Weekly Wrap: Drones Usurp Warships, Chips Top $1t and Fortuna Clears the Field

Britain's scrapping warships it's sailed for a century. You can guess what for.

Well, that’s us out. The Socceroos went down on penalties, and our two-week stint as armchair tacticians goes down with them.

Back to the day job, which had a better week than the national side.

An explorer put its ore through a plant, and the concentrate came out cleaner than some of the world’s biggest producers. High grade copper results land in Mongolia. A gold explorer puts a diamond rig into a historic million ounce gold mine.

We saw big investments in drones and chips this week, a small-cap expands its contract with a major, and a biotech that’s one to watch.

Here’s what caught our eye this week:

The world’s cleanest rutile from a bulk sample lands for Fortuna

Evion lands in Nevada fluorspar and turns a graphite profit

Drilling gets to untested depths for Black Horse

Gold’s worst quarter since 2013, central banks keep buying

Sulphides hit in NSW for Exultant Mining

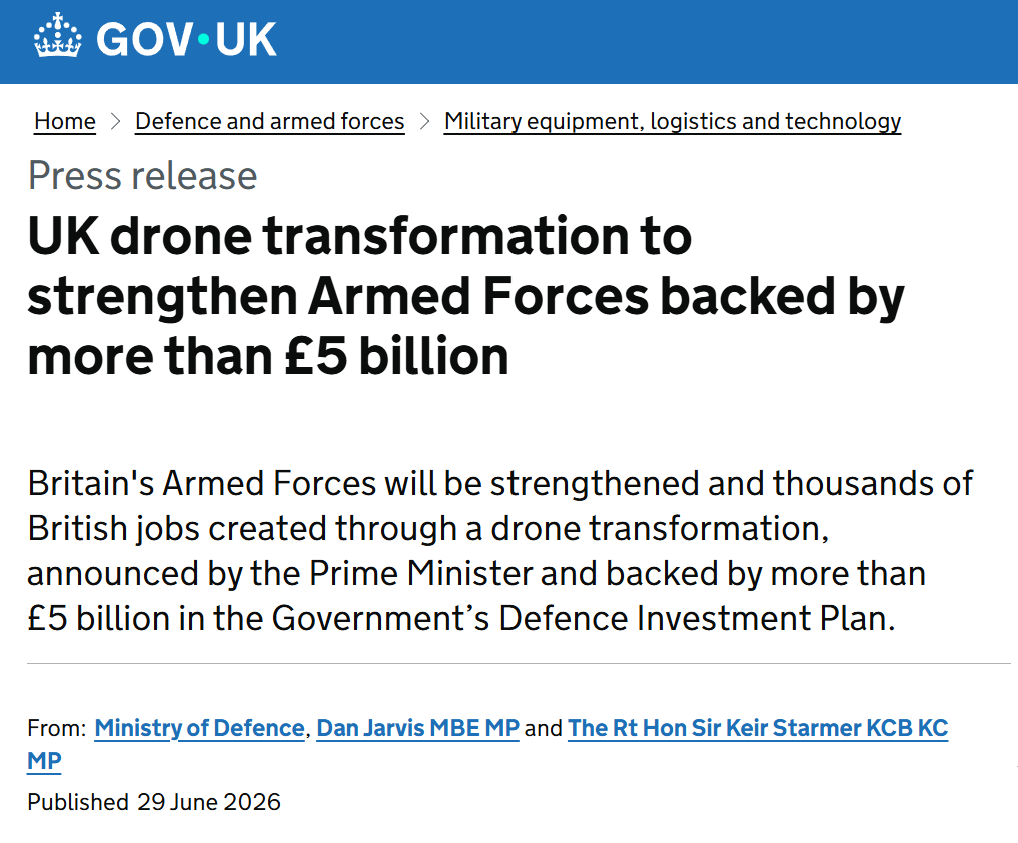

Britain puts £5 billion into drones, ditches its next destroyers

Chip spending blows past a trillion dollars

Swift TV keeps winning repeat Chevron orders

Syntara, a biotech in the right space waiting on big results

But First, We've Been Picking Brokers' Brains

We’ve hit the phones, sent emails and had coffees with brokers all around Australia the past couple of weeks.

The ask was simple: tell us what you think will do well in the second half of 2026.

We've pulled it all together: the sectors they like, and the small-caps they're backing.

We'll have it all in an article this week, subscribe now to be first to know.

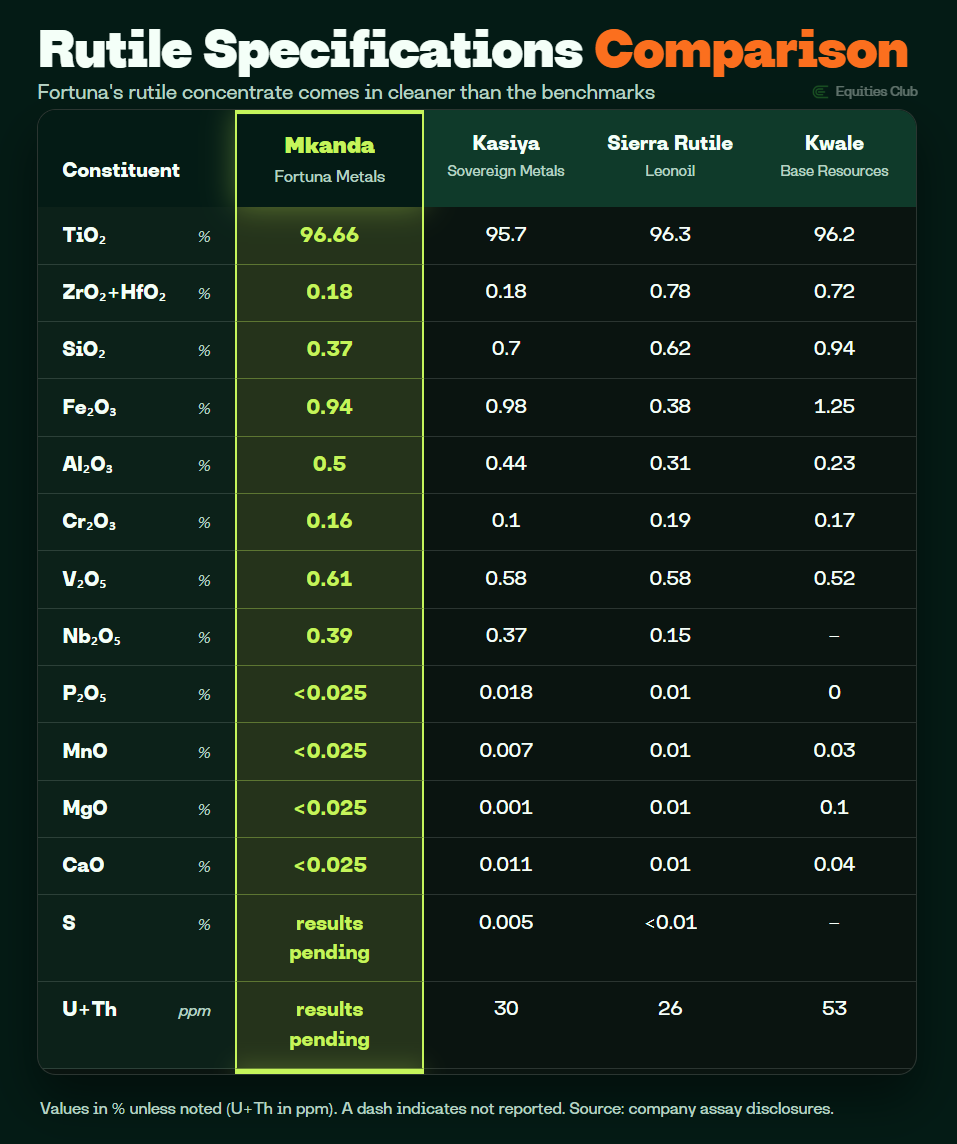

FUN’s Rutile Comes in Cleaner Than the Producers

Fortuna Metals (ASX: FUN) ran its first bulk sample through a plant this week, and pulled out rutile grading 96.66% titanium dioxide.

That's cleaner than the rutile the established producers have been shipping for years. The stock finished the week up 11%.

Rutile is the cleanest natural source of titanium, which is pretty much the whole pitch. Every bit of waste left in it is something a buyer has to refine out down the line, so the cleaner it comes, the more they pay.

At that grade, Fortuna’s out in front.

Sierra Rutile has been loading ships out of Sierra Leone at 96.3%. Base's Kwale mine in Kenya came in at 96.2% before it wound down. Both fed the world's pigment plants and titanium mills for years. Sovereign's Kasiya pilot, off the giant deposit up the road, came in at 95.7%.

Fortuna cleared the lot on its first pass.

Hand-pick the best pieces off a site and you can flatter almost any deposit, which is why nobody gets too excited by a headline number from rock chips.

Fortuna crushed 5.4 tonnes of ground and ran the lot through the plant, waste and all, and 96.66% is the grade that came out.

The concentrate is headed for titanium sponge makers, the high-value end of the chain that feeds aerospace-grade metal.

A maiden resource lands within weeks, the first number on how much of it is actually down there.

Check out the full write-up on the result here.

Evion’s Big Week: Nevada Boots and a Downstream Push

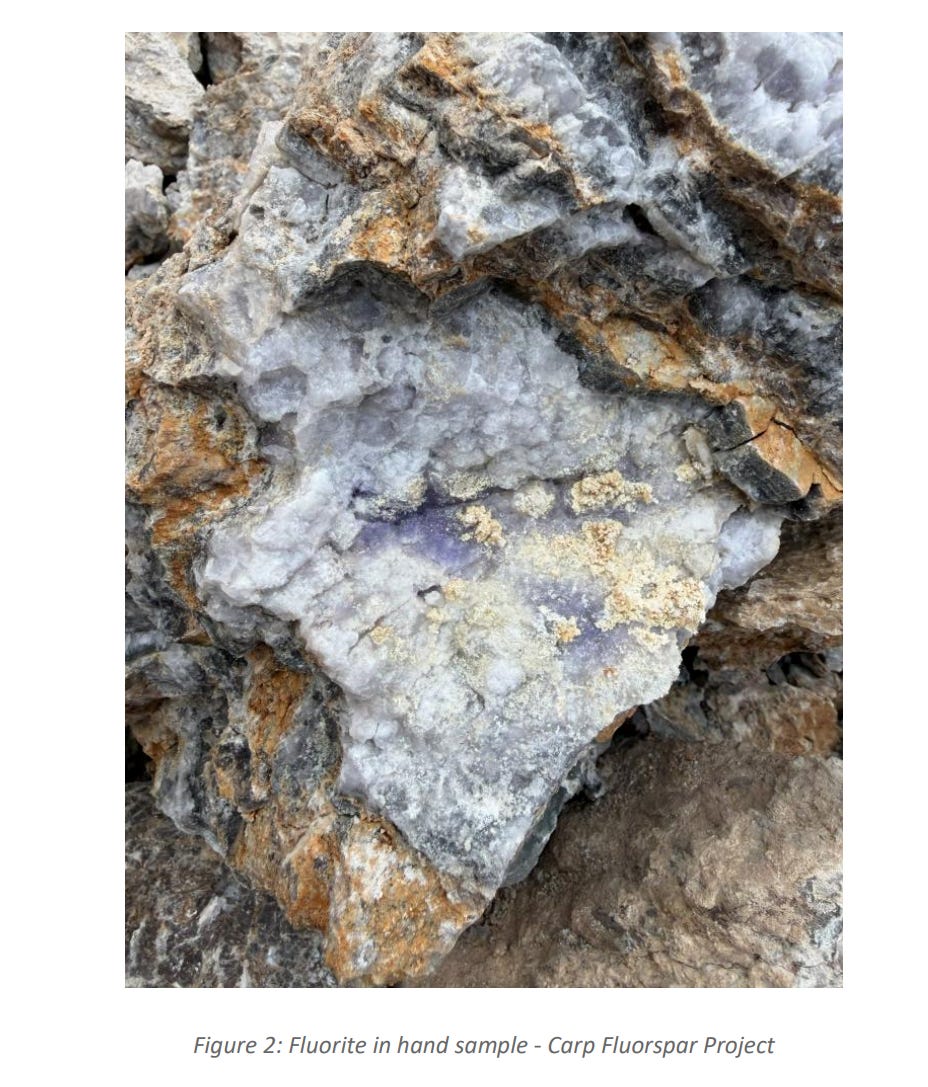

The world’s biggest economy can’t supply its own fluorspar. This week a tiny ASX company went after that problem out in the Nevada desert.

Evion Group (ASX: EVG) had a second story running in India too, and the stock finished up just over 13%.

Monday put boots on the ground at Carp, the historic fluorspar mine in Nevada that EVG optioned in May.

A field crew is sampling a north-west corridor beside the old pits, with a magnetic survey to follow and drilling once the targets firm up.

Carp shipped fluorspar to Kaiser Steel for 13 years at around 69% purity before cheap imports shut it in 1971. Verified sampling has since pulled grades as high as 88.15% CaF2 out of the same pits.

At 69% it goes to steelmakers as a flux, the cheap end of the market. As the number climbs it heads toward acid-grade, the premium tier that feeds batteries, chips, refrigerants and nuclear fuel.

America imports every tonne of fluorspar it burns through, and the Pentagon recently put US$168.9 million into a single fluorspar supply contract. A high-grade deposit on home soil is just what Washington has started writing cheques for.

You can find our write-up here.

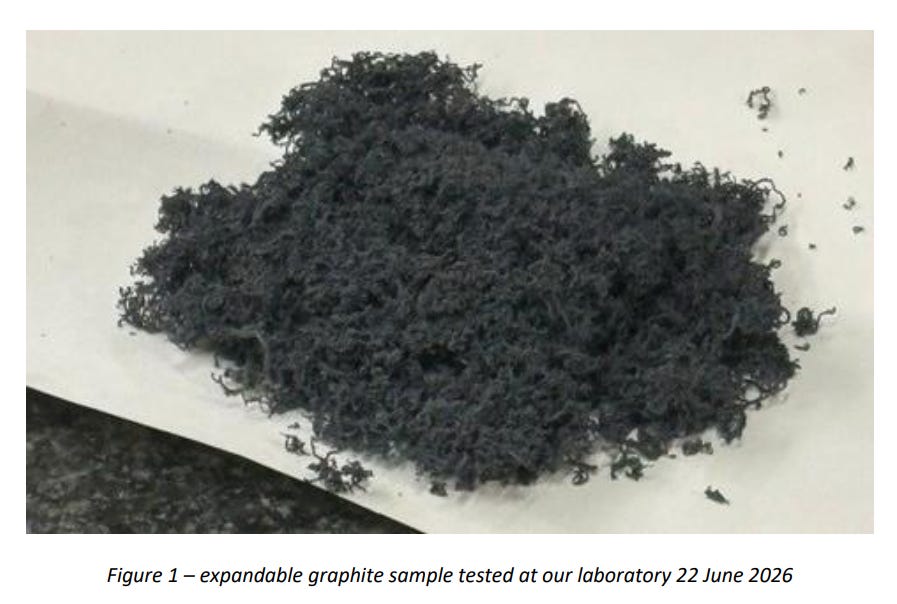

Evion’s Indian graphite arm, Panthera Graphite Technologies, is already turning a profit, and Thursday’s announcement set out how it plans to scale.

Positive EBITDA in FY2026 gives it the base to push expandable graphite into AI data centres, defence and battery safety, the markets where fire protection and thermal management earn premium prices.

A profitable graphite business in India and a high-grade fluorspar project in Nevada give Evion two levers into the same story: the West scrambling for critical minerals it can source outside China.

AZ9 Hits Thick, High-Grade Copper in Mongolia

Azzuro Resources (ASX: AZ9) drilled the best hole in its life at Red Hill this week.

A survey had lit up copper sitting at depth under Red Hill in Mongolia. Azzuro drilled straight at it and pulled up more than 21 metres of copper-rich sulphide grading 1.70% copper.

Plenty of copper explorers report grades under 1% and call it a good day.

Tucked inside that run was an 8-metre core going 3.27% copper, near enough double the headline again.

The hole carries gold, silver and a bit of zinc alongside the copper. In a producing mine those get sold too, and rolling them into copper terms lifts the grade to 2.84% copper-equivalent.

The copper also sits closer to the surface than Azzuro expected, and the shallower ground carries the better grade. Shallow copper is cheap to mine, so higher grade up top is about the best result they could ask for.

Assays on nine more holes are due this month, and the rest of the 2026 program is funded, so the rig keeps turning without a cap in hand.

Copper is near record highs, with data centres, grids and EVs all pulling on the same tonnes while a new mine still takes the better part of two decades to build.

Azzuro is worth about $15 million. It just drilled a copper hole a company 20 times its size would be happy to put its name on. Nine more holes are at the lab.

Our full write up can be found here.

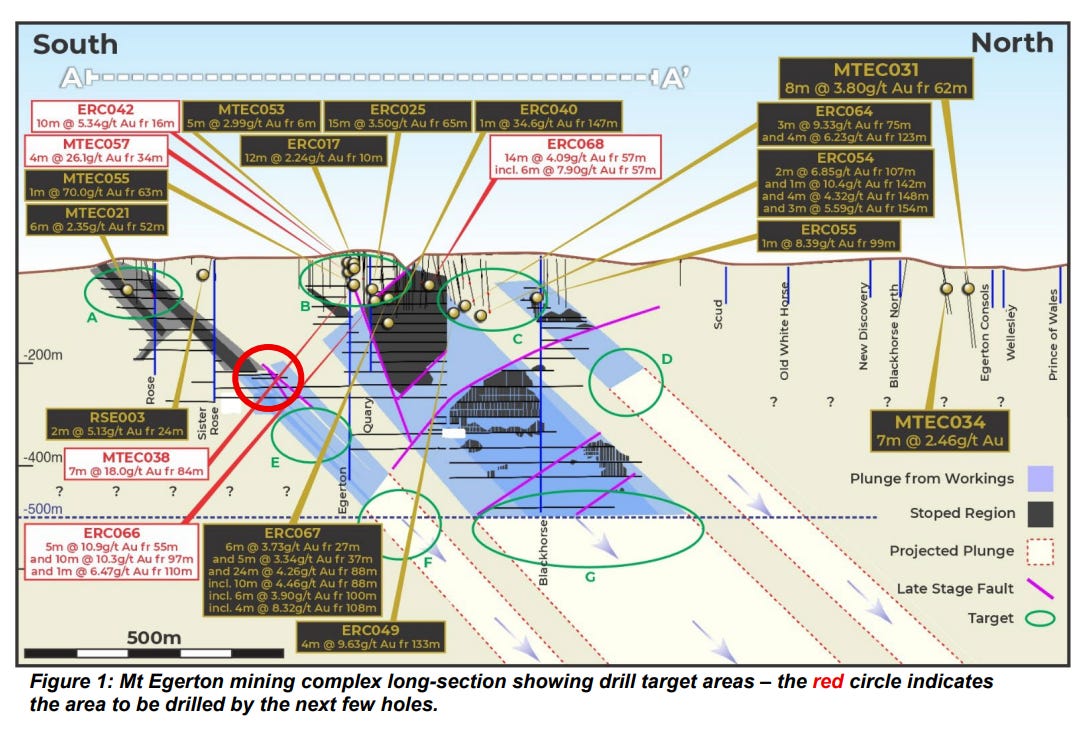

BHL Goes Deep at Mt Egerton

In 1906 the water won.

Mt Egerton had produced 1.29 million ounces of gold at around 12 grams a tonne when the workings flooded. The pumps couldn’t hold it back, so the miners walked out and left the gold sitting under the water line.

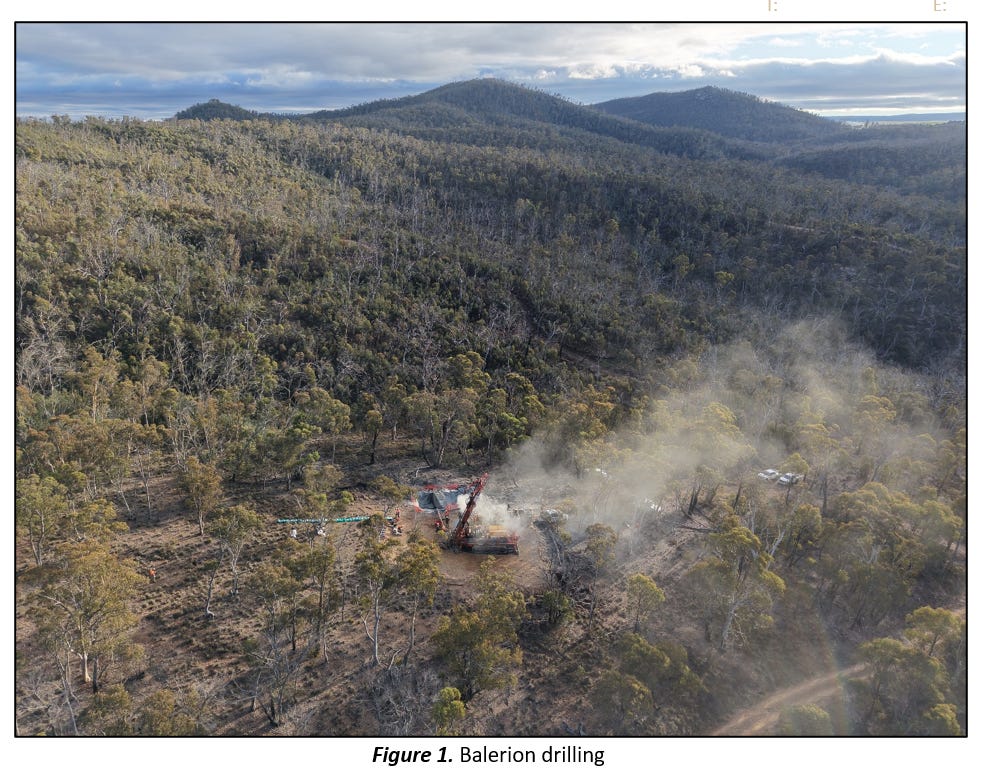

This week, 120 years on, Black Horse Mining (ASX: BHL) put a diamond rig on the ground to go and get it.

The rig is on site, with the deeper holes, around 500 metres each, due to start turning within 10 days.

More than 90% of the drilling at Mt Egerton has stopped above 150 metres, so the deep ground has barely been touched. These are the first holes going after the gold down where the pumps gave up.

Victorian goldfields tend to get richer the deeper you chase them. Fosterville was a tired little mine nobody rated until someone drilled beneath the old workings and hit the Swan zone, which turned it into one of the richest gold mines on earth. Mt Egerton sits in the same corridor, and no one has properly drilled it deep.

Black Horse is also reopening the Sister Rose adit, a tunnel sealed for more than a century. Getting back inside lets them map where the old workings run, so they can aim the drill at the right ground.

The early holes came back with only anomalous gold, so keep the expectations in check. This is a deep test of ground no one has drilled, which is where the risk and the reward both sit.

BHL is our 2025 Small-Cap of the Year. It trades at 19 cents, under its 20 cent listing price, with the drills now heading for ground the old timers never reached.

For anyone wanting exposure to a Victorian gold play with a million-ounce history, that entry point does some of the work for you.

Gold’s Pullback has Big Buyers Stacking

Gold just had its worst quarter since 2013, down 15% to around US$4,175 an ounce. In January it was scraping US$5,600.

Step back though and it's still up about 23% on a year ago, which tells you how hard it ran before this.

The tourists are heading for the exits, spooked by a Middle East war that has markets betting on higher-for-longer rates, which pulls money out of bullion.

We read the drop as a correction inside a bull market, one that shakes out the punters who piled in near the top and resets the base for the next leg.

Not long ago the queues ran around the block outside ABC Bullion in Sydney, people happy to wait hours for a bar. Money like that comes and goes with the headlines.

The people who run central bank reserves move slower. A survey of them landed this week from OMFIF, a London think tank that tracks how they invest, and most see gold between US$5,000 and US$6,000 over the coming year.

The World Gold Council found a record 45% of them plan to add to their holdings over the next 12 months.

They buy on a ten-year view, and they're still buying now.

We covered the investment bank targets last week, most sitting well above where gold trades today. Put those next to a pullback that's already done most of its damage, and it's a backdrop we're comfortable holding through.

The crowd that queued for bars not long ago is now halfway out the door. The buyers who move this market count in tonnes and decades, and a record share of them are lining up to buy more.

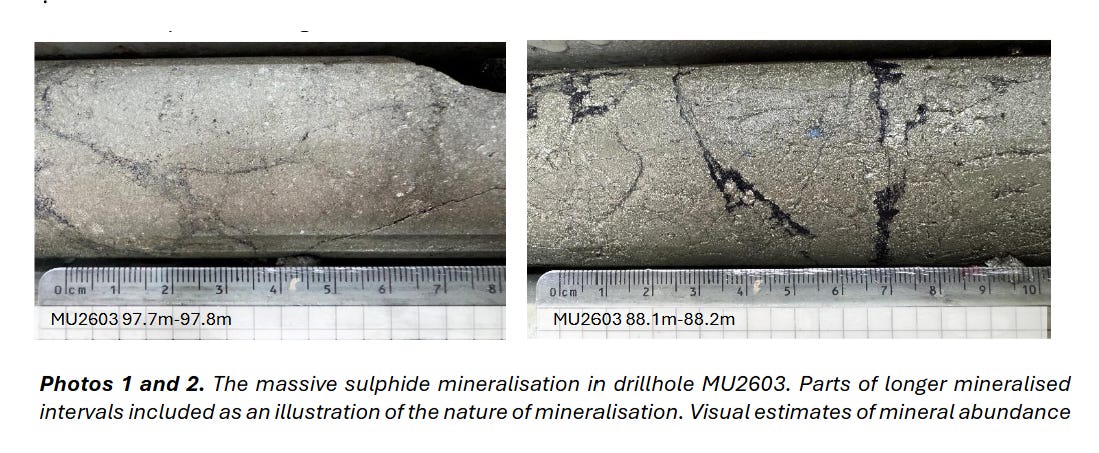

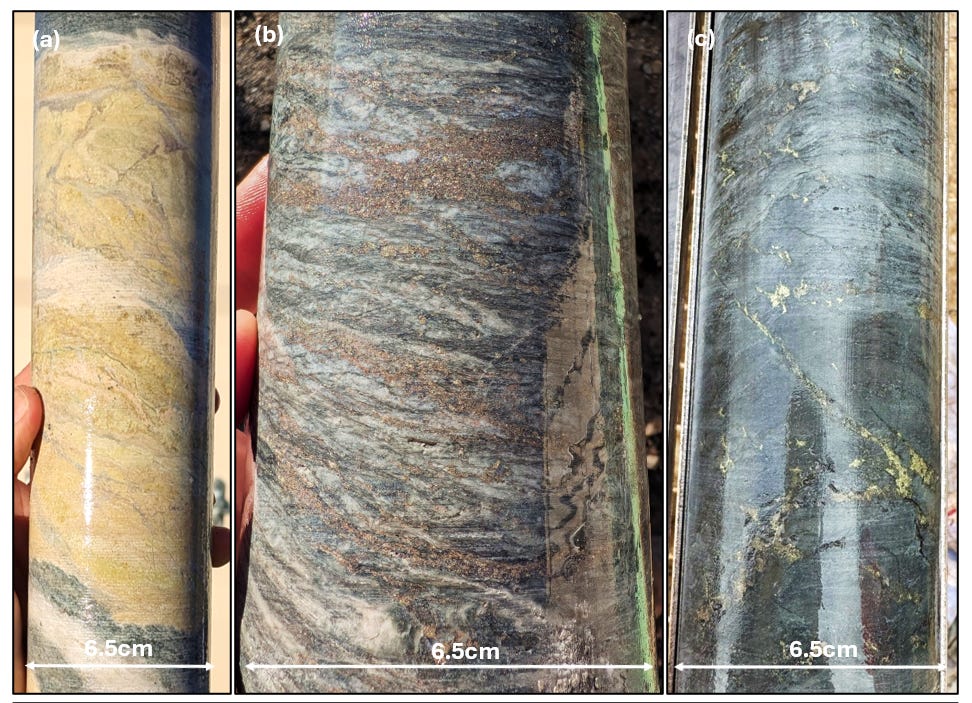

Sulphide in Two of Three for 10X

The first holes are in the ground at Exultant Mining (ASX: 10X), and the early signs are promising.

Two of the three came up carrying the copper, zinc and lead 10X was chasing at its Balerion prospect, part of the Peak View project in southern NSW.

The second hole was the pick, a thicker, more continuous run of sulphide than the first, with a coarse banded zone the geologists were happy to see.

These are visual reads off the core, not lab numbers, so how rich it is comes down to assays, still pending on all three holes.

The team were able to tidy up the targeting and trimmed the program with five holes remaining. Those five are the ones that count, aimed down-dip of old high-grade hits into ground no modern rig has reached.

10X is one of ours, trading at 18.5 cents for around a $7 million market cap.

You can find our full write up here.

Drone Spending Keeps Climbing

Ukraine is now burning through around 9,000 drones a day.

That number is rewriting how rich countries think about hardware, and this week Britain put a price on it. Its long-delayed Defence Investment Plan landed with drones taking £5 billion over four years, the most the country has ever committed to them.

To pay for it, the Royal Navy is walking away from its next line of destroyers. They're giving up warships they've sailed for a century, all for machines that cost a few thousand quid and often don't make it home.

The safest way to play a boom like this is to build the part every drone needs, whoever’s name ends up on the side. That’s the well-worn picks and shovels mantra, while everyone else pans for gold.

It’s what KTEK Aerosystems (ASX: KTK) does, making the airframes and sub-assemblies that go inside drones for the tier-one defence contractors.

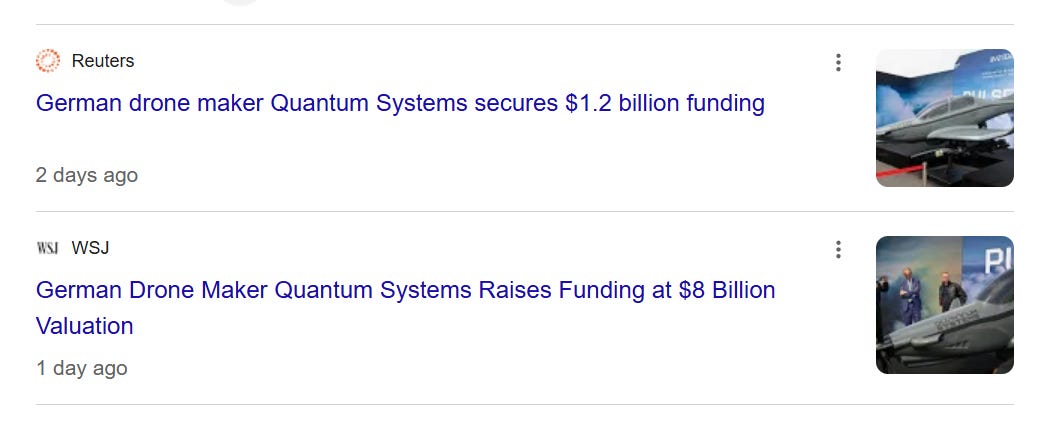

Private money is moving just as fast as the governments. German drone maker Quantum Systems raised US$1.2 billion this week, with Blackstone and Airbus writing cheques, doubling its valuation to US$8 billion in a single round.

KTK locked in a Los Angeles facility last month, putting its production inside the world's largest defence market, and its order pipeline into tier-one contractors has filled out since.

When the whole world is buying drones, you want to be the one selling the parts.

Chips Blow Through the Trillion-Dollar Mark

The world is spending an absolute fortune building computer chips right now.

South Korea just committed more than US$576 billion to it, with Samsung and SK Hynix each building two new chip factories. Taiwan’s TSMC, the company that makes the chips inside your iPhone and Nvidia’s AI hardware, is putting US$165 billion into Arizona alone, the biggest foreign investment America has ever seen.

Every dollar of it traces back to AI. Chip sales pass US$1 trillion this year for the first time, and some believe they’re headed toward US$1.5 trillion as the AI race eats every chip it can get.

(We paid $900 for a 4TB hard drive at JB this week. You can thank the AI build-out for that too.)

But there’s a problem sitting inside every one of those chips, and no amount of money makes it go away.

A chip works by moving electrical signals through unbelievably tiny wiring, and that wiring is copper. As chips keep shrinking, the copper has been squeezed about as thin as copper can physically go. Push much further and it stops doing its job.

So the industry needs something to replace the copper, and it agrees on what that something is: graphene. That’s where Adisyn (ASX: AI1) comes in.

Last month it grew graphene at under 300°C, cool enough that a finished chip survives the process, verified by the University of New South Wales. And it holds the patented chemistry to grow that graphene inside the machines chipmakers already use.

A trillion dollars a year of chips is about to run into the limits of copper. Adisyn is one small ASX company holding a patented way around it.

Deals Are Landing For This Small-Cap

If you’re stuck on a mining camp hours from anywhere, or out on an oil rig off the coast, you can’t just flick on Kayo and watch the footy. The internet out there won’t carry it.

Swift TV (ASX: STV) has built a whole business on fixing that. Its low-bandwidth tech and on-site servers get Netflix, Kayo and the rest streaming in the places normal broadband can’t reach, from mining villages and offshore rigs to aged care homes.

And once a screen goes in, it keeps paying. Swift runs it as a subscription, so the TV on the wall of a Chevron camp earns month after month.

The customer list runs to Chevron, Shell and Australia’s largest private aged care provider, and the board has some pedigree, with Argonaut co-founder Charles Fear as chairman.

Chevron came back for more this week, ordering another 1,900 devices to roll the platform out across its Barrow Island and Wheatstone Offshore accommodation sites.

The order follows more than 2,000 devices already installed at Wheatstone’s onshore village, lifting the installed base across Chevron sites to around 3,900. Last month the same relationship delivered a five-year subscription contract worth a minimum of $2.9 million.

A $9 million company keeps landing repeat orders from one of the biggest energy companies on the planet, and barely anyone has noticed.

Big Pharma Keeps Paying Up to Fix One Blood Cancer

Myelofibrosis is a rare cancer of the bone marrow, and it’s become one of the most fought-over targets in the drug world. Over time the marrow turns to scar tissue and the body stops making blood properly, leaving patients exhausted with swollen spleens.

The drug most patients get put on is ruxolitinib, and it works for a while. The trouble is that somewhere between half and three-quarters stop responding within a few years, and when they do they’re nearly out of road.

This week Ipsen, a French drug company, agreed to pay up to US$1.75bn for a private US biotech called Kartos. They’re buying it for a single drug, navtemadlin, designed for the patients ruxolitinib has stopped helping. GSK recently paid up in the same space too, buying into its own myelofibrosis drug.

Syntara (ASX: SNT) is a small Sydney biotech worth less than $50 million. Its lead drug, amsulostat, targets those same patients, the ones who’ve stopped responding to standard treatment.

It takes a different approach to the drugs Ipsen and GSK bought, but it’s chasing the same problem. The US FDA has cleared the design of its next big trial starting in the December quarter.

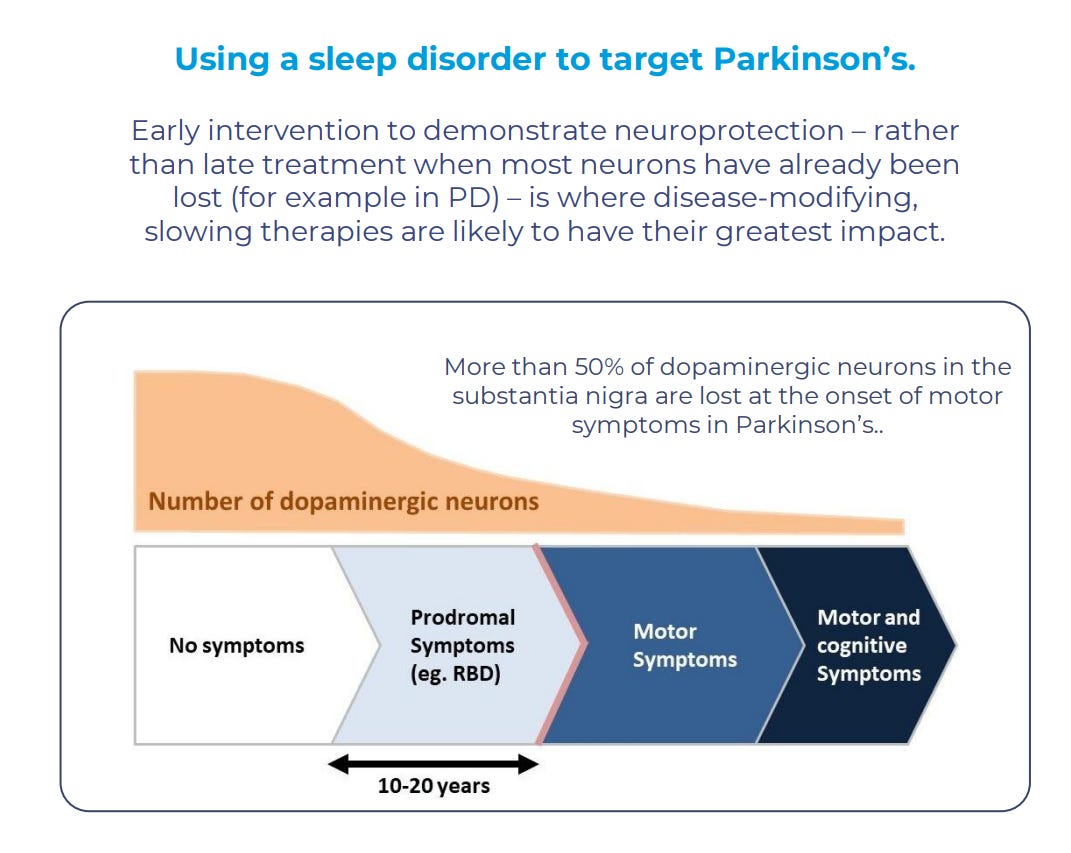

Syntara shares ran 21% this week before the company called a trading halt on Friday. The halt covers a different Syntara drug entirely, SNT-4728, which is being tested in a sleep disorder that often shows up years before Parkinson’s.

Early results are due next week, with trading set to resume by Tuesday unless the news lands first. We don't own Syntara and it's not a client. Clinical-stage biotech lives and dies on results like these, so expect a big move either way.

The Week Ahead

A new financial year is here and it feels like optimism is starting to creep back into the market. Many brokers are still away, but if you’ve been around the small-cap game long enough, you know a lot of positioning happens now.

We’ll have our piece out on the broker picks for the back half of 2026. Some familiar small-caps named, and some completely left field.

Gold looks to be bouncing and the forecasts into the new year are strong. Defence and tech money keeps flowing. And we’ll be watching the biotech space closely, with trial results due.

Till next week.