Weekly Wrap: SpaceX Wants Billions, Silicon Valley Wants Malawi, and DXN Soars

SpaceX asks the public for US$75 billion, smart money lands on Fortuna, and Opthea sheds 97.5% in a single session. Plus: drones, graphene, and a price query gone wrong

The world's richest man wants your money. About US$75 billion of it.

This week Elon Musk and SpaceX put their hand out for one of the biggest cheques public investors have ever been asked to write, a raise that would value the company at roughly US$1.8 trillion.

ASX investors can get a slice too.

To put that in context, it's about what the entire ASX top 100 is worth combined

SpaceX started life as a rockets company, but that’s almost the boring part now. These days it’s pitching itself as a satellite internet giant and an AI infrastructure player that could end up one of the most important tech platforms of the next decade.

Whether it’s actually worth US$1.8 trillion is something the market will sort out in a couple of weeks when it lists.

Back in small-cap land, news was dropping everywhere. Silicon Valley money turned up in Malawi, AI1 went into a halt chasing a world first, EVG quietly added to its foundations, and DXN reminded everyone that AI stories work a lot better with a signed contract attached.

We also caught one of the strangest announcements of the year, a brutal biotech wipe-out, and a drone supplier having the week of its life off the back of the market's hottest theme.

Let’s get into it.

Silicon Valley money arrives in Malawi as WndrCo backs Fortuna Metals

Adisyn shareholders brace for a Milestone 2 verdict

Evion adds Arthur Sinodinos and delivers positive EBITDA

KTK keeps climbing as drone demand gathers momentum

DXN proves AI still works when revenue is attached

Opthea's 97.5% collapse and the cold reality of biotech

SRJ's awkward SpaceX moment and the price query that followed

Silicon Valley’s Smart Money Lands in Malawi

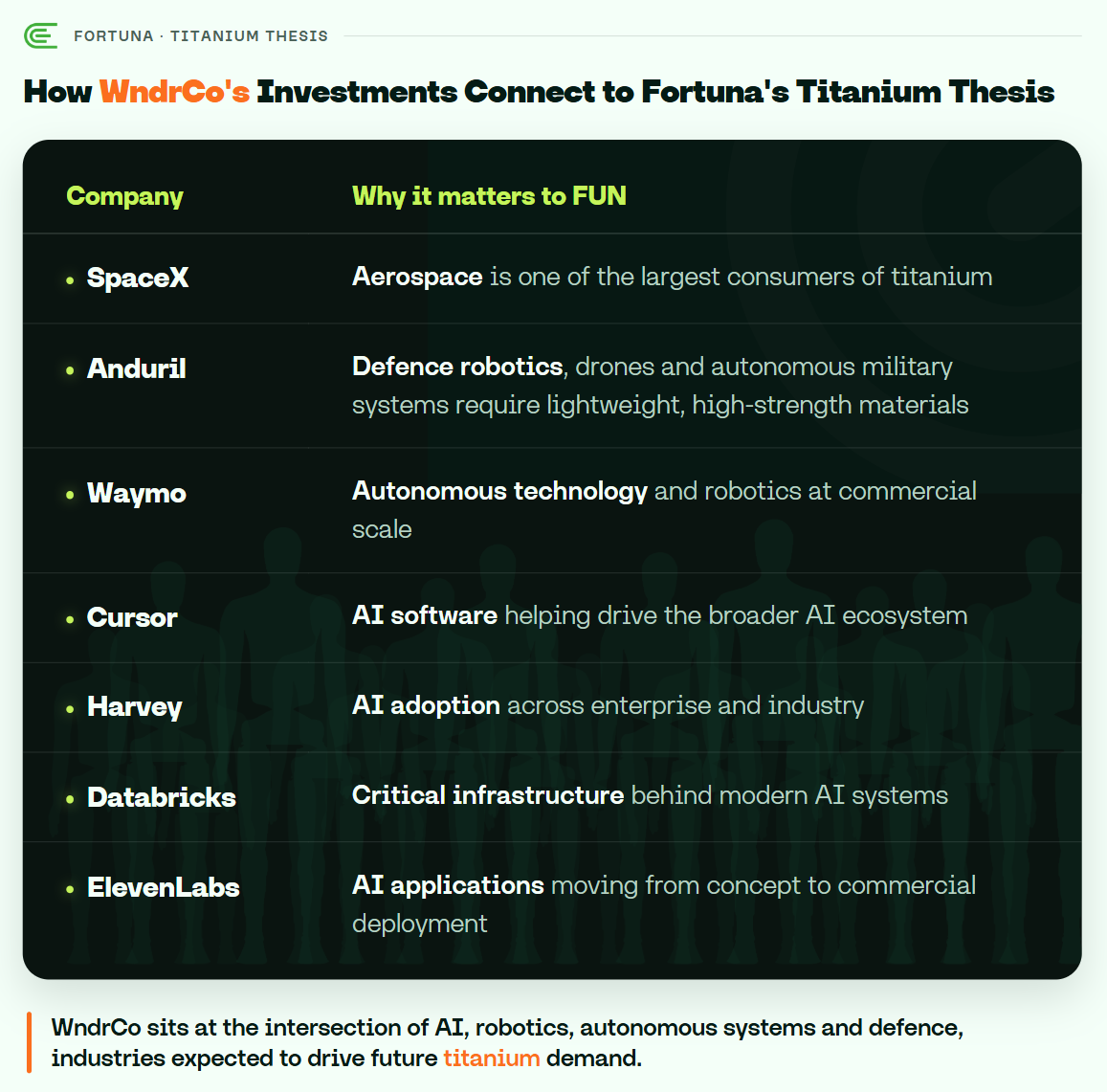

One of the most connected technology investors in Silicon Valley has just written an $8.6 million cheque to Fortuna Metals (ASX: FUN), taking a 19.9% stake and becoming its cornerstone shareholder.

The investor is WndrCo, the US fund founded by Jeffrey Katzenberg and Sujay Jaswa, with more than US$3 billion under management and a track record of backing some of the biggest tech winners of the past decade.

Names in the portfolio include SpaceX, Anduril, Waymo, Databricks, Figma, Airtable and 1Password.

This is smart money. It spends its time working out where technology is heading before the rest of the market catches on.

WndrCo is arriving just as humanoid robotics moves from theory to production. Tesla wants to build millions of Optimus robots, defence contractors are deploying autonomous systems, and every one of those machines needs lightweight, high-strength materials.

Titanium sits near the top of that list, and rutile is one of its key feedstocks (the raw material you process to get the metal).

The money itself is meaningful, but the network may prove even more valuable.

With roughly $15 million in the bank after the raise and a cornerstone backer who understands where titanium demand is heading, Fortuna goes into the second half of the year with options. The stock finished the week at 12 cents. You can find our full write-up here.

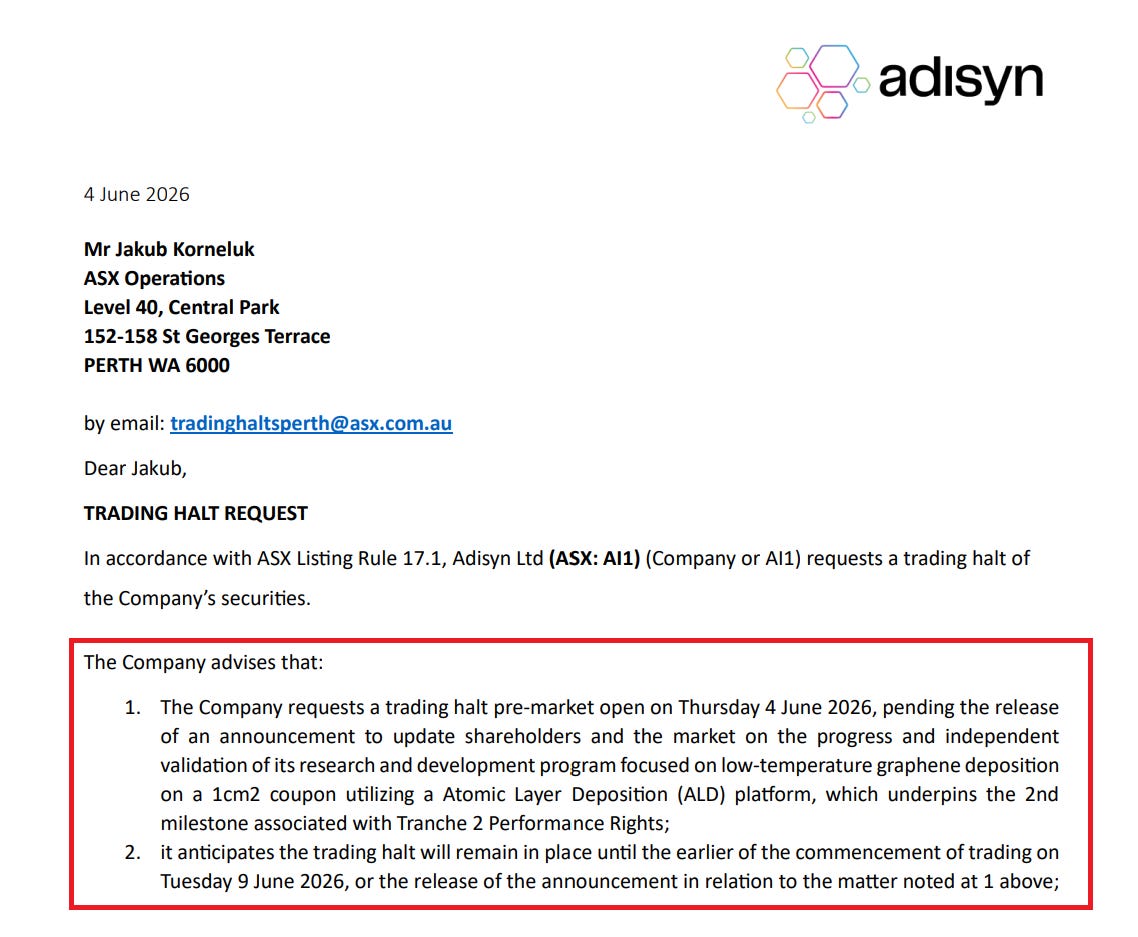

Adisyn Waits for a Defining Moment

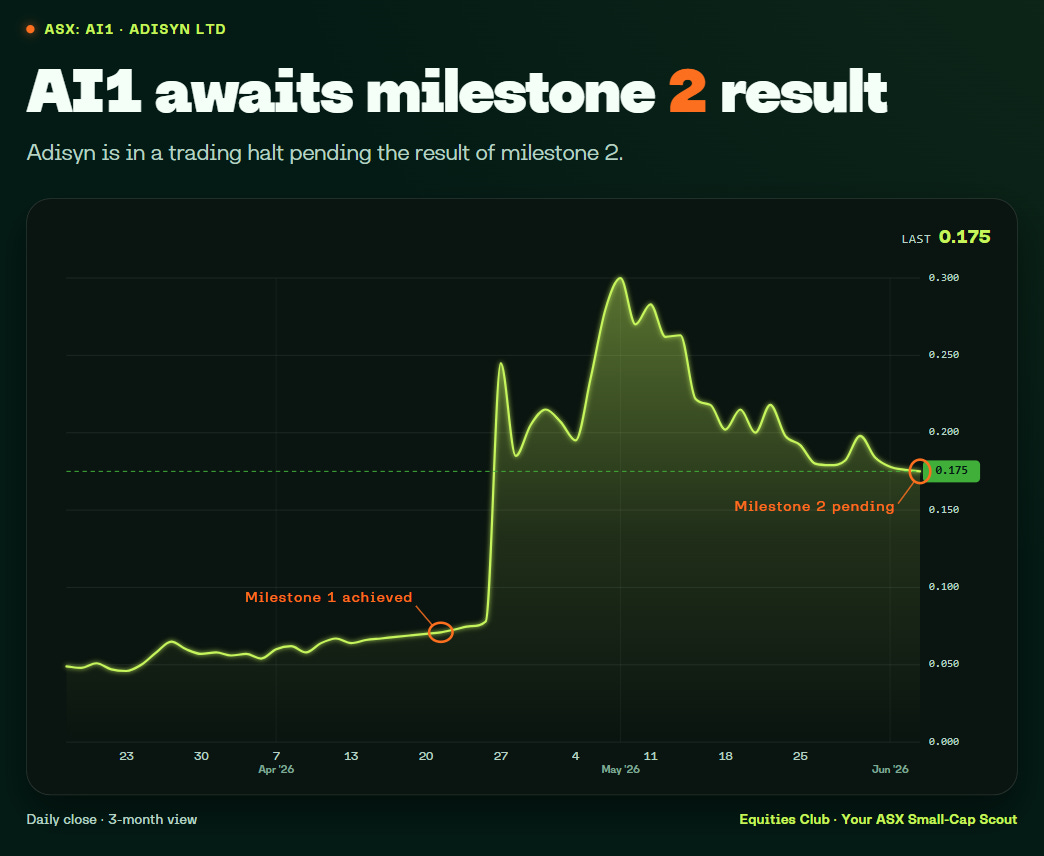

Adisyn (ASX: AI1) is one of ours. We backed it at 6.8 cents and it's now 17.5 cents, so we're watching this one as closely as anybody.

The company went into a trading halt this week pending independent validation of Milestone 2 in its graphene semiconductor program.

In plain terms, it needs to show it can lay down graphene reliably and repeatably below 300°C across multiple independent runs, with even coverage right across the test surface.

Management reckons that if it lands, nobody anywhere in the world has pulled it off before.

The whole case rests on graphene eventually replacing or improving the tiny connections that move data around a chip, the interconnects, which are one of the bottlenecks the industry keeps running into.

Holders have already had a taste of what a result does here. When Milestone 1 came through in January, the stock ran from around 6.8 cents to almost 30 before settling back under 20.

Milestone 2 carries even more weight.

There’s no guarantee the result lands the way shareholders are hoping. If it does, and the company keeps moving towards commercial engagement with semiconductor groups, Milestone 1 showed how the market tends to respond.

Bring on Tuesday.

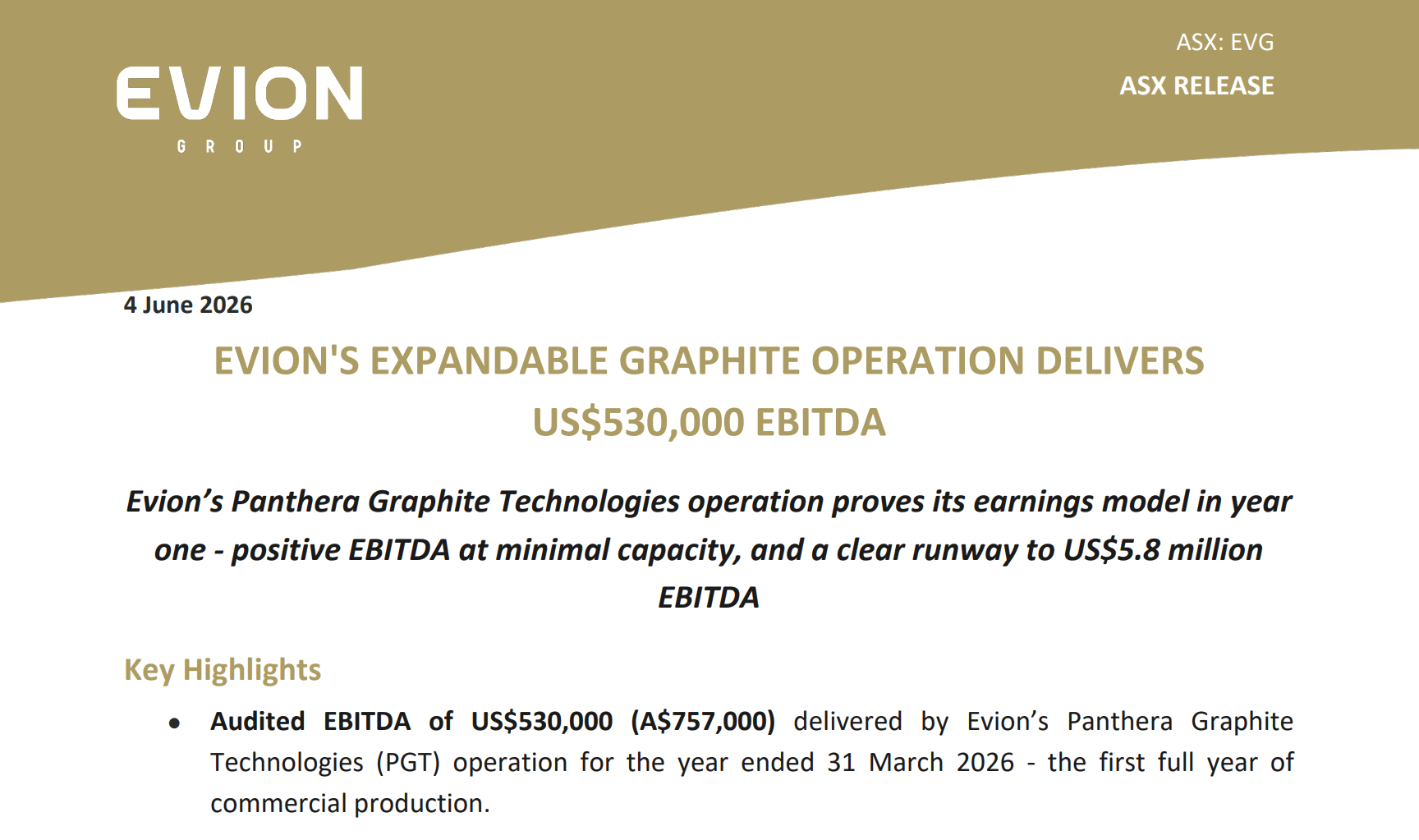

EVG Keeps Adding Bricks to the Wall

The share price didn't show it this week, but Evion Group (ASX: EVG) kept putting runs on the board.

First came the appointment of former Australian Ambassador to the United States Arthur Sinodinos AO as a strategic adviser. For a $29 million company, landing someone whose network runs that deep through Canberra, Washington and critical minerals policy is a rare get.

Later in the week EVG’s Panthera Graphite Technologies operation delivered audited EBITDA of US$530,000 in its first full year of commercial production. The eye-catching part was that it did it while running at only 20-25% nameplate capacity (the maximum the plant is built to produce), while still paying down debt from operating cash flow.

Management is now mapping a path towards US$3.4 million EBITDA at Stage 1 capacity and US$5.8 million at Stage 2.

So EVG has a critical minerals business that actually earns money, a Nevada fluorspar project sitting in the middle of America's supply-chain scramble, and now an adviser plugged into the circles writing that policy.

The fluorspar backdrop shifted in Evion’s favour this week, and it came out of China.

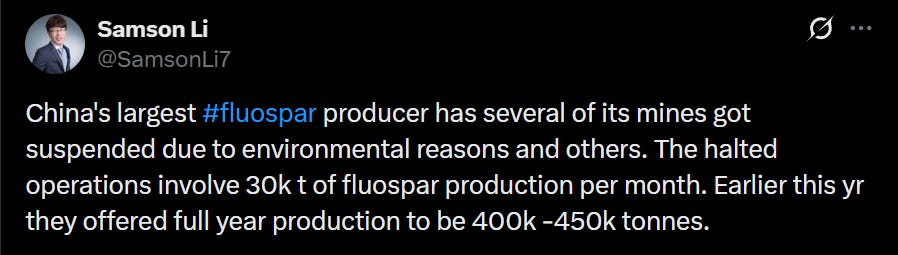

China Kings Resources, the country's biggest fluorspar producer, has suspended several mines and launched a self-inspection on environmental and safety grounds.

China supplies most of the world's fluorspar, so when its largest producer pulls tonnes offline, everyone downstream feels the pinch.

Every shutdown like that makes a non-Chinese source worth a bit more, and a Nevada project feeding America's critical minerals push sits on the right side of it.

The market marked the stock down this week, but the underlying story keeps getting stronger.

KTK Keeps Finding Buyers

Plenty of stocks spike for a day and disappear. KTEK Group (ASX: KTK) is doing the opposite.

Another one of ours, backed from the 20-cent IPO, it climbed another 50% this week, from 32 cents to 48 on better than $5 million of turnover, as the market kept chewing over last week's news that deliveries had resumed after some supply-chain strife. On paper that's a fairly standard update. The buying says investors see something bigger.

What they're looking at is where KTK sits in a defence sector changing by the month.

The company makes composite airframes and the electromechanical guts of drones for Tier-1 manufacturers, which plants it inside one of the fastest-growing corners of defence going around.

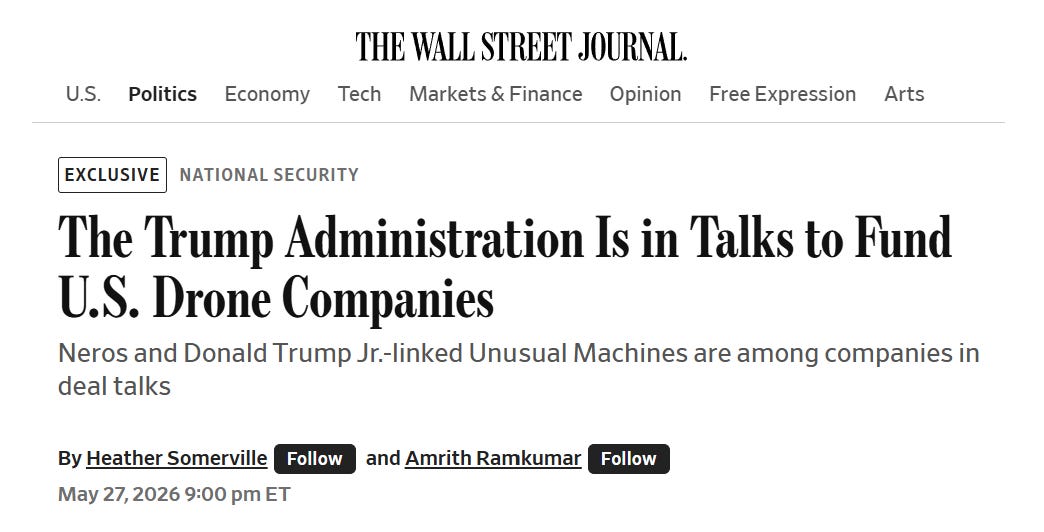

The backdrop keeps helping, with reports only last week that the Trump administration is weighing funding to prop up domestic drone makers and shore up America's supply chain.

Management has talked about taking its ‘cordless factory’ model into the US, setting up small production sites right next to customers rather than building one giant plant. That idea makes a lot more sense if Washington starts tipping real money into home-grown drones.

For now the market's treating drones less like aerospace and more like ammunition, and that tailwind is still blowing hard.

DXN Finally Gives the Market Something Real

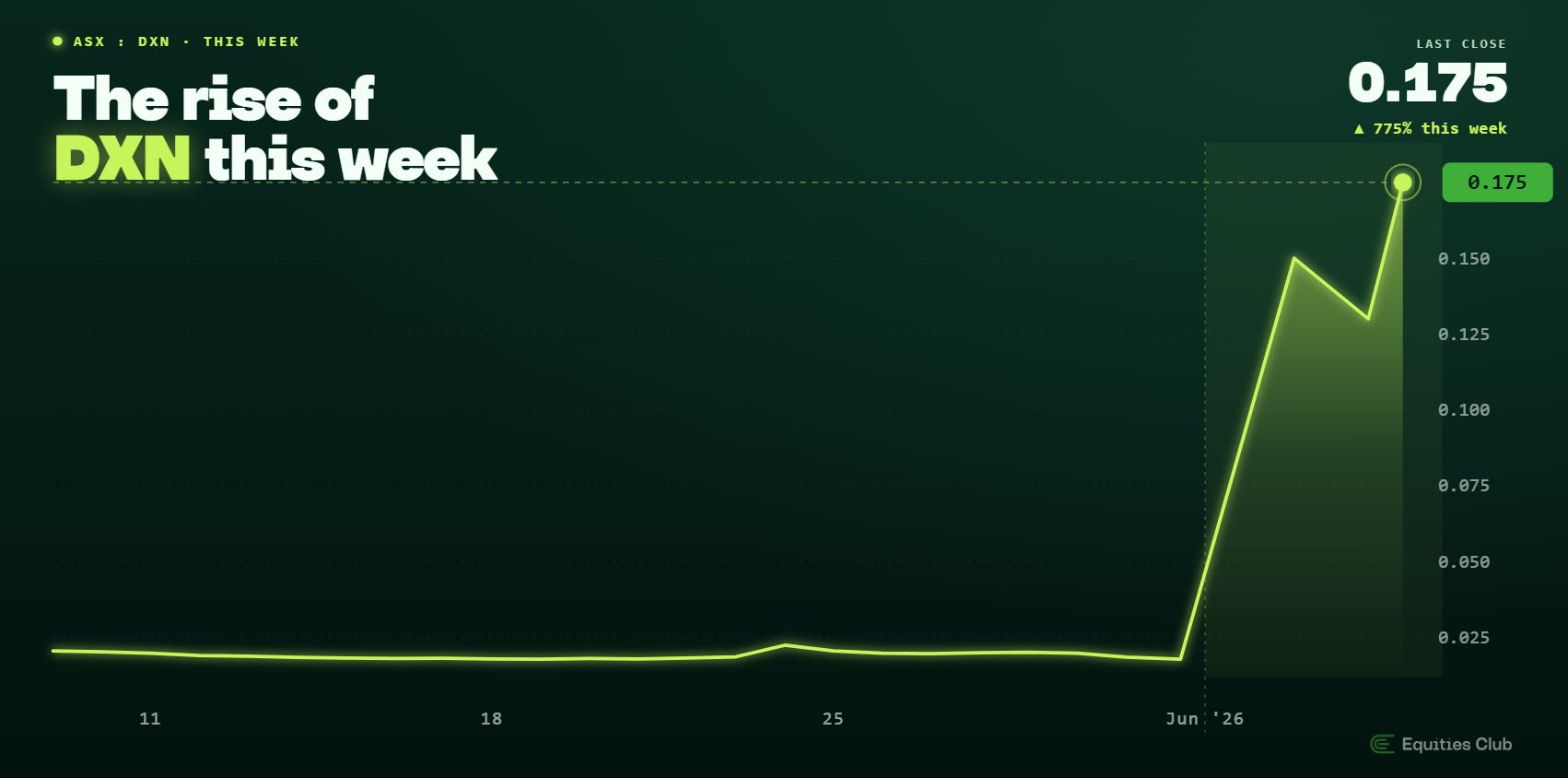

The most talked-about small-cap of the week was DXN (ASX: DXN), and no wonder, it finished up 775%.

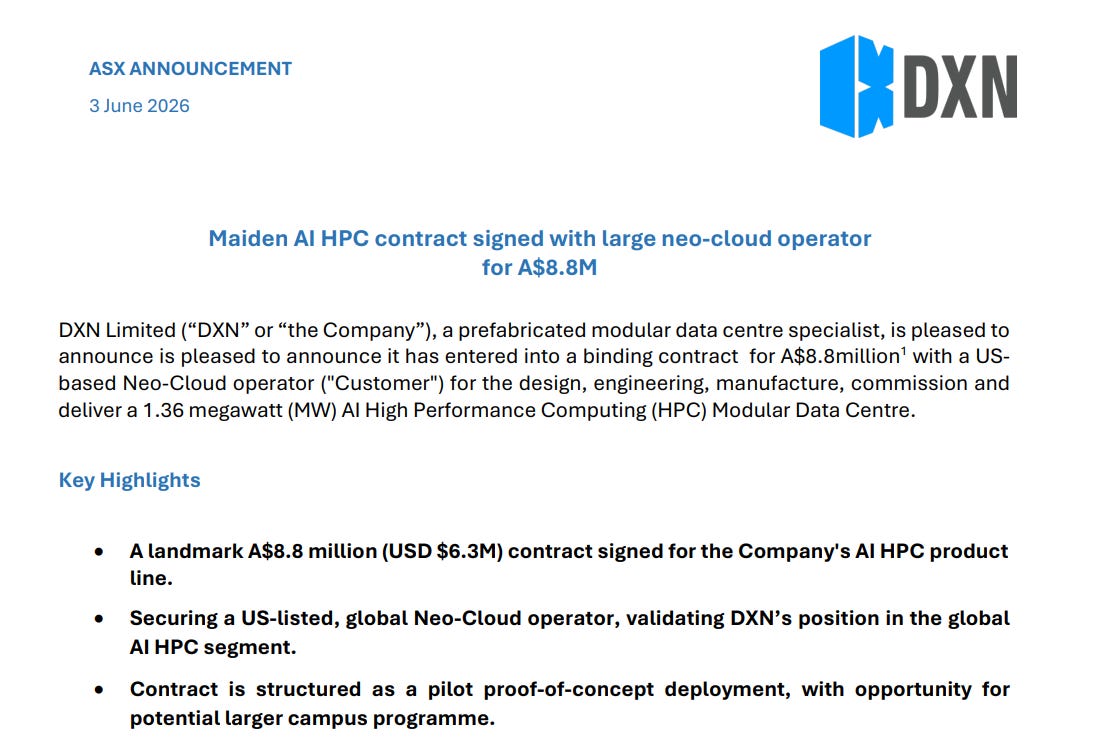

The stock ripped higher after signing a binding $8.8 million contract with a US-listed neo-cloud operator (a newer breed of cloud provider built specifically for AI workloads) to design and build an AI modular data centre.

This one moved because of a signed contract with revenue and a delivery attached.

It stood out in a week where a lot of the market’s biggest movers were still running on reinstatements, capital structure changes, speculative bets or simple repricing.

The contract is a pilot deployment, but management believes a clean delivery could open the door to follow-on work north of US$200 million.

It also lands square in the right theme, with AI infrastructure starting to bleed into the defence-grade and sovereign computing that governments want kept onshore.

The one blemish came late Friday, when two directors trimmed part of their holdings, worth roughly $78,000 and $130,000.

After a move that size, few would begrudge them taking a little off the table.

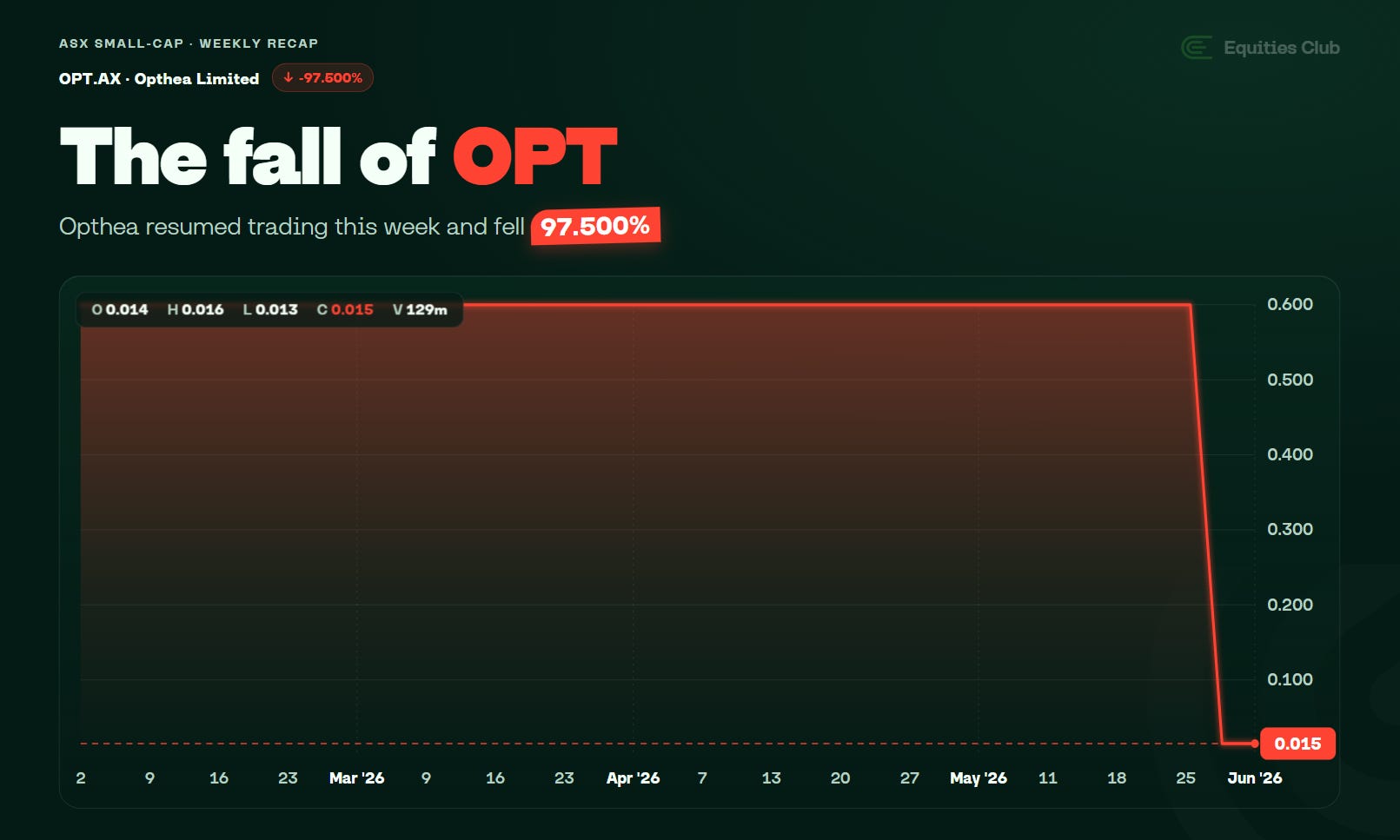

OPT Shows How Brutal Biotech Can Be

Few charts this year have looked uglier than Opthea's (ASX: OPT).

The company came back to trading this week after a long suspension and immediately lost around 97.5% of its value, dropping from roughly 60 cents to just 1.5 cents.

The collapse had been building for months. A late-stage drug trial failed (Phase 3, the final round before a treatment can be approved), in this case for a common eye disease that causes vision loss in older people. After that, the company had to rethink what it would become next.

The old Opthea is gone.

What's left is a much smaller company built around its remaining drug candidate and a new focus on a rare lung disease called LAM, with $31.2 million in the bank and an 18-month plan to develop it. That's a long way from the business that went into suspension.

Biotech is one of the highest risk/reward corners of the market. Years of work and hundreds of millions of dollars can vanish on a single failed trial.

Sometimes the science works. Sometimes it doesn’t.

Opthea is what the second one looks like.

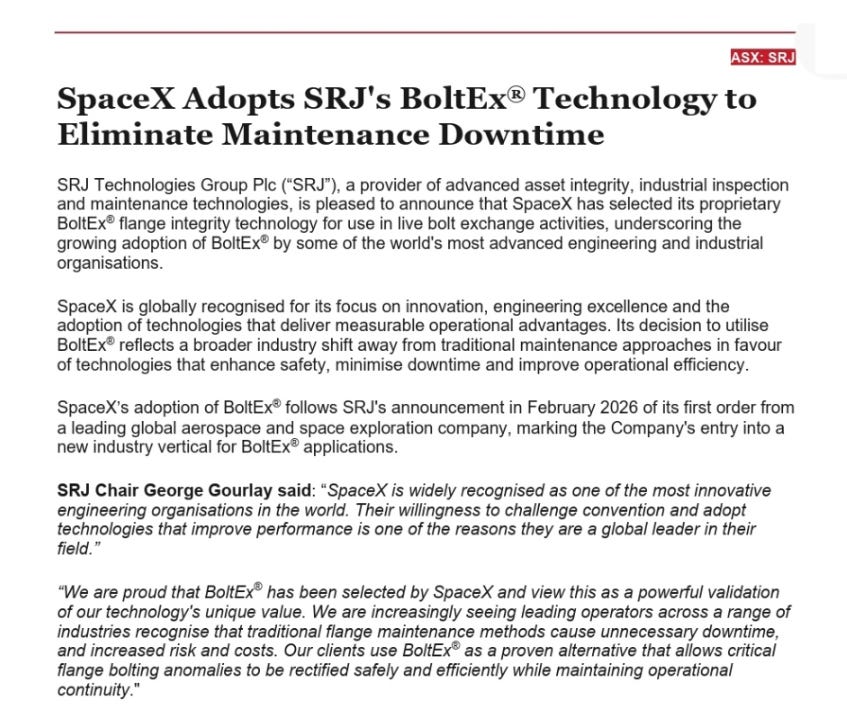

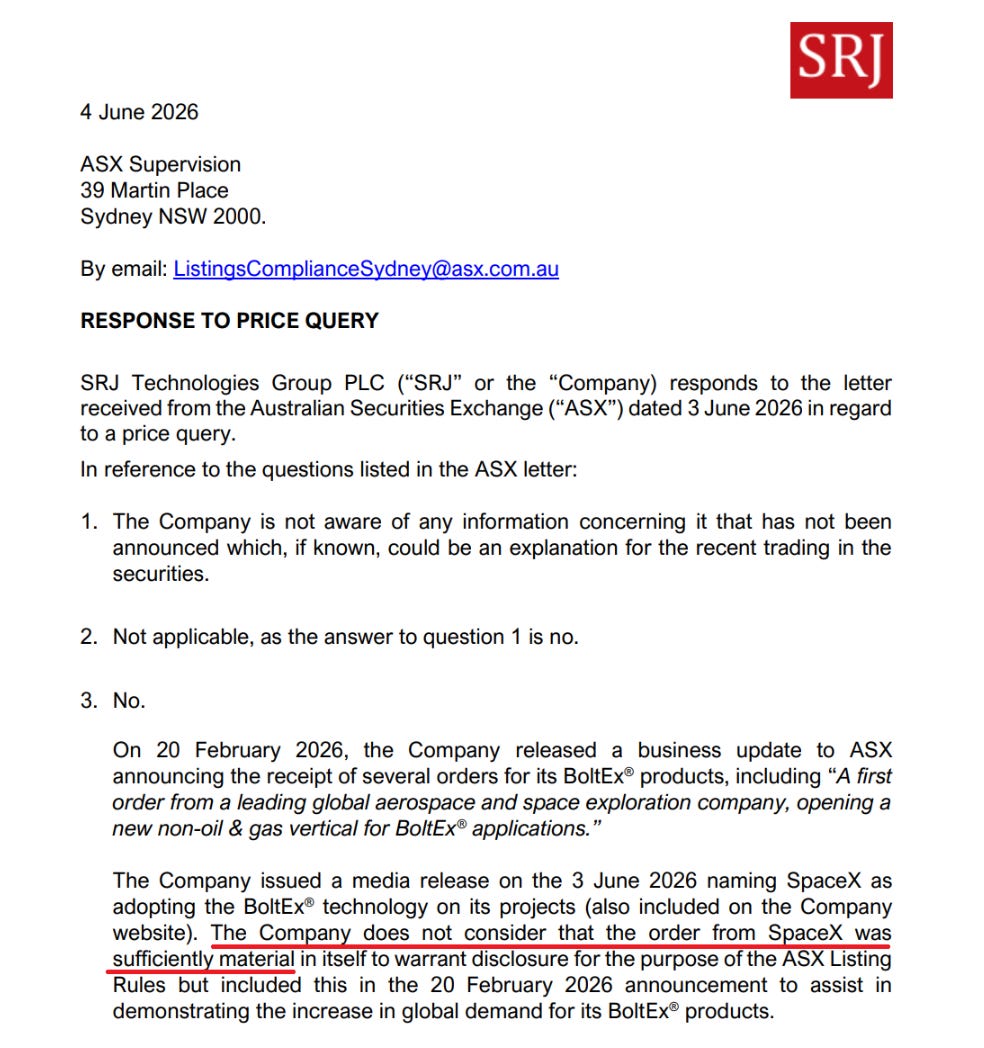

SRJ Gets Itself Into an Awkward Spot

Which brings us back to where we started, only at the other end of the size scale.

SRJ Technologies (ASX: SRJ) was probably the strangest story of the week.

The company emailed shareholders to reveal that SpaceX had adopted its BoltEx technology, a maintenance fix designed to keep critical infrastructure running while bolts are swapped out.

For a small-cap, that’s validation you dream about. SpaceX is one of the most demanding engineering shops on the planet and doesn’t hand out endorsements lightly.

Investors piled in. Shares jumped more than 50% at one stage before the ASX stepped in with a price query.

Then it got awkward. SRJ told the market operator the SpaceX adoption wasn’t material enough to warrant an announcement, and that the underlying order had already been referenced in an earlier update.

Flagging something straight to shareholders and then calling it immaterial when the regulator taps you on the shoulder is not a great look.

The stock still finished the week up 23%, but questions linger.

Having SpaceX deploy your tech is still real validation. The challenge for SRJ now is turning it into revenue and orders investors can actually measure.

The Week Ahead

Tuesday morning is the one to watch. Adisyn comes back from its halt to tell the market whether it can deposit graphene below 300°C, the core of Milestone 2.

We'll also be keeping half an eye on gold after Friday's drop to see whether it steadies, and on copper to see whether it holds its ground.

US markets fell on Friday night, so Monday opens with the question of whether we follow them down or shrug it off, though with Victoria on a public holiday we'd expect a fairly muted session either way.

As we roll into June, the bigger question is whether the market holds up over the coming weeks. Whichever way it breaks, we're expecting a solid run of news out of our portfolio companies.

Till next week.