Weekly Wrap: RIU Buzz, Discovery Drought, and the Copper Flip

Record highs on the ASX as conference floors fill and capital returns to resources

Four years ago, every second booth at the RIU Explorers Conference was a lithium story. This year in Fremantle it was gold and copper, and the booths had lines.

Tuesday reportedly set a one-day attendance record. Perth brokers were out in force, a solid contingent flew in from the east coast, and funds, family offices and delegates from the majors were all working the floor.

We spent three full days on the ground in Fremantle this week, and our full rundown of RIU Explorers Conference 2026 can be found here.

Meanwhile, the ASX 200 pushed to a fresh record high this week, backed by strong earnings from the big end of town. From Telstra to NAB through to BHP and Rio Tinto, reporting season reminded investors why the majors anchor portfolios - the big end of town are making billions.

And while the large caps did the heavy lifting, the bottom end of town has been just as busy. Another conference floor packed out, drill programs funded, and discoveries being rewarded in a way we haven’t seen for a long time.

What caught our eye this week:

RIU Explorers Conference: Record attendance as capital circles

Discoveries are lacking: Exploration dollars are being spent, but true greenfields finds remain scarce.

BHP & RIO: Relying heavily on copper to pick up iron ores slack

The Middle East: Oil above US$70/b and gold above US$5,000/oz as geopolitical risk returns.

Lithium: Majors restart plants and deploy billions, signalling a shift in tone for the battery metal.

RIU Explorers Conference Fremantle

Conferences like RIU are a live barometer of risk appetite, and this one said the money is coming back to the junior end of the market.

Gold sitting around record levels and copper holding firm has changed the conversation. If you want to know where the market’s head is at, look at which presentations filled rooms and which MDs couldn’t get off the floor. This year, it was gold and copper, and it wasn’t close.

We sat in on presentations, caught management between sessions, and had the sort of off-stage conversations that never make it into slide decks. Many brokers we spoke with expect both gold and copper prices to hold strong through 2026, giving a launch pad for small-cap explorers that are yet to return results but are drilling.

Once the clock ticked past 5pm each day, the conversations moved from the booths to the bar and poolside functions that ran late into the night. If you want to speak to an MD at RIU, you walk up and have the conversation. That accessibility is what keeps this conference on the calendar year after year.

A few companies stood out on the presentation floor:

Terra Metals (ASX: TM1) has been one of the headline stories of the past eight months, up roughly 900% off the back of its Dante PGE-copper-nickel discovery in Western Australia. Some of the highest-grade PGE assays ever reported globally, and they were one of the most popular booths at the conference. The focus now is testing deeper for high-grade feeder zones beneath Dante, and with copper and PGE prices both running, results from that program could move things again.

New Murchison Gold (ASX: NMG) is up around 600% since last year's RIU. In twelve months they've reported an ore reserve, secured mining approval and started producing and selling gold. That pace of development made CEO Alex Passmore one of the most sought-after presenters at the conference. Exploration upside sits on top of existing production, which is a combination that draws attention in a market like this.

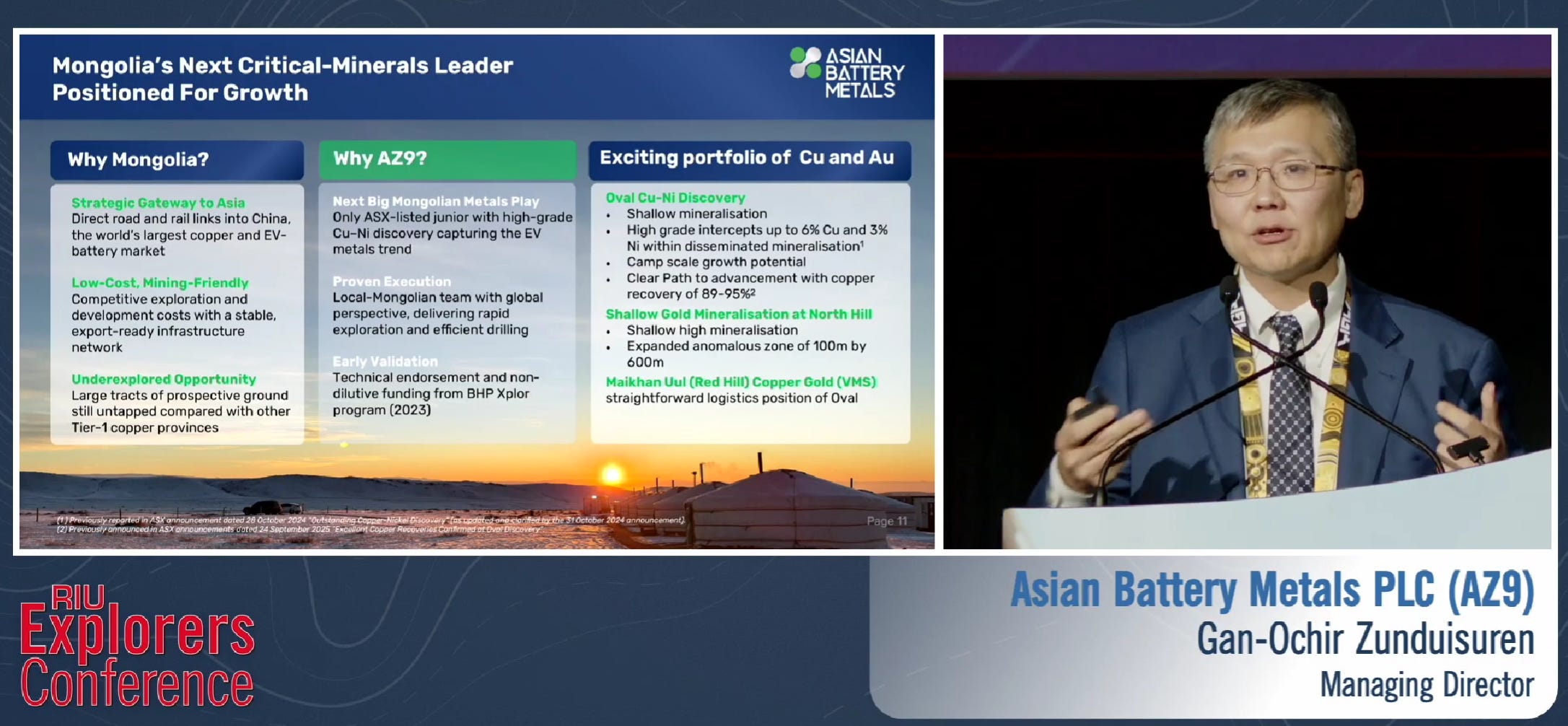

Our portfolio company Asian Battery Metals (ASX: AZ9) presented to a near-full room on Wednesday afternoon. The detail that caught our ear was timing - the next phase of drilling is due to kick off within weeks at Oval, with the focus on expanding the footprint at Maikhan Uul and North Hill. Rigs are about to turn on proven copper and gold mineralisation, and you could see brokers actively taking notes as the timeline was laid out.

You can find AZ9 Managing Director Gan-Ochir Zunduisuren’s full presentation from RIU Explorers here.

We also ran into board members from our other portfolio companies Fortuna Metals (ASX: FUN), Exultant Mining (ASX: 10X) and Top End Energy (ASX: TEE) across the three days, all fielding steady interest from brokers and investors.

More Exploration but Less Discoveries

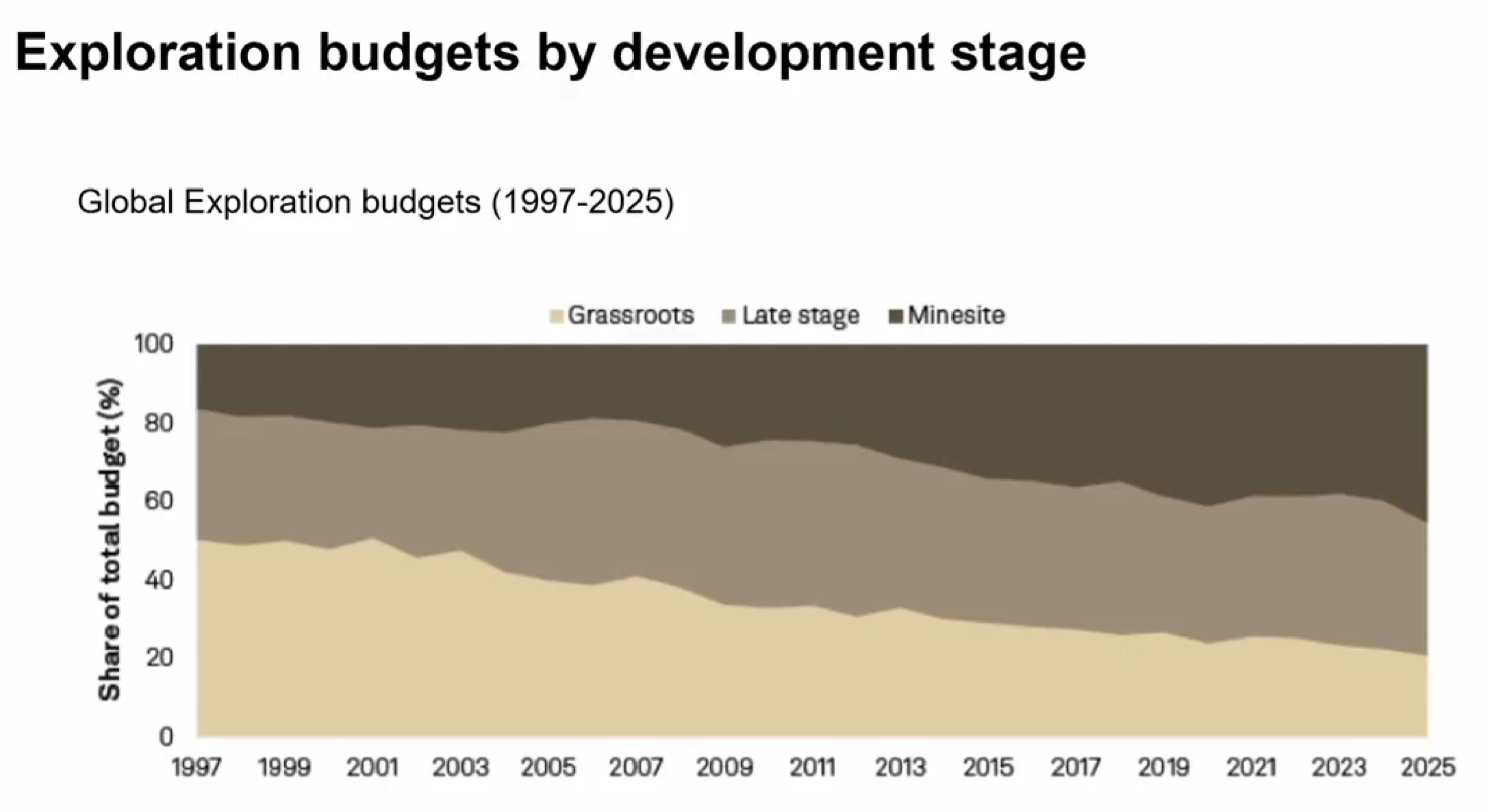

The industry is spending more on exploration than it has in years, and finding less.

S&P Global presented the data at RIU this week and it’s hard to argue with. Global exploration budgets keep climbing, but most of that money is going into extending known deposits rather than punching holes in new ground.

Newly discovered contained copper has fallen sharply since the 1990s. Roughly 400 million tonnes have been added to global copper resources since 2005, but the vast majority came from expanding mines that already existed. The industry is getting bigger without actually discovering anything new.

Gold is the same. Five major gold discoveries globally since 2020. Five. Average discovery sizes have also shrunk to around 3.5 million ounces, well below the previous decade’s average.

That’s partly why TM1 ran 900% and NMG ran 600% over the past twelve months. When the pipeline is this thin, a genuine greenfields find gets repriced fast because there’s so little competition for capital. The explorers drilling fresh ground in this market are the ones with the most leverage if they hit.

BHP and RIO: Copper is Doing the Heavy Lifting

For the first time, BHP made more money from copper than iron ore, and that’s a big tell for where the cycle is heading.

In the six months to December, copper contributed US$7.95bn in operating earnings versus US$7.50bn for iron ore, with copper now making up 51% of group earnings. Realised copper prices jumped about 32% over the year, while iron ore demand out of China flattened and prices rolled over, even as unit costs in the iron ore business rose.

Iron ore still matters, but it’s increasingly treated like a mature cash cow while copper is being priced as the growth engine tied to electrification, data centres, EVs and grid spend.

Rio told a similar story from a different angle. Net profit landed at US$9.97bn, the weakest since 2020, with softer iron ore pricing and costs creeping higher in the Pilbara. Copper picked up the slack as Rio’s Mongolian mine Oyu Tolgoi keeps ramping and realised prices improved.

Rio held the dividend at US$4.02 a share but warned Pilbara mining costs could rise again next year, which tells you margins are getting tighter. Management is pushing harder into copper across the growth plan and exploration budget, and BHP is doing the same.

When the two biggest miners on the ASX are both hunting copper projects, it tells you something about where the next decade is heading. Juniors with drills turning on copper targets are in pole position if they can hit.

Trump, Iran and What It Means for Oil and Gold

Geopolitics is pricing back into markets, and this time it's centred on Iran.

Trump has given Tehran 10 to 15 days to agree to a nuclear deal, with two carrier strike groups already in the region and the Pentagon reportedly ready to act if talks collapse. Prediction markets are putting odds north of 50% on some form of US military action in the coming weeks, and asset prices are already moving.

Brent crude oil, roughly two-thirds of the world's internationally traded physical oil crude, has climbed to near six-month highs above US$70 a barrel as traders price in potential supply disruption through the Strait of Hormuz, a chokepoint that handles a huge share of global oil trade.

Goldman Sachs has flagged that even a shortfall of 1 million barrels a day could lift oil prices significantly if the strait's security comes into question.

Gold is holding above US$5,000/oz and every escalation seems to add another layer to the bid. At these levels, fear is doing as much work as fundamentals, and investors are piling into bullion as a hedge against whatever comes next.

Oil rises on supply risk, gold rises on uncertainty, and equities tend to cop it when energy costs spike. We’ll be watching this one closely over the coming days.

Lithium: The Majors Are Writing Cheques Again

After two years in the doghouse, lithium is starting to get some attention again.

Spodumene peaked at roughly US$8,200/t in late 2022 and spent the next two years sliding to lows near US$575/t by mid-2024. Prices have since clawed back to around US$2,100/t on the back of Chinese production curbs and renewed EV demand, and the majors are starting to put real money back in.

That improvement is now translating into real capital decisions:

PLS (ASX: PLS) is restarting its Ngungaju plant by July, backed by a deal with China’s Canmax that floors the price at US$1,000/t.

Wesfarmers is looking to potentially double the size of its Covalent Lithium operation in Western Australia, which is already making money.

Rio Tinto is committing US$300m to increase its stake in Canadian lithium miner and processor Nemaska Lithium, a joint venture with the province of Quebec.

When majors reopen plants and deploy billions after a downturn, it signals confidence the worst of the lithium winter has passed.

Two years ago nobody wanted to touch lithium. Now PLS is restarting a plant, Wesfarmers is looking to double its throughput and Rio is the majority holder in a Canadian processor. The cycle looks like it's turning.

Worth noting for juniors though - all three are expanding what they already own. Nobody is out there buying discoveries from small-caps the way they are in copper. For a lithium junior, that means finding the ore is only half the battle.

You've still got to fund it, process it and sell it into a market where the big end of town is already entrenched. That hardly ever ends well.

The Wrap

For small-cap explorers, this feels like one of those windows where sentiment, capital and commodity prices all line up.

That doesn’t guarantee anything, but the companies with drills turning and results due are walking into about as good a setup as you could ask for. And the RIU floor this week told us the appetite is there from the broker and fund side.

The Iran countdown clock hits zero inside the next two weeks (though Trump is known to extend a deadline). If that escalates, oil and gold both move higher and equities get choppier. If it resolves, the risk premium comes out and things settle.

Either way, it's the wildcard that could soon override everything else we've covered this week.

Oh, and the US Supreme Court struck down Trump’s emergency tariffs on Friday night. He signed a new 10% global tariff under a different law before the ink was dry, and flagged more to come. Markets will need to digest that next week.

From our side, it’s as busy as it’s been all year. Drill results coming, portfolio companies advancing, and a market that’s actually rewarding the work.

Till next week.