Weekly Wrap: JPM in the Tabloids, $55B for Drones and Three-in-One at FUN

Wall Street provided the entertainment, the Pentagon multiplied a drone budget by 240, and Fortuna stacked rare earths and graphite on top of its rutile

JP Morgan had a bad week. The kind of bad week that ends careers and starts lawsuits and fills tabloids around the world.

The bank spent it answering for things that had nothing to do with the price of money or stocks, and by Friday the whole thing was coming apart at the seams.

We won’t dive into it but if you haven’t caught up on the story, wait until the kids leave the room.

Wall Street, as ever, providing the entertainment.

Closer to home, things were quieter. The ASX 200 finished the week roughly flat after another hotter-than-expected inflation number was shrugged off, and commodity prices held their ground while blue chips drifted through five sessions of indifference.

Quarterly reporting season also landed this week, which is the part of the calendar a lot of retail investors underrate.

For a pre-revenue explorer or biotech, the quarterly is the only window you get into how the company is actually being run. What got drilled, what got spent, and most importantly, what’s left in the bank.

It's the cleanest read you'll get on whether the company you're holding is three months from a rerate or three weeks from coming back to market with the hat out.

Here’s what caught our eye:

We’re giving away an ounce of gold, for FREE

Fortuna Metals folds rare earths and graphite into the rutile story

Mount Ridley Mines brings on a metallurgist with the right CV

The Pentagon goes from US$225m to US$55bn on drones

Solstice Minerals nearly doubles on Nanadie depth

Pathkey runs 50% on a Singapore semiconductor deal

Intel posts its biggest month in half a century

One Ounce of Gold, Yours to Win, for FREE

One ounce of gold. Real, physical, from the Perth Mint. It goes to whoever calls the gold price in AUD closest at 12pm AWST on 1 December 2026.

Entry is free.

Gold’s been on a tear most of us never thought we’d live to see. The Iran war broke the bull run for about a fortnight, then the price went back to climbing. Central banks kept buying through the dip.

Meanwhile, the world’s debt pile crossed US$346 trillion last quarter, or roughly three times global GDP. Governments are now borrowing close to US$29 trillion a year just to keep the lights on. All of this adds chapters to the gold bull narrative.

Whether the next leg is another rip higher or a long sideways stretch is your call.

Closest to the pin takes home the ounce.

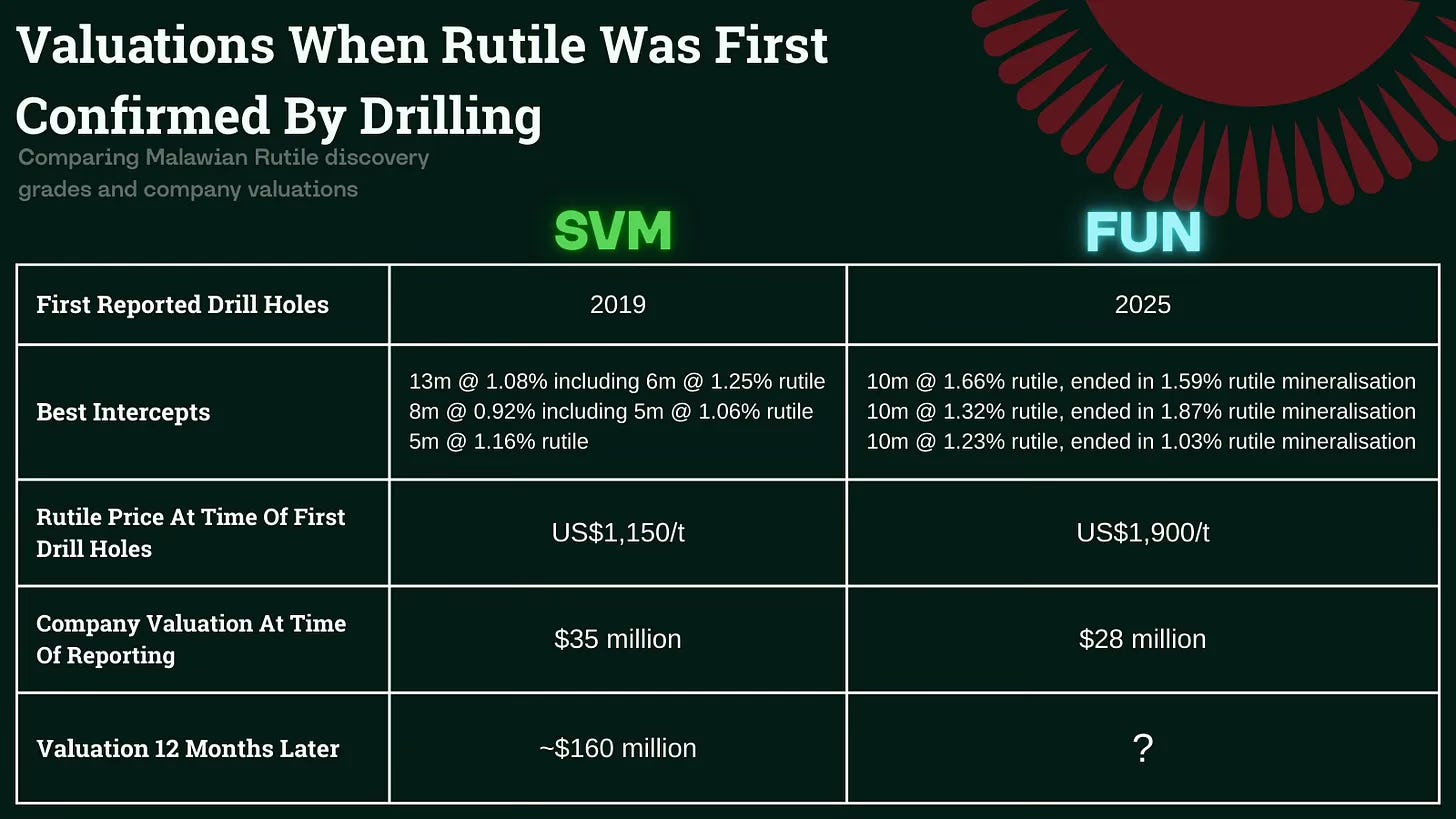

From Rutile Play to Three-Commodity Story

Fortuna Metals (ASX: FUN) had a hell of a week. Two announcements in three days and the share price up around 25% by Friday.

For new readers, FUN is a small-cap rutile explorer working in Malawi. Their project, Mkanda, sits 20 kilometres south of Kasiya, the largest rutile deposit on the planet. Kasiya is owned by Sovereign Metals (ASX: SVM), capped at roughly $460 million with Rio Tinto on the register.

FUN is working the same belt of rocks with the same weathered geology, but much earlier in the story.

Fortuna’s first announcement this week expanded the mapped rutile footprint at Mkanda from 37 km² to 53 km², with the high-grade core now sitting around 28 km².

That sits on top of a 180-240 million tonne maiden exploration target FUN put out three weeks ago, and that target was calculated on samples only four metres deep.

And there’s a lot more rock under that.

Then on Wednesday came the announcement we weren't expecting. Drilling at Mkanda picked up heavy rare earth grades and graphite intercepts in the same dirt, and the chemistry came back ahead of Kasiya on two of the three magnet metals that matter. Yttrium grades ran nearly double Sovereign's.

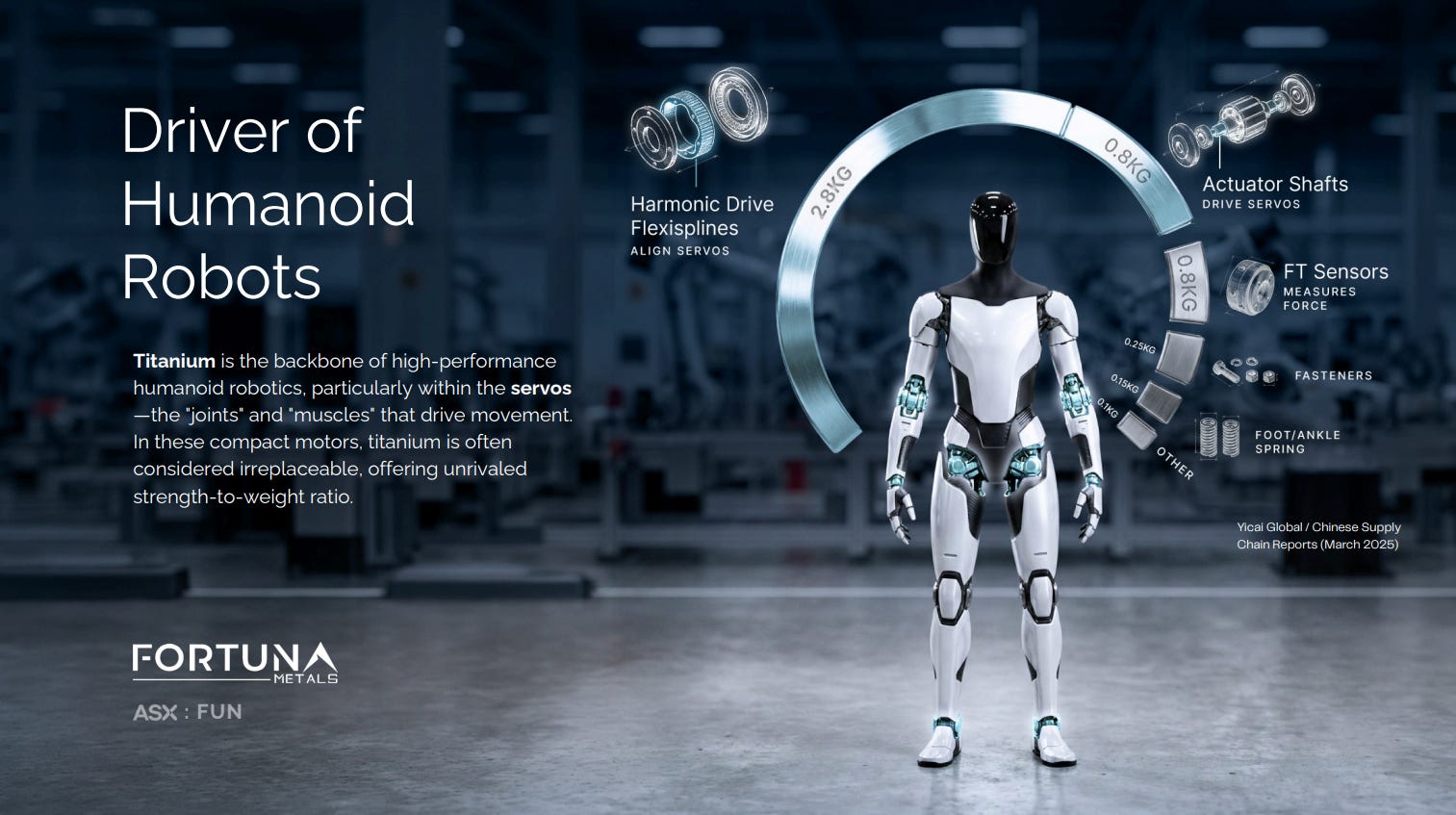

Rutile is the cleanest feedstock for titanium. Titanium goes into jet engines, missile casings and humanoid robots, and each humanoid uses up to 10 kilograms of rutile.

There's currently one humanoid being built every thirty minutes in China, and that pace of growth is only going up.

Dysprosium, terbium and yttrium are the magnet metals that sit inside EV motors and defence-grade electronics. Graphite goes into every EV battery on the planet, plus a long list of industrial uses.

At a $28 million market cap, Fortuna is currently valued at less than a fifteenth of its northern neighbour, despite working through the same geology. Graphite hits at Mkanda are already running several times Kasiya's average grade.

Aircore rigs roll into Mkanda late next month to drill below the four-metre depth limit of the hand augers. The last time deeper drills went into this geology, Kasiya’s resource jumped from 644 million tonnes to 2.1 billion.

A $28 million company sitting on the same belt of rocks as a $460 million neighbour, drilling three commodities the world is short of, with deeper holes about to go in. Hard to think of a setup we'd rather own right now.

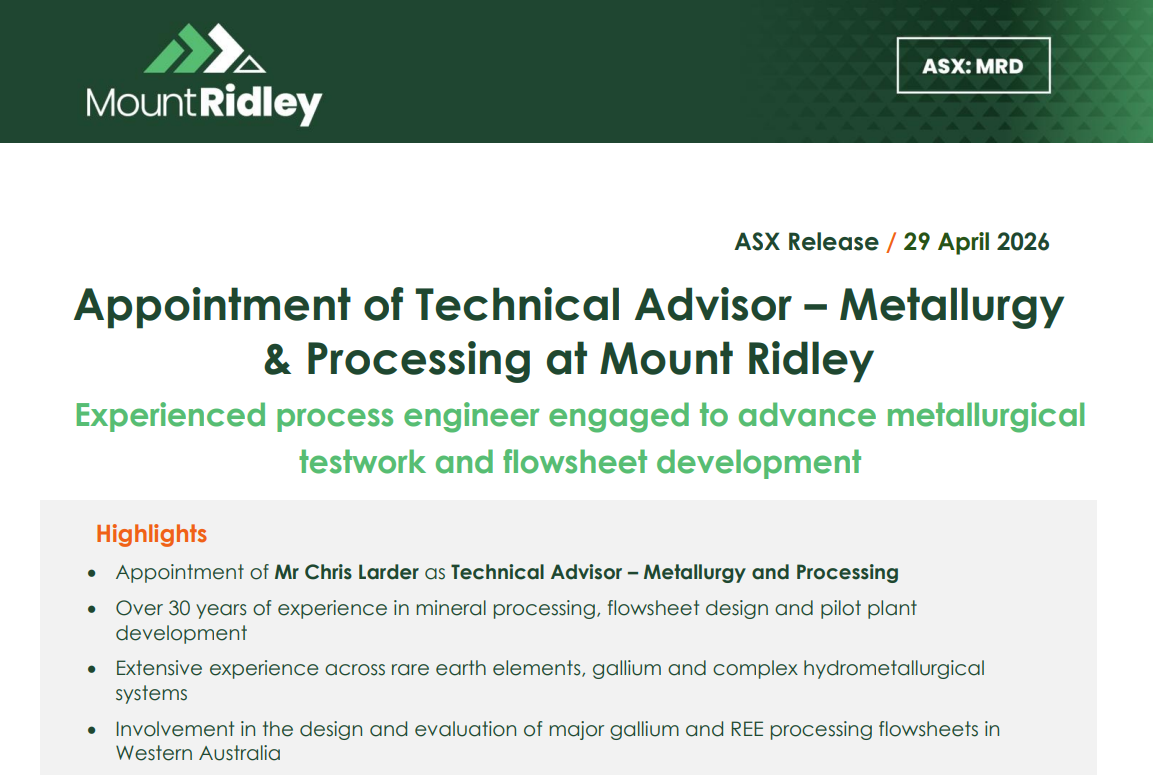

MRD Hires a Lynas Hand for Grass Patch

Mount Ridley Mines (ASX: MRD) appointed metallurgist Chris Larder as technical adviser this week. It’s not a flashy headline, but the kind of move that’s crucial once a project gets close to flowsheet work.

Flowsheet design is the engineering blueprint that turns rock into a saleable product. It’s where critical minerals projects live or die.

Larder’s done that work at Wagerup (the WA alumina refinery) and Mt Weld (Lynas’ rare earth operation). Both sit in the part of Australia’s processing chain that governments are now actively trying to expand outside of China.

That experience maps neatly onto Grass Patch, MRD’s project just north of Esperance, where dysprosium, terbium, scandium and gallium are all sitting in the same corridor.

MRD already has early met testwork in the bank on Grass Patch, so this hire is about taking those results into proper flowsheet territory.

Every one of those metals is on the West’s critical minerals list. Bringing in someone who’s actually built flowsheets for these elements before tightens the pathway from resource to product.

Pentagon’s US$54 Billion Drone Bet

Last year the Pentagon spent US$225 million on drones. Next year it’s spending US$54 billion.

That’s the same budget line, multiplied by roughly 240, in a single planning cycle.

And when the US writes gigantic cheques like that, allies have to follow. NATO, Israel, Australia and parts of Asia all build militaries that plug into US gear, so when the gear changes, their defence buying changes with it.

On a military radar screen, a quadcopter drone currently looks about the same size as an F-35 fighter jet. Once spotted, it gets shot down a few seconds later. You can build drones cheap and smart and in swarms all you want, but if the radar sees them, none of that helps.

Adisyn Ltd (ASX: AI1) is developing a graphene material with Tel Aviv University that coats a drone and shrinks its radar signature by up to 100 times.

That same quadcopter, with AI1’s coating on it, now reads on radar at about the size of a bird. The next target, and what they’re working on right now, is making it insect-scale.

We announced AI1 had been added to the portfolio last week when it was 6.8c. By last Friday it was at 20c, after a graphene chip breakthrough on the Monday and an exclusive worldwide licence on the drone material two days later.

Meitav, Israel’s largest investment house, cornerstoned the $14 million placement that followed. Regal Funds Management came in alongside them. The placement shares allocated this Wednesday.

This week AI1 pushed to a new all-time high, then settled back to 21c by Friday.

The Pentagon’s announcement landed straight into the middle of all of that.

Solstice Minerals Doubles on Nanadie Depth

We flagged Solstice Minerals (ASX: SOL) back in February when the stock was trading at 93c.

It closed this week at $1.66, a roughly 78% move while drilling kept confirming the size of the copper-gold system at Nanadie in WA’s Murchison.

The intercept that kicked the run off was 62m at 1.55% copper and 0.66g/t gold to end-of-hole, including 22m at 2.78% copper and 1.25g/t gold.

This week’s update pushed it further. Solstice completed its first diamond tail to 629.1 metres, confirming visible chalcopyrite (the copper sulphide ore mineral) across multiple zones and extending mineralisation at least 300m below previous drilling.

The existing resource sits at 40.4Mt at 0.4% copper and 0.1g/t gold. In a system like Nanadie, going deeper is how you find more copper, and Solstice just went 300 metres deeper than anyone has before.

A 10,000 metre Phase 2 RC program is already turning, with another 2,000 metres of diamond tails to follow.

Plenty of stories run hard and then sit. This one has reasons to keep moving.

Pathkey Runs 50% on Semiconductor Deal

Designing a custom chip from scratch is one of the hardest, most expensive things a tech company does, and there are not many people in the world who can do it.

The ones who can are paid like surgeons. A mid-level hardware engineer hits the job market and is gone within six hours. They get poached every six months by the same handful of companies who are themselves losing engineers to the same handful of competitors.

It’s the same group of well-paid people just swapping lanyards around basically.

This week, an ASX small-cap with a market cap of $30 million took a binding option on a company that automates what they do.

Pathkey.AI (ASX: PKY) finished the week up roughly 50% after announcing a binding option to acquire Singapore-based Chipforge, an AI platform that runs the chip design process end-to-end.

Engineers describe what they want the chip to do, the platform writes the hardware code and runs the verification tests, then takes the design through to a physical prototype.

Full custom chip manufacture is next on the roadmap.

The slowest and most expensive part of this whole process is verification, the work of checking that the design actually behaves the way it's meant to before the chips get manufactured.

Verification alone eats more than half the time and budget of a chip project. Chipforge does it in software.

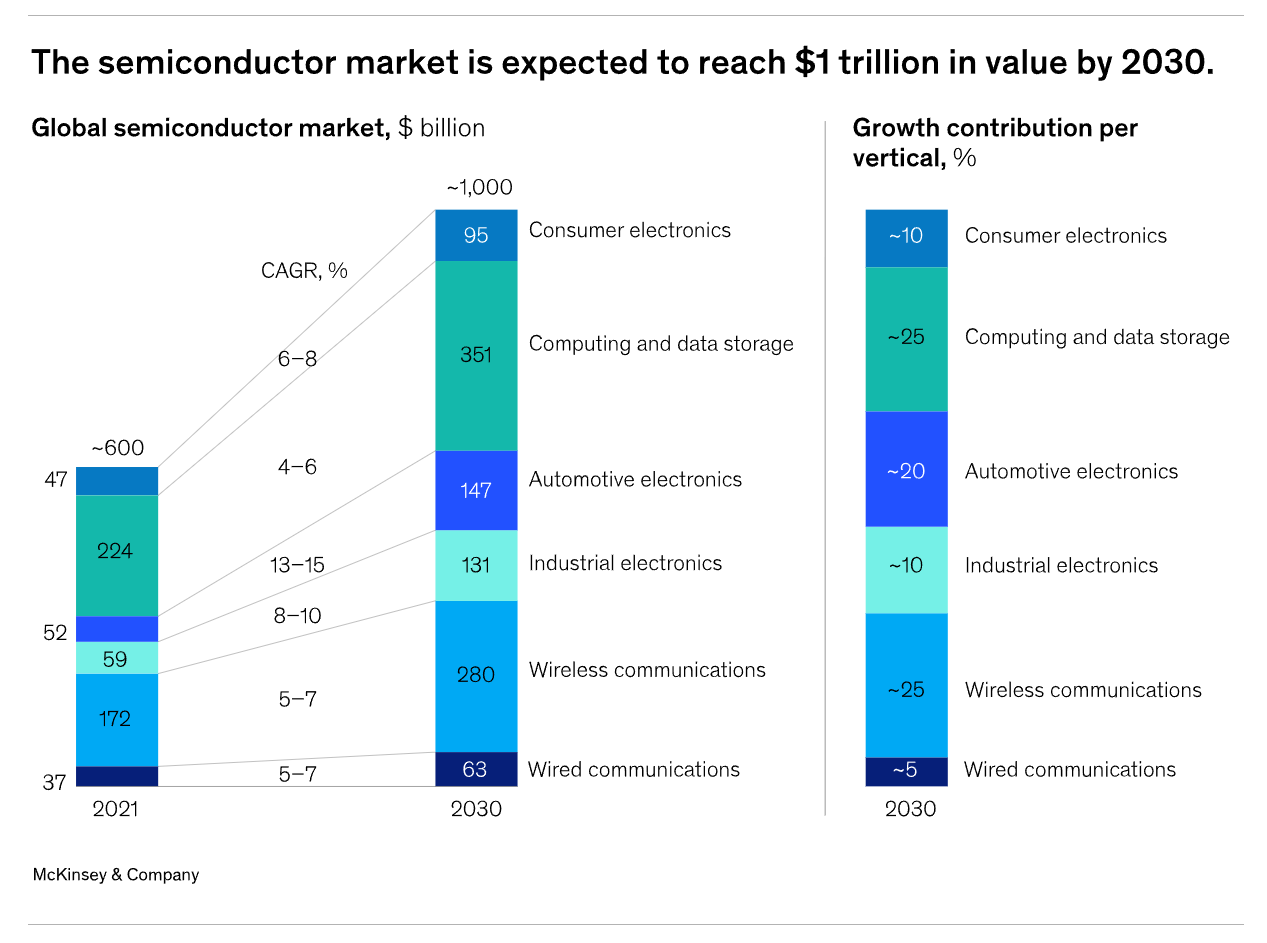

The deal lands Pathkey inside a sector that McKinsey predicts will hit US$1 trillion a year by 2030, driven by AI compute, data centres, defence electronics and edge computing.

It also fits with what Pathkey already does. Their existing TrialKey platform applies the same agent-based AI architecture to clinical trial design.

It’s the same engine, applied to two of the slowest, most expensive industries on the planet. One to keep a close eye on.

Intel’s Biggest Month in Half a Century

Intel had its strongest month on Nasdaq in 55 years, with the stock up around 114% in April after years of losing ground to TSMC and Nvidia.

Revenue lifted more than 7% in the latest quarter to US$13.6 billion, helped by hyperscaler demand from Google, Microsoft and Amazon, plus OEM orders from Dell, HP and Lenovo.

The Trump administration converted US semiconductor support into a near 10% stake in Intel this month. Washington now owns part of a chipmaker the same way it owns parts of the steel and oil industries.

Inside AI compute, the bottleneck is also moving. The processor isn't the only ceiling anymore. The interconnect layer between chips, where signal speed and heat loss start to cap performance, is the new pressure point.

Adisyn's graphene material has a second application here. The same coating being developed for drone stealth also works in chip interconnects, letting high-performance chips talk to each other faster and run cooler.

The Wrap

We’re hoping to hear that drilling has kicked off across a couple of portfolio names next week.

Exultant Mining (ASX: 10X) is lining up its maiden drilling campaign in NSW, and Asian Battery Metals (ASX: AZ9) is gearing up to go again in Mongolia chasing copper-gold. Both have the potential to move quickly if the drilling proves up good grades.

May is the last real window for capital raisings before financial year end, so expect a run of placements across the small-cap space over the next few weeks.

We’ll be watching the upcoming federal budget too, with a few interesting rumours doing the rounds about what might land in it.

On our end, we’ve been sitting down with a handful of companies lately. Can’t say much yet, but readers will be the first to know as things firm up.

Plenty more coming.

Till next week.