involves understanding what’s actually keeping it shut. It’s insurance. Iran doesn’t need warships blocking the channel. Its drone and mine campaign pushed maritime insurance premiums so high that no commercial shipping company will send a tanker through, even on days when nothing gets hit. One or two attacks a week is enough to keep premiums at levels that make the maths impossible.

If you still don’t understand why one waterway has brought the global economy to a standstill, Javier Blas at Bloomberg put together a visual explainer this week that lays it out better than anything we’ve seen. Worth a few minutes of your time.

The US keeps saying it’ll reopen the Strait soon. Energy Secretary Chris Wright said on Thursday the Navy could start escorting tankers through by end of month. Two days earlier he posted on X that a tanker had already been escorted through. Oil dropped 17% in minutes. Then the post was deleted. The White House confirmed it never happened.

So the real timeline is: not yet, and nobody in charge agrees on when.

All three sides - the US, Iran and Israel - have publicly committed to goals that require the other sides to collapse. Trump wants unconditional surrender. Iran wants reparations and security guarantees. Netanyahu wants to keep striking until the regime breaks. None of those positions leave room for a ceasefire, which means there’s no timeline for when oil flows again. Markets hate that.

You’d think with the sStrait closed the big energy producers on the ASX would be soaring. It was quite the opposite this week with Woodside (ASX: WDS) and Santos (ASX: STO) down roughly 3% each.

Higher fuel costs are already feeding into inflation expectations. ANZ hiked fixed rates ahead of Tuesday’s RBA meeting, with most now above 6%.

Every day the Strait stays shut, the pressure compounds.

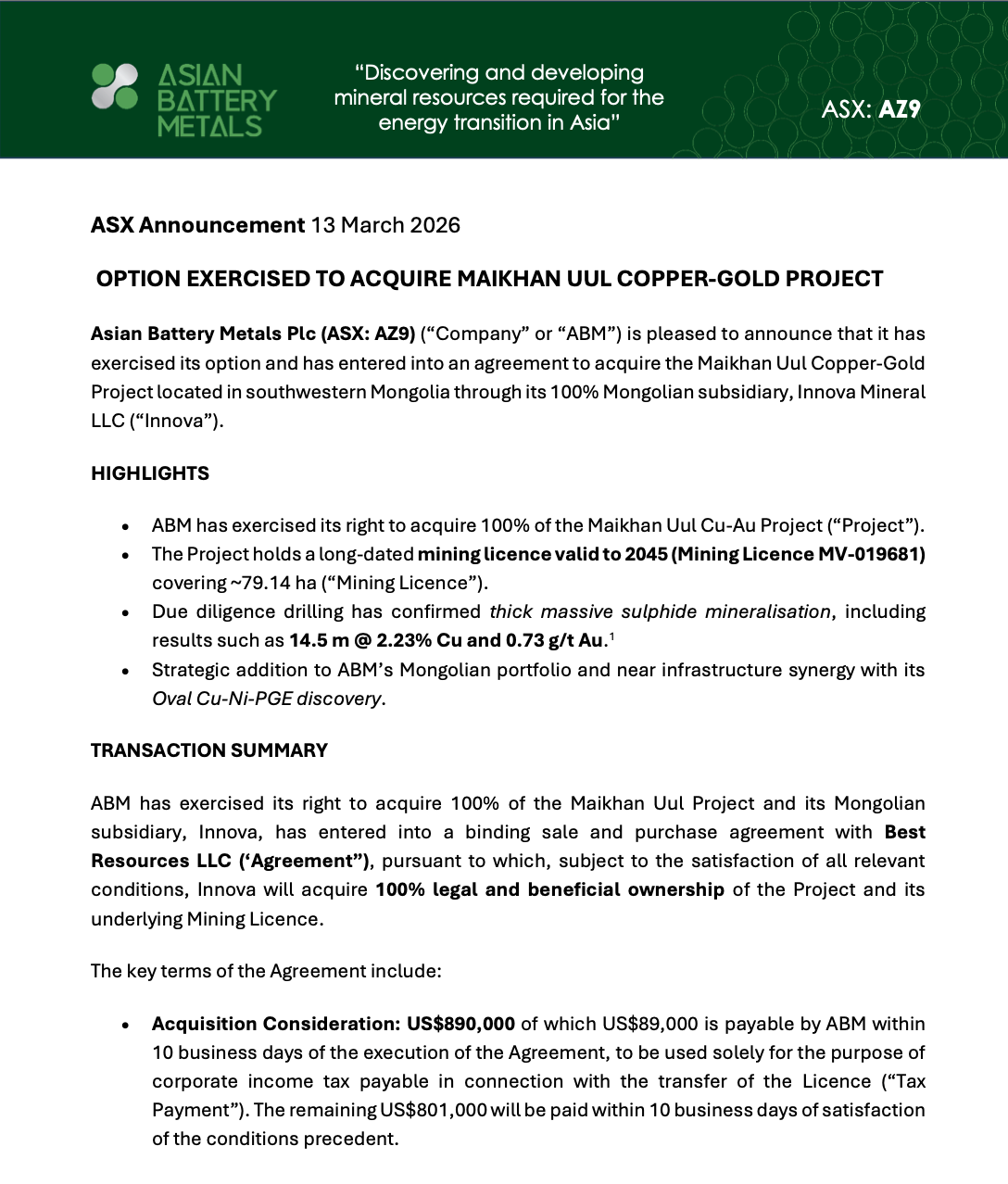

AZ9: Maikhan Uul Locked In

Asian Battery Metals (ASX: AZ9) has been quietly putting together a copper district in south-west Mongolia for the past eighteen months. On Friday, they locked in another piece.

AZ9 exercised its option to acquire 100% of the Maikhan Uul copper-gold project, paying US$890,000 for a granted mining licence that runs to 2045.

The company had spent the past six months drilling to verify old government data before committing. The data checked out.

Due diligence drilling returned 14.5m at 2.23% copper and 0.73g/t gold from thick massive sulphide, and a twin hole late last year pulled 20 metres of visible massive sulphide that sits outside the existing 5 million tonne resource boundary.

If assays confirm what the visuals suggest, AZ9 may have extended the copper system beyond what anyone had modelled.

Maikhan Uul sits eight kilometres from AZ9’s flagship Oval copper-nickel discovery, where drilling has confirmed mostly continuous mineralisation over 880 metres of strike with grades up to 6% copper and 3% nickel.

The two projects sit in the same volcanic belt, close enough to share infrastructure, and both keep hitting sulphides every time the drill turns.

An executive director at GBA Capital named AZ9 as their pick of the year in our Broker Black Book, calling it “poised for a re-rate” and pointing to the maiden JORC resource expected in 2026 as the catalyst.

With copper above US$11,000 a tonne and genuine new discoveries getting scarcer by the year, a company sitting on two copper systems in the same district is in a good spot.

At 2.5 cents and a market cap around $15 million, AZ9 now owns two copper systems within eight kilometres of each other, with assays from both still flowing through.

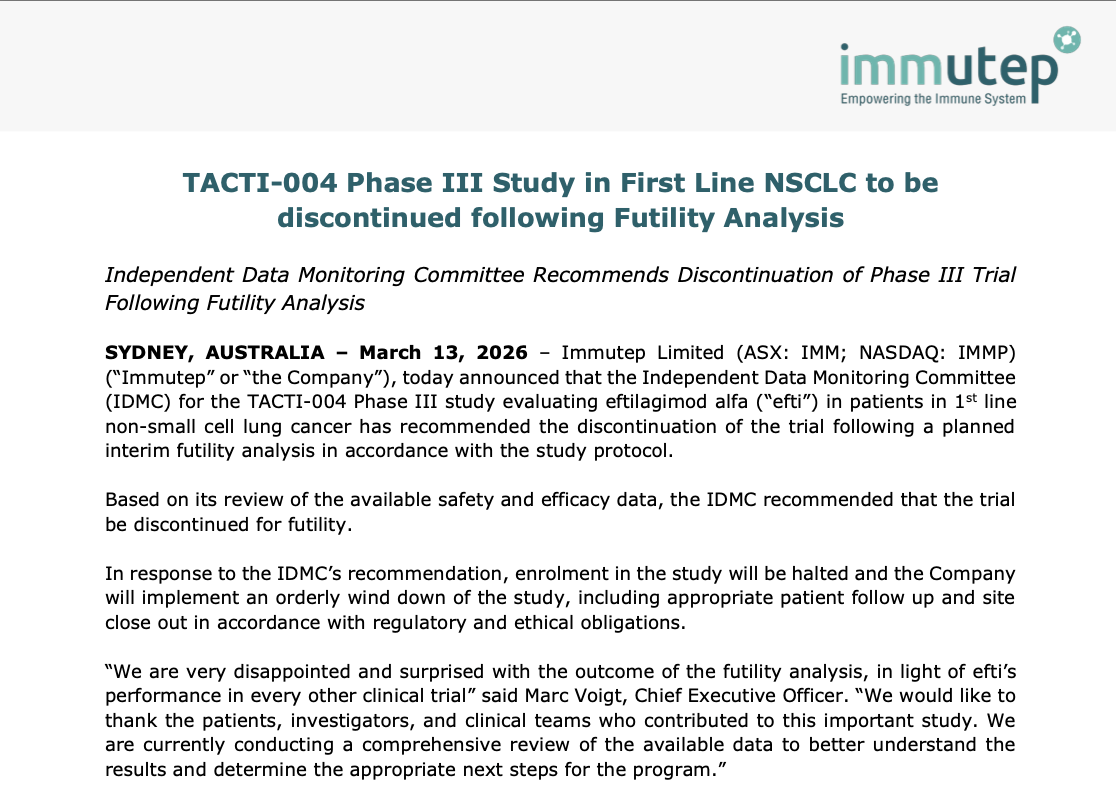

Immutep's $500 Million Wipeout

Half a billion dollars gone before lunch.

Immutep (ASX: IMM) came out of a trading halt on Friday and dropped 89%. A company worth $582 million the last time it traded closed the session at $56 million. Over 356 million shares changed hands.

The cause was a Phase 3 trial failure. Immutep’s lead drug Efti, a lung cancer therapy designed to work alongside Merck’s Keytruda, got scrapped on the recommendation of an independent review committee. Years of development, trials across 27 countries, and the whole thing came down to one sentence.

The stock had run 40% in December after Immutep signed a deal with Indian pharma giant Dr. Reddy’s to commercialise Efti. That gain and then some evaporated in the first few minutes of trade on Friday.

Immutep still has around $70 million in cash and other programs in the pipeline including treatments for breast cancer and autoimmune conditions. But Efti was the reason most people owned the stock, and Efti is done.

CEO Marc Voigt said the company was “very disappointed and surprised.” At 4.5 cents a share, the market has priced it at close to cash backing and not much else.

NST: Gold Boom, Mill Bust

Gold’s above US$5,000 but Australia’s biggest gold miner can’t get enough ounces out of the ground.

Northern Star (ASX: NST) dropped 19% on Friday after its third guidance downgrade in six months. The company now says production will land “above 1.5 million ounces” for the year. Back in July it was targeting up to 1.85 million. That’s a big miss in the best gold market most of us have ever seen.

The problem is the Super Pit’s ageing mill at KCGM in Kalgoorlie, which keeps breaking down and can’t hold throughput. A $1.5 billion replacement is on track to start commissioning in July, but until it’s running, Northern Star is stuck nursing a 37-year-old plant through its final months.

Jan and Feb gold sales came in at 220,000 ounces combined, well short of the run rate needed. Jundee, Northern Star’s other major WA gold operation, is also underperforming, with a cost review now underway to work out which ounces are still worth chasing.

CEO Stuart Tonkin told analysts the priority for the next four months is getting the new mill delivered on time, even if that means this year’s production numbers come in soft. The stock is down 31% in two weeks.

Northern Star sits on more than 70 million ounces of gold and the new mill will more than double processing capacity once it's running. The long-term story hasn't changed. But three downgrades in six months means the market won't give them the benefit of the doubt until the new plant is pouring gold.

Lithium Demand Heading for a Supply Crunch

Longer-term sentiment around lithium continues to improve after a new report from Wood Mackenzie said global lithium demand could exceed 13 million tonnes of lithium carbonate equivalent by 2050.

That’s the most bullish scenario and would require lithium supply to increase by over 700% from today’s roughly 1.6 million tonnes per annum.

The base-case scenario sits closer to 6 million tonnes per annum, still implying an increase of more than 300% from current production.

Under that base case, Wood Mackenzie estimates the industry will need up to US$114 billion in new investment to build the mines and processing plants required to meet that demand.

Bringing new supply online through exploration, permitting and construction, is likely to mean the biggest constraint is time. If investment doesn’t accelerate soon, the market could flip back into deficit by the end of the decade.

After two years of oversupply and falling prices, lithium’s bounce back may finally be underway. The next few years could see demand increase significantly, helping small-cap lithium come back into favour on the ASX.

What Comes Next

The market is stuck between two forces right now, and neither one is backing down.

Any escalation out of the Middle East sends oil higher and drags everything else lower. On the flip side, the US is set to meet with China this week, and if those discussions produce anything resembling de-escalation, markets will move up fast.

Outside of oil, most commodities are treading water. Gold, copper, silver, iron ore. All waiting for a catalyst or a clear direction. But markets keep moving through wars, and good drill results still get rewarded in any environment. This week proved the other side of that too. Bad results get punished, and they get punished quickly.

We're trading with caution from here. Volatility creates opportunity, but right now it cuts both ways.

Till next week.