Weekly Wrap: A Dead Coal Stock Revived, KTK Gets Paid and Europe's €120B Chip Bet

Defence, critical minerals and semiconductors dominated the week as capital flowed toward revenue, drilling success and strategic supply chains.

The Enhanced Games were meant to be one of the biggest sporting stories of the year. World records falling, wall-to-wall coverage, athletes free to take whatever they liked. The company behind it listed in New York at US$1.2 billion on exactly that pitch.

Then the gun went. One record fell all weekend, and a Greek swimmer set it clean. The juiced-up games limped out of the blocks.

The real action this week was a long way from Las Vegas. Across commodities, defence and tech, investors got a proper run of news. Europe drew a line in the sand on chips, and the lithium cheques came back out. The biggest mover of the lot was a coal stock that had been left for dead.

Closer to home, our portfolio kept ticking. Revenue landed, fresh samples came back, drills started turning and the big thematics gathered pace.

Let’s get to it.

KTK turns its IPO into revenue, fast

Humanoid robots start moving onto production lines

EVG returns high-grade fluorspar samples in Nevada

AZ9 keeps hitting massive sulphides at Red Hill

10X kicks off maiden drilling at Balerion

Europe’s €120 billion bid for chip independence

Coal pulls serious capital as a small-cap goes vertical

Lithium money keeps flowing at both ends of the market

KTEK: A Week From Bell to First Invoice

KTEK Aerosystems (ASX: KTK) rang the ASX bell less than a fortnight ago, and this week it shipped product and booked revenue against it.

Plenty of freshly listed small-caps are still all promise at this stage. KTK is already getting paid.

The first delivery since listing booked $500,000 in revenue.

KTK makes the parts that go inside drones, and leaves the job of bolting together finished aircraft to someone else. Governments are spending a fortune on drones already, and every budget you look at says they're about to spend far more. Actually winning those contracts, though, is a knife fight.

KTK sits that fight out.

Whichever drone-maker takes the tender, KTK's components are in the aircraft, and KTK gets paid either way.

Management is aiming for 150 units a month inside five months. On their own numbers that works out to around $9 million a year from customers KTK already has, before a dollar of the IPO money goes to work.

More Tier-1 contractors are being courted, and the “Cordless Factory” model, which lets KTK grow without pouring money into a factory of its own, keeps expanding.

Most early defence manufacturers never make it past the certification grind. KTK spent years clearing the audits and approvals to supply the people who build the drones, and this week that work started showing up as revenue that’s real and repeatable. It’s a big tick for a small-cap.

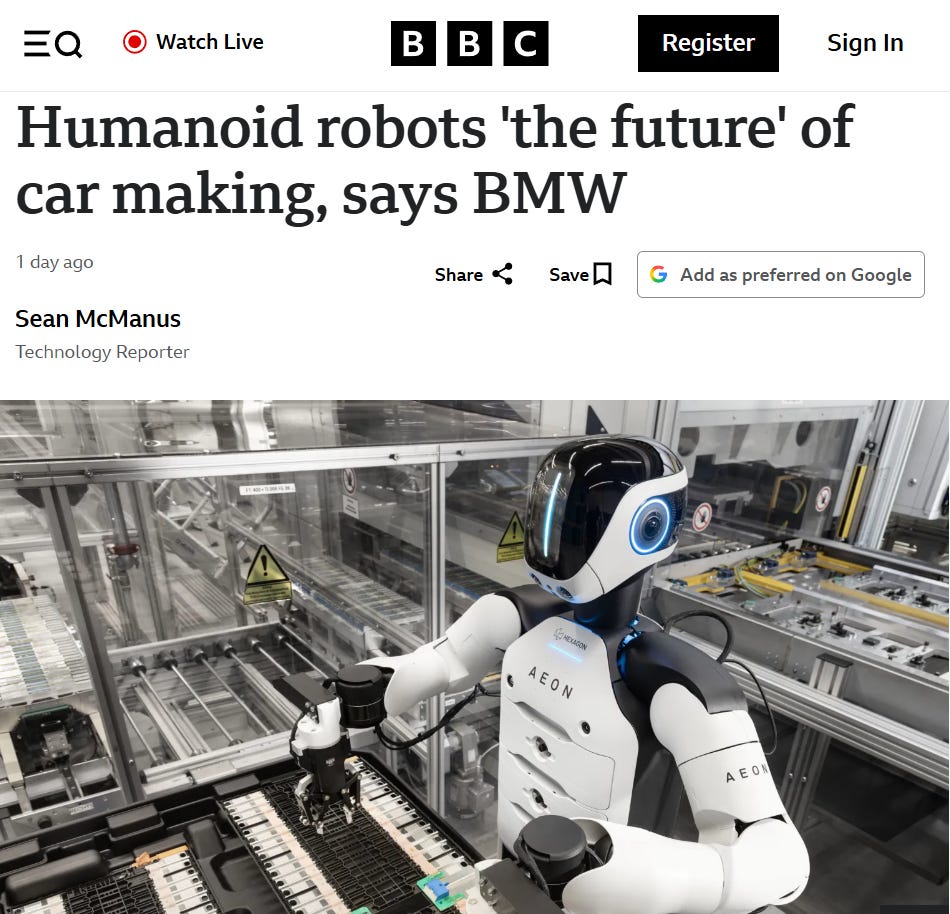

The Robots Are Real Now, and They Need Rutile

Fortuna Metals (ASX: FUN) is sitting at 13 cents and a market value of around $37 million, and one of the commodities it’s chasing through rutile could end up in the middle of one of the biggest manufacturing shifts of the next decade.

Humanoid robots have spent years feeling like tomorrow’s technology that never quite arrives. Every few months a video does the rounds of a robot pulling off a backflip, everyone gets excited, then it goes quiet again.

That’s now changing with BMW. The carmaker is putting humanoid robots onto its vehicle production lines, joining a run of global manufacturers already trialling human-shaped machines on the factory floor.

The thinking behind it is almost dull in its obviousness. Factories and warehouses were built for people, so rather than redesign every workplace around some purpose-built machine, you build a machine shaped like the worker the place was made for.

The military has landed in the same spot, trialling humanoids to haul supplies and drag wounded soldiers out of places you would not send a person.

Ukraine is already chasing tens of thousands of robotic systems this year as the tech moves from concept to the battlefield.

For investors, the question worth sitting with is what these machines are built from. Humanoids need lightweight, high-strength materials that can handle constant movement without chewing through power. Titanium sits near the top of that list.

Rutile is one of the key feedstocks for titanium.

The humanoid story is only getting bigger with some of the largest car makers, industrial names and defence groups in the world prioritising them.

Demand has to work its way back up the chain to the raw materials that make it all possible, and rutile is the very start of a humanoid.

10X Drills Ground the 90s Left Behind

The wait is over for Exultant Mining (ASX: 10X). Since it listed in December the company has been heads-down in soil sampling, IP and gravity surveys, building the case for where to put a rig.

This week one finally started turning at its Balerion Prospect in New South Wales.

Twelve holes, 3,425 metres of RC drilling, chasing copper, silver, lead, zinc and gold across ground that has already given up high-grade hits.

We've said before that discoveries are made long before the first hole goes down. The graft is in the data and the targeting. Now the theory meets the drill bit.

Two explorers drilled this ground in the 90s. One of them pulled 4.4 metres grading 342 grams of silver a tonne, lead and copper running with it.

Then they did the only sensible thing anyone could with metal prices where they were. They stopped drilling and left.

The grades stayed in the rock, and so did the fault underneath it, the same one that fed Captains Flat through 80 years as one of the biggest base metal mines NSW ever ran.

Cheap metal sent everyone home, and now expensive metal has brought the rig back.

The program is built to test it from several angles, soil chemistry, IP, gravity, magnetics and the old drilling all pointing at the same ground. It’s a campaign with several shots at a result.

At 18.5 cents, 10X is the smallest name in our portfolio. These are early days and a discovery is far from guaranteed, but for a company valued where 10X is, even one good hole brings a lot more eyes with it.

Drilling should run for the next four to six weeks, with assays coming back as they clear the lab.

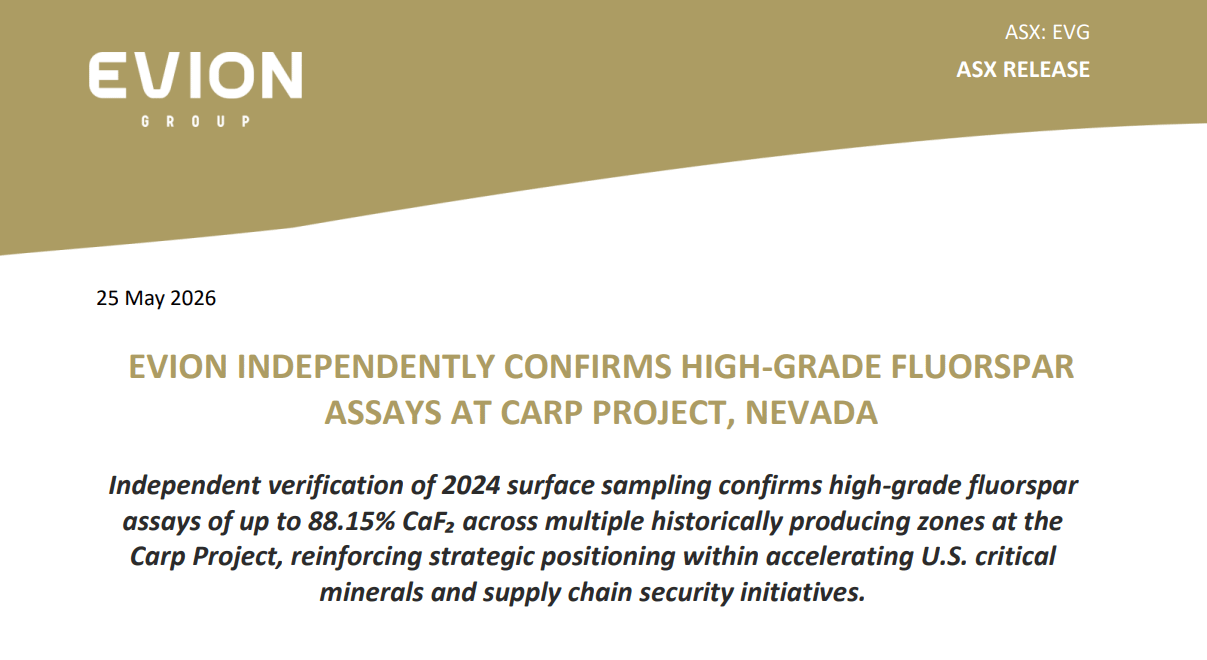

America Forgot About Fluorspar. It Remembers Now.

The US hasn’t pulled fluorspar out of its own ground since 1990. China makes around 59% of the world’s supply now.

For 35 years that suited everyone. The rock came cheap from somewhere else and nobody asked where.

In January the Pentagon wrote a US$168.9 million cheque to restart a single mine in Utah, rock grading 60 to 70%, just to get American supply moving again.

This week Evion Group's (ASX: EVG) Carp project in Nevada returned surface samples grading up to 88.15% calcium fluoride, independently verified, with several of the old mining areas clearing 80%. Higher-grade rock than the Utah mine the Pentagon just paid to reopen.

These are hand-picked surface samples, not what the whole deposit grades, and Carp still has to be drilled out. But for a project only recently added to our portfolio, it backs the geology management flagged when they picked it up.

Most investors never give fluorspar a second thought, yet it turns up in semiconductors, EV batteries, refrigerants and nuclear fuel processing.

The US imports all of what it uses despite getting through hundreds of thousands of tonnes a year, and that level of reliance is exactly what policymakers are now trying to unwind.

Carp was a producing mine once. The high-grade rock never left, and EVG now holds far more of the ground around it than when it first picked the project up.

With more than $7 million in the bank and a run of catalysts coming across Nevada, Madagascar and India, you’re starting to get a clearer read on where Evion wants to sit in the critical minerals supply chain.

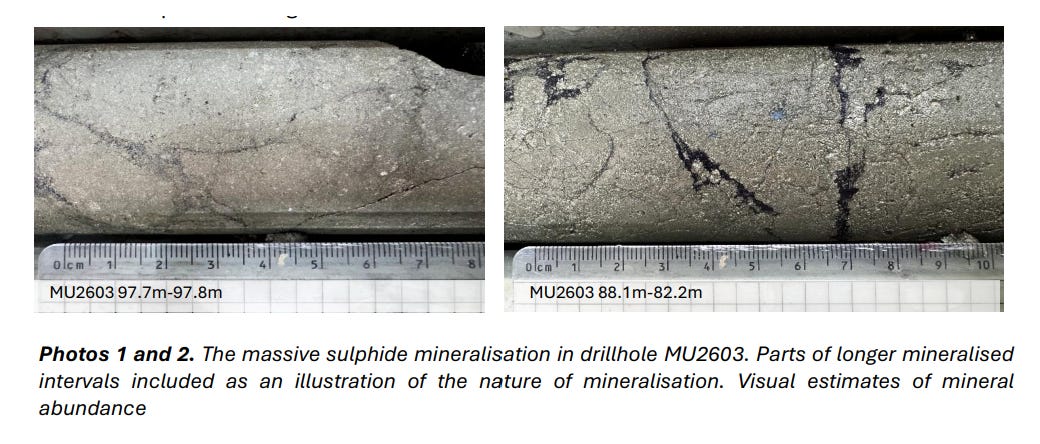

AZ9: Two Holes, Two Hits, and a Richer Copper

Asian Battery Metals (ASX: AZ9) has flown under the radar for much of the past year. Two holes at Red Hill have changed that.

The first, drilled in May, came back with 18.8 metres of massive sulphide. The second, MU2603, went better. 21.9 metres, and known mineralisation now runs past 155 metres of strike.

Each hole is adding weight to the idea that Red Hill is part of a much bigger mineralised system.

The detail catching attention is chalcocite showing up in the sulphides. Chalcocite is a high-grade copper mineral, and finding it can be a sign the drilling is closing in on the hotter core of the system.

Assays are still to come, so the visuals are only part of the picture, but the geology is pointing the right way and management has already stepped out with more holes to test where it strengthens.

Copper itself is climbing. Codelco, the biggest producer on earth, just posted a 27-year production low, and the metal is trading near the highest it's held all year. AZ9 is drilling a system that gets bigger with every hole, and the company’s well funded with more than $5 million in cash.

The next batch of assays aren’t far away now and they’ll be telling us a lot about how real Red Hill is.

Europe Wants Its Chips Back

One of the week’s bigger stories slipped past most people.

The European Union is lining up a major overhaul of its chip strategy, more than €120 billion aimed at building semiconductors on home soil instead of importing them.

Europe makes around 8 to 10% of the world’s chips today and wants to double that by 2030. Brussels is starting to talk about chip supply the way it talks about energy supply, as something a continent can’t afford to leave in someone else’s hands.

Money like that gets spent in two directions. Building the factories, and backing whatever makes the next chip faster than the last one.

That second part is where Adisyn (ASX: AI1) lives.

Through its graphene semiconductor technology, the company is chasing a path beyond traditional copper interconnects, aiming at better speed, lower power draw and improved thermal performance.

A modern chip moves data through a dense web of copper wiring. Shrink it far enough and copper starts to choke, running hot and slow at scales it was never meant to work at. The whole industry can see the wall coming.

Graphene is one of the materials being looked at to get past that limit, and it’s what AI1 is working on. Europe’s billions will build the fabs. The harder question, how to make the silicon inside them genuinely faster, runs straight through the work AI1 is doing.

As governments commit hundreds of billions to semiconductor independence, anything that can deliver the next step up in chip performance gets more valuable by the day, and the macro backdrop for AI1 keeps building.

A Coal Stock Rocketed. So Much for the Funeral.

Everyone's been writing coal's obituary for years. White Energy (ASX: WEC) put on 195% this week, the biggest gain of any company under $100 million, which suggests the funeral was called early.

The jump took its market cap to around $86 million, on a non-binding term sheet to pick up a metallurgical coal project in Alabama and a large package in Queensland's Surat Basin.

The spark was a sparky. Nathan Tinkler, the Hunter Valley electrician who rode coal all the way to becoming Australia's youngest billionaire before losing the lot, is coming back as executive chair.

The man instrumental in building Whitehaven, the $5 billion miner that swallowed his Aston Resources, is having another go.

Non-binding is the word doing the heavy lifting there. Due diligence, financing, approvals and definitive agreements all still have to land before any of it is real. White Energy said as much itself, flagging there’s no guarantee the deals complete.

The Alabama asset comes with a coal handling plant already built, rail access, and a staged restart aiming at production inside 12 months of switching back on.

Infrastructure that already exists is infrastructure nobody has to fund from scratch.

So a market that supposedly hates coal just bid a coal stock up 195% on the strength of a deal that hasn’t closed yet. For all the noise around AI, defence and critical minerals, a credible path to revenue still gets coal a serious look.

The Big Money is Still Backing Lithium

The most telling signal in lithium this week came from the companies writing the cheques.

Western Australia approved the Mt Holland expansion, doubling spodumene concentrate capacity to 4.4Mtpa, while MinRes and Ganfeng signed off on a fresh $490 million investment into Mt Marion.

Spot lithium is still well off its all time highs, but it’s still very healthy and the biggest players in the game are committing serious money to future supply anyway.

Big investments like these rarely hinge on where the price sits today. They’re built on where management teams reckon demand lands a few years out.

Down at the junior end, Solis Minerals (ASX: SLM) put on 41.2% after locking in a A$6 million placement and pushing ahead with plans to drill in Brazil.

Funding often shows up before the discovery does. Capital’s still there for the stories investors believe can deliver.

Why a Quiet June Might Suit Us

There’s a thing that happens to markets in June, and most people read it backwards.

The volume disappears. Tax-loss selling drags it off, the screens go thin, and the easy assumption is that nothing’s happening and nothing’s about to.

The opposite is usually closer to the truth. A thin market is one with nothing standing in the way of a good result, which is exactly why a strong announcement hits harder in June than it would in a crowded tape.

Commodity prices are holding up, and the money is still walking past the companies that just talk to back the ones that deliver, drill results, resource growth, actual revenue where it exists.

The portfolio’s got drilling results, assays, development milestones and a few commercial calls all due over the coming weeks. Plenty of our holdings are kicking hard into the back half of the year.

The stocks that run in 2026 are the ones putting out real results, one announcement at a time. Finding those companies before the rest of the market does is the whole job, and it’s the one we get up for.

Till next week.