Top Six on the Planet, Eight Metres Deep

FUN's maiden rutile resource just landed. The deeper drilling starts now.

For a year now we’ve been writing about a company drilling beside the biggest rutile deposit on earth.

Fortuna Metals (ASX: FUN) just proved up one of its own.

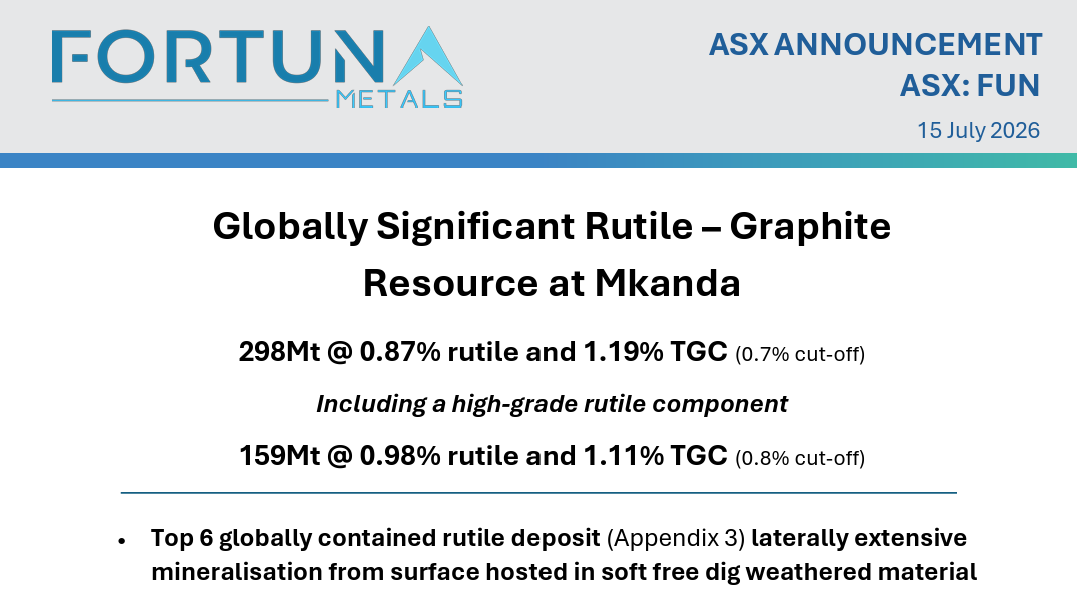

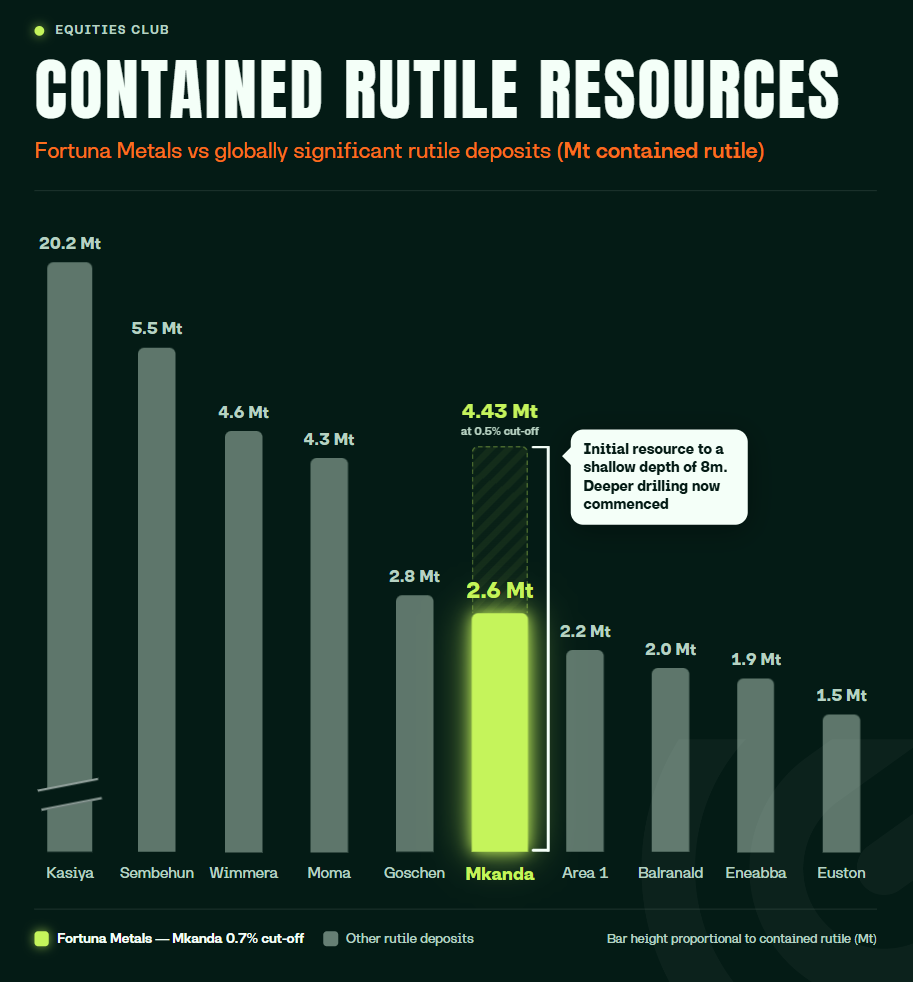

FUN’s maiden resource, announced this morning, puts its Mkanda project in central Malawi at 298 million tonnes at 0.87% rutile, for 2.6 million tonnes of contained rutile.

On the company’s own ranking, that lands it top six on the planet.

The headline number uses a 0.7% cut-off grade, meaning only ground above that grade gets counted. Lower the bar to 0.5% and Mkanda already holds 4.43 million tonnes of contained rutile.

And FUN got all of it on hand augers alone, shallow holes averaging 8.4 metres that mostly stopped at the water table with the rutile still running underneath them.

The aircore rigs that arrived last week drill more than three times deeper.

Funds that won’t touch an explorer without a JORC resource can now run Mkanda through their models. And the company can start the studies that work out what a mine here would actually cost to build and earn.

At 10.5 cents a share, the company carries a market cap of around $33 million, with a very handy $15 million in the bank, most of it from WndrCo, the Silicon Valley fund that bought close to a fifth of the company in June.

Inside a Top-Six Resource (So Far)

Mkanda covers 658 square kilometres of the Lilongwe Plain in central Malawi, flat farming country where tropical weathering has spent a few million years quietly doing FUN's prep work.

The rain and heat broke down the rock and washed the light minerals away, and the heavy minerals (the rutile), stayed put and piled up near surface.

Within the headline number sits a higher-grade heart of 159 million tonnes at 0.98% rutile, above the average grade Sovereign Metals (ASX: SVM)carries at the biggest rutile deposit in the world next door.

FUN now has both the tonnes and the grade, which is a rare thing to see in a maiden resource.

The rutile itself came back at 96.6% TiO₂ from a bulk sample earlier this month, which is higher than product the established producers have shipped for decades.

Buyers pay a premium for rutile that clean because it skips a whole refining step on the way to becoming titanium.

There’s 3.55 million tonnes of contained graphite sitting alongside it at 1.19% too, a second product that could pay its own way once the metallurgy is sorted.

Then there’s Kahuna, a prospect in the central part of the project that sits outside the resource entirely and has already returned 10 metres at 1.43% rutile. Those numbers get folded into the next update.

Digging it all up means a loader and a truck rather than explosives and a crusher, since the rutile sits in soft, weathered dirt. Mining rarely comes cheaper.

The deeper rigs that started turning last week are pointed straight at making it bigger. A maiden number this size off drilling this shallow tells you most of the deposit is still in the ground, waiting to be counted.

The Sovereign Comparison

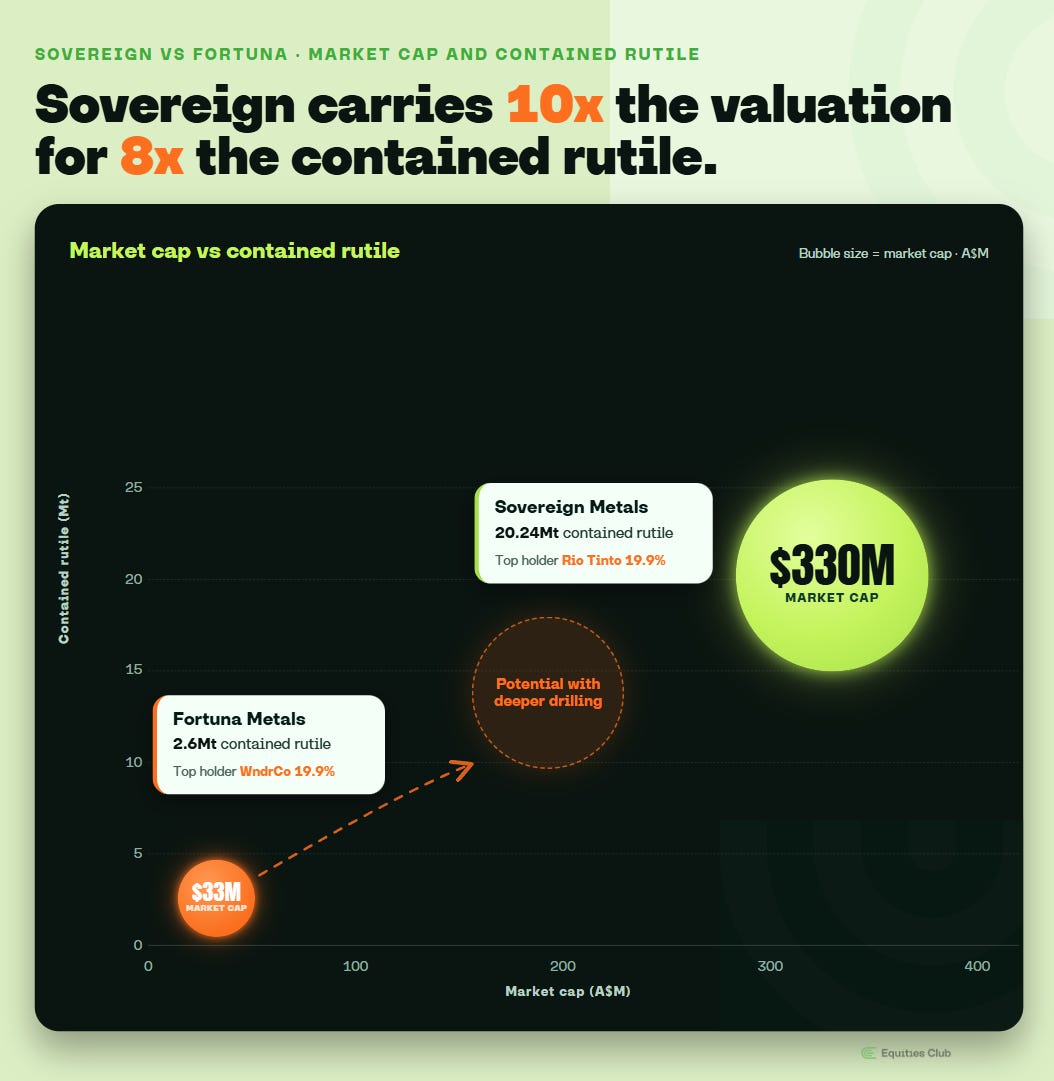

You can’t talk about FUN without talking about Sovereign Metals (ASX: SVM), the neighbour to the north.

Sovereign owns Kasiya, has Rio Tinto on its register with just under 20%, and has pushed the project all the way through a Definitive Feasibility Study. It’s a $330 million company.

FUN is worth $33 million, and on the face of it that ten-to-one gap looks absurd for two outfits sitting on the same weathered belt. The picture gets more nuanced once you dig in, but the case for FUN being underpriced still holds.

Kasiya carries roughly 20 million tonnes of contained rutile against Mkanda’s 2.6 million, so on raw size the deposit up the road is far bigger and much better understood. A bankable study and years of drilling will do that.

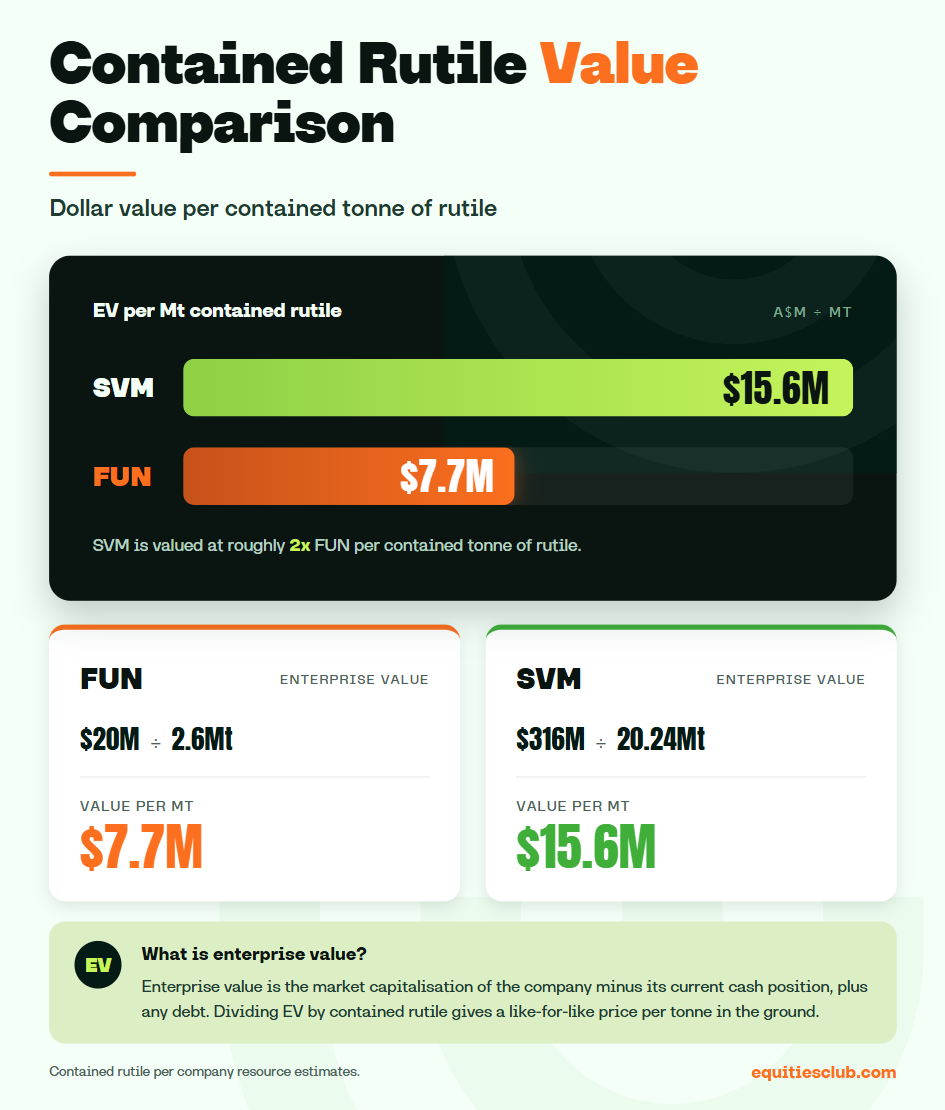

The gap tells a different story once you price the rutile itself. Strip out the cash each company holds and look at what the market pays per tonne of contained rutile in the ground.

Sovereign sits at roughly $15.6 million for every million tonnes. FUN comes in near $7.7 million on the same measure, for a deposit on the same belt.

Some of that discount is fair, since Sovereign has a finished feasibility study and Mkanda has a maiden resource off shallow holes.

What the discount ignores is everything Mkanda hasn’t drilled yet.

Then we move onto rutile equivalent, which rolls the graphite credit into a single number so you can line deposits up on one measure. Mkanda comes in at 1.57%, a touch above the 1.51% Sovereign booked in its reserve.

So FUN is cheaper per tonne and carrying slightly better grade on top.

In the year after its first proper drill results, Sovereign grew from a small explorer into a company worth more than $150 million. By the time SVM released its first resource, the market capitalisation had hit $321 million.

FUN is walking the same road, on the same ground, with a maiden resource already in hand, at a sliver of that valuation, just $33 million.

FUN's ground sits about 20 kilometres from Lilongwe and close to the Nacala rail corridor, a line running to a deep-water port in Mozambique that's the target of a $7 billion Japanese-government-backed upgrade.

It's the same track Sovereign is counting on to move Kasiya's product to market, already in place, already being spent on.

Why The World Needs More Rutile

Natural rutile is the scarce end of the titanium world. Most titanium feed comes from ilmenite, a lower-grade mineral that has to be chemically upgraded before it’s any use.

High-grade natural rutile like Mkanda’s skips that step and goes almost straight into the process, which is why it commands a premium and why fresh supply is so sought after.

Rutile sells for anywhere from US$1,100 to US$1,700 a tonne today, and the supply side is heading the wrong way. The old mines that have carried the market for decades are running down, and there aren’t many new ones coming through to replace them.

Titanium goes into jet engines and defence hardware, and it’s turning up more and more in robotics, where its blend of light weight and strength is tough to beat.

Tesla alone wants to build a million Optimus robots a year, and every machine that walks off a line adds another draw on the same tight pool of metal.

The US imports every gram of its titanium sponge and more than 70% of it came from Japan in 2025. Japan’s producers need a steady feed of natural rutile to keep their plants running.

China now sits on around 70% of global sponge production, which is a reliance Washington is scrambling to unwind.

The whole titanium market is tipped to grow from around US$30 billion in 2025 to US$54 billion by 2034. The West is hunting for high-grade supply outside Chinese control, and a deposit near surface in a stable corner of Africa fits the brief.

From Here

The aircore rigs run through to September, chasing the rutile below the hand-auger holes, and assays from them land right through the back half of the year.

Kahuna folds into the next resource update. Then before Christmas the rigs get their first look at Kampini, FUN's second project 40 kilometres south, which has never been drilled.

Get those right and the 2.6 million tonnes becomes a starting point.

The usual maiden-resource caveats apply here, with the estimate sitting in the lowest JORC confidence category and the metallurgy still being proven. Malawi’s approval timelines are unproven too, and Sovereign will be the first to take a rutile mine through them.

We backed FUN at 4 cents because it was drilling the right ground next to the right neighbour. That neighbour spent years and a lot of money to build a 20 million tonne resource.

FUN just booked its first 2.6 million with hand tools and sits at a $33 million market cap. Sovereign is worth ten times that, one belt over.

The drills will spend the rest of the year working on the difference.