Weekly Wrap: Lithium's Revival, China's Grip Slips, Intel Rips

Thin volumes into year-end, but the themes carried it. Lithium's revival, the G7's move on China, and Intel's big run

The World Cup is underway, and the money around it has gone vertical.

Last time the US hosted, back in 1994, the average ticket cost about US$58. This year it’s nearer US$1,600, and seats for next month’s final in New Jersey are changing hands around US$16,000. A few have even been listed north of US$2 million.

Three host nations have poured money into stadiums and transport, betting the crowds pay it all back, and at those prices they probably will.

We’re writing this a little worse for wear. The Socceroos stunned Turkey on Sunday and the whole country was floating, then we got up before dawn to watch the Yanks bring us back to earth. Paraguay’s next on Friday, and we’ll be glued to that one too.

One result can turn a whole country, and markets are no different. A single number or headline and the price swings hard. We know that game well.

Back in small-cap land the news was a bit thin this week. A diamond rig finally turning below a million-ounce Victorian goldfield, a maiden rutile resource taking shape in Malawi, lithium roaring back to life, and the West drawing a line on Chinese rare earths.

Let’s get to it

BHL puts a diamond drill rig into a historic million-ounce Victorian gold mine

FUN commissions its own lab in Malawi as a maiden resource bears down

Lithium claws out of a two-year hole and runs hard

The G7 sets a deadline to break China’s grip on rare earths

IVG reckons it can make battery-grade graphite without the acid, and pops 28%

Billions pour into chips as Apple, Intel and Qualcomm redraw the map

It’s Diamond Drill Time in Victoria

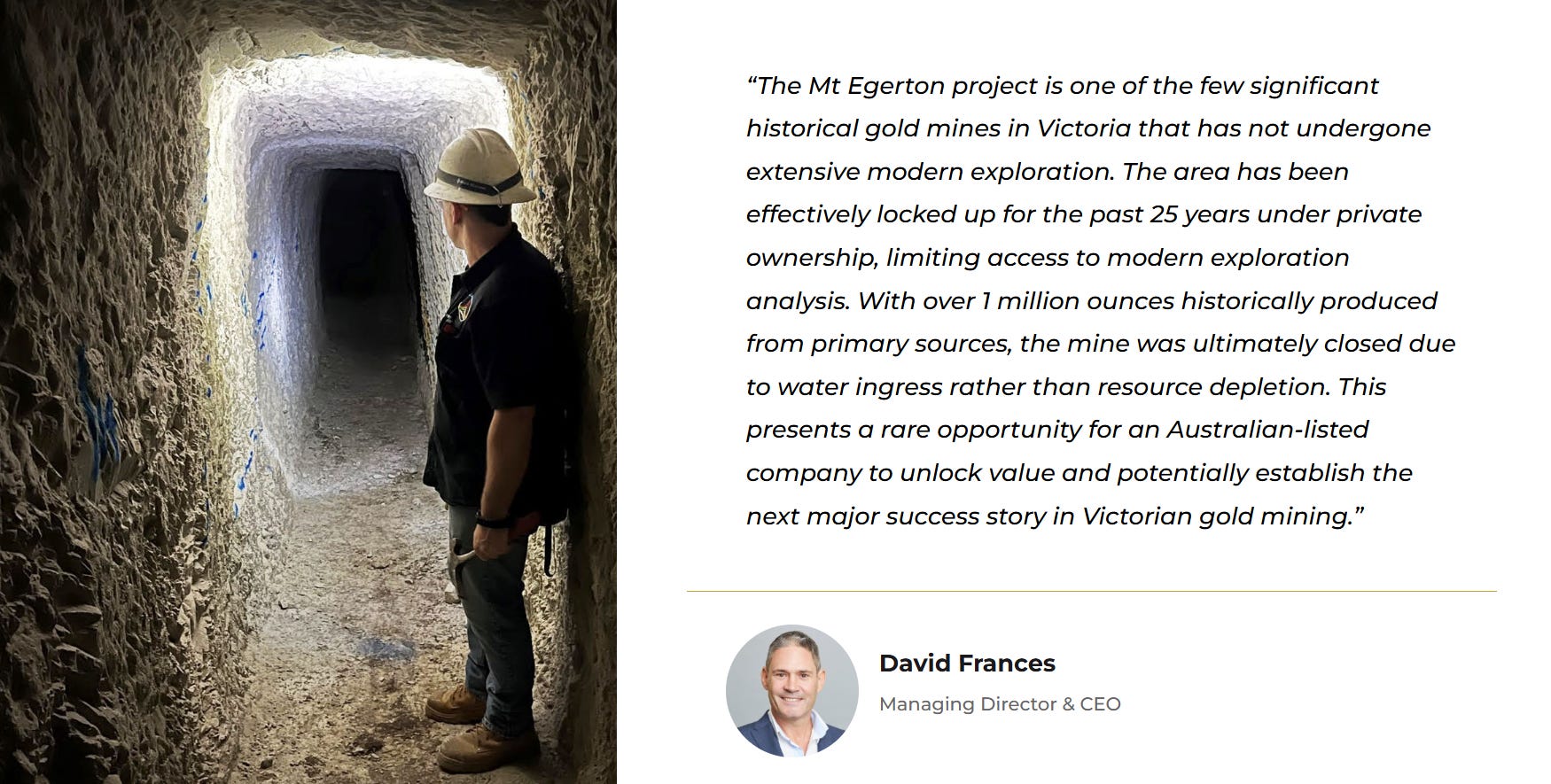

Our 2025 Small-Cap of the Year and portfolio company Black Horse Mining (ASX: BHL) finally has a diamond drill rig on site, ready to punch below a historic mine that produced more than a million ounces of gold.

This is the program we’ve been waiting for. The rig is at Mt Egerton with roughly 4,000 metres across 10 holes lined up to test the system at depth.

Mt Egerton pulled 1.29 million ounces out of the ground at around 12 grams a tonne before water flooded it and shut the whole thing in 1906.

More than 90% of the drilling since has stopped above 150 metres, so the deep system (the bit that actually counts), has sat there untested for the better part of a century.

Victorian gold has a habit of getting richer the deeper you chase it.

Fosterville’s ultra-high-grade Swan zone, the discovery that turned it into a cash machine, wasn’t found until drilling pushed past historic workings.

Mt Egerton sits in the same structural corridor as Fosterville, Costerfield and Sunday Creek, and every one of them paid out for whoever chased the grade deeper.

Black Horse has also been given access to reopen the old Sister Rose adit, a horizontal tunnel dug into the hillside that miners once used to haul ore out before it was sealed up over a century ago.

Getting back inside lets them map where the historic workings sit underground, so they can aim the drill at the right spot below them rather than guessing.

Early results were modest, with only anomalous gold from the maiden holes. The depth test is the one that counts.

FUN Lab Commissioned, Resource in Sight

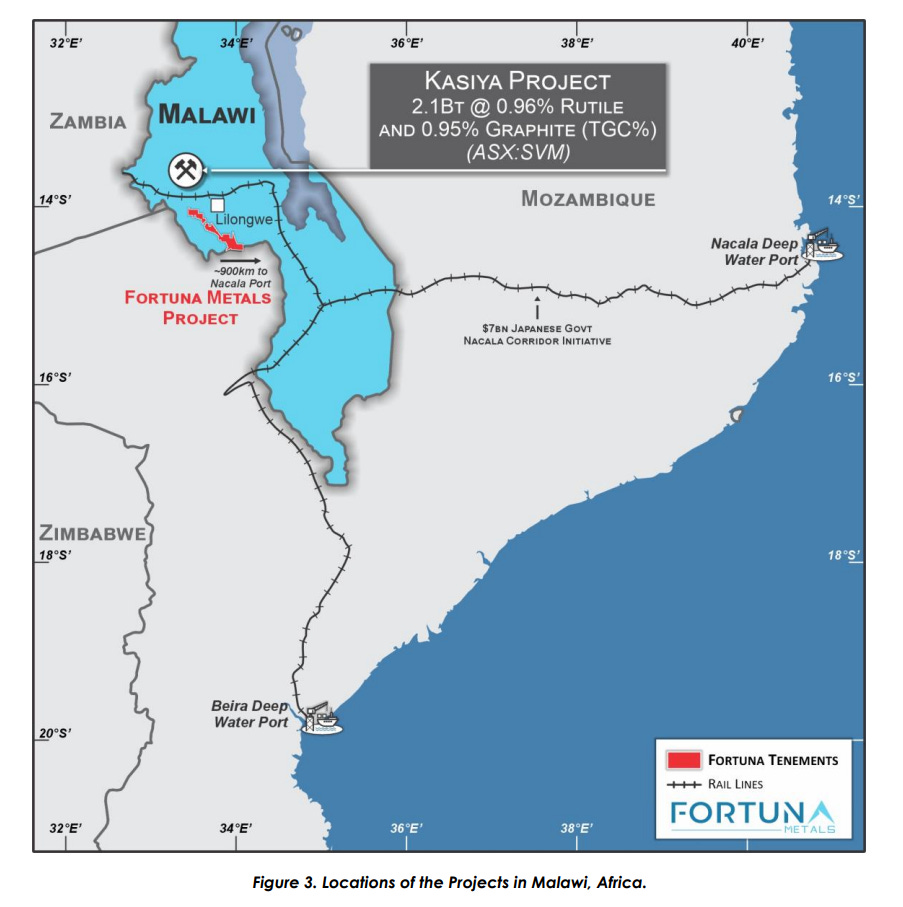

Fortuna Metals (ASX: FUN) has commissioned its own laboratory in Lilongwe, Malawi, a sharp move with a maiden resource bearing down.

For anyone new to the story, FUN is chasing rutile in Malawi, the cleanest titanium feedstock going, and titanium is the light, strong metal aerospace and defence keep wanting more of.

Fifteen technicians have been trained to process samples in-house, with duplicates checked against an external lab for quality control.

Running their own assays cuts both the cost and the turnaround time for Fortuna, handy when you’re trying to feed rutile results into a resource and keep the drill bit moving through 2026.

Around 62% of the 6,000-metre hand auger program is now done, the 5,000-metre aircore program kicks off in early July, and the maiden inferred resource estimate lands the same month.

Resource competent person Richard Stockwell has been on the ground auditing both the drilling and the sample processing ahead of that estimate.

Mkanda sits about 20km south of Sovereign Metals’ Kasiya, the largest rutile deposit in the world, and Fortuna is going after rutile, graphite and potential rare earths across the same ground.

A maiden resource is the catalyst we’ve been waiting on as holders, and the company now has around $15 million in the bank after the recent investment from WndrCo, which funds the aircore program testing depth and the more than 600 holes still to report.

Plenty to keep the news flowing through the back half of the year.

Lithium Bulls Are Back In Charge

Lithium spent two years in the gutter. It has now climbed out, and it is climbing fast.

The metal that gutted portfolios through the downturn is running hard again, and the holders who refused to sell are watching the screen turn green for the first time in a long while.

In China, lithium carbonate is up around 40% this year and roughly 175% on a year ago, sitting near 165,500 yuan a tonne, or about US$24,500.

Grid-scale battery storage is the new driver this cycle, a second engine bolted on next to EVs.

The forecasters who left lithium for dead are now quietly rewriting their numbers upward. Bloomberg has CRU Group, Benchmark Mineral Intelligence and Citigroup all seeing stretched supply push prices past recent highs.

CRU sees carbonate averaging around US$33,900 a tonne next quarter, Benchmark reckons it could touch US$30,000 this year, and Citi has flagged about US$37,000 in Q3.

China is heading into its busier buying season, when battery makers step up their ordering. That has calmed earlier fears the market was carrying too much unsold stock, or that restarted Australian mines like Finniss and Bald Hill would flood it with fresh supply.

Some ASX names have already moved. PLS is up 36% this year, Wildcat Resources (WC8) is up 48%, and Galan Lithium (GLN) is up 23%.

Many others remain muted which may represent opportunity for those who want to back the analyst calls above.

The G7 Wants Out of Chinese Rare Earths

For two decades the West outsourced its rare earths problem to China and tried not to think about it. That's ending.

The G7 has agreed to source at least 40% of the materials for high-tech magnets from outside China by 2030, pushing for 50% as soon as they can manage it.

For anyone building a rare earths project somewhere the West trusts, that’s a tidal wave of future demand with their name on it.

China still controls more than 90% of global processing, and these are the materials inside half the things the modern world runs on, from the EVs in the driveway to the guidance systems steering missiles.

The G7 has now said out loud that it wants out, and the manufacturers and defence buyers chasing that target will be forming a queue outside every developer that can deliver before 2030. There aren’t many of them.

Lynas in Australia and MP Materials in the US already have price floors locked in, Lynas’ through a Japanese buyer and MP’s through the Pentagon.

Those deals set a minimum of US$110 a kilogram for the neodymium-praseodymium oxide that goes into magnets, around twice the market price before they were struck.

The US has gone further again with Project Vault, a US$12 billion critical minerals reserve.

A junior sitting on the right ground in a country the West trusts can suddenly raise money without scrapping for every dollar, with offtakers circling years before they normally would.

2030 is brutally tight for projects that mostly haven’t built anything yet. Processing is the part nobody likes to talk about, and most still have to prove they can turn rock into something a magnet maker will actually buy. Plenty will say they can. Only the best will.

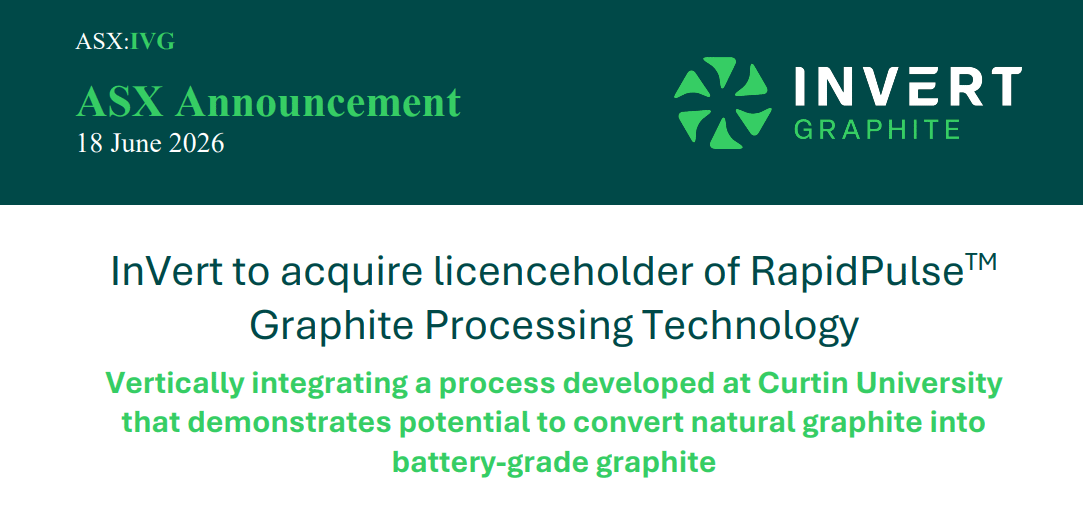

InVert Graphite Says No To Acid

Almost nobody outside China has managed to build a battery-grade graphite plant, and the thing standing in the way is a tank of hydrofluoric acid.

Turning raw graphite flake into the material a carmaker will actually buy is the hard, expensive part, and the usual way to do it leans on hydrofluoric acid. It’s nasty stuff to handle, and a permitting nightmare in the West.

China processes roughly 98% of the world’s graphite, and the acid is a big part of why everyone else keeps stalling.

InVert Graphite (ASX: IVG) caught our eye this week, up as high as 57% before closing the week up 28% after announcing it’s acquiring RapidGraphite and a technology called RapidPulse.

RapidPulse is a process developed at Curtin University that the company says can do that conversion in seconds and hit around 99% purity without any acid involved.

Take the acid out and the cost of building one of these plants outside China drops hard.

Carmakers and governments are desperate for graphite from anywhere that isn't China, and a cleaner, cheaper process lowers the bar to handing them one, assuming it holds up once it leaves the lab.

IVG comes with the Morogoro graphite project in Tanzania and a potential route into downstream processing, and has raised A$2.5 million to fund the trials.

It’s early days for IVG and they are not a portfolio company for us, but it's one we'll be keeping an eye on.

Billions for Semiconductors and AI Chips

Intel spent years as American tech's cautionary tale, the giant that passed on the iPhone chip and then watched Nvidia run away with AI. It's clawing its way back now, and this week Apple and the White House gave it another shove.

Trump confirmed this week that Apple has agreed to work with Intel to design and build chips on American soil.

Intel shares jumped more than 10% on the day and are now up past 240% for the year. The US government is on the register too, after taking a stake back in August.

When Washington starts buying into chipmakers directly, the onshoring push has real teeth.

There are indicators everywhere that the big money is piling into chips, and it shows no sign of slowing.

Qualcomm (NASDAQ: QCOM), one of the biggest names in mobile silicon, is reportedly circling an AI silicon startup for between US$8 and US$10 billion. That's the going rate now for a genuine edge in AI.

We’re not going to pretend the local tiddlers are about to land Apple contracts.

But when the largest companies and governments on the planet are paying up for chips and racing to onshore supply, the ASX small-caps with exposure to that supply chain tend to catch the slipstream. That’s the corner of the market we’re watching closely.

The Week Ahead

We’re into the last full trading week of the financial year, which usually means thin volumes and not much news. June tends to be a soft month anyway, as people crystallise losses and buying dries up while portfolios get a once-over to setup for the second half.

So we’re not expecting much. Maybe a drilling update or two, but nothing major across the portfolio. If commodities take a breather and nothing flares up in the Middle East or the drone and tech space, we’d be happy enough heading into July.

Our eyes will be locked on the Socceroos on Friday. A win or a draw against Paraguay sends Australia through to the Round of 32 in second place, and even a loss leaves the door open as one of the best third-placed teams.

Fingers crossed. Till next week.