Weekly Wrap: AI1 Goes Vertical, Cochlear's Confession and the Copper Setup

Weeks like this one don't come around often

Adisyn (ASX: AI1) was 6.8c when we told readers it had been added to the Equities Club portfolio. By Friday afternoon it was 20c.

In the four trading days between those two prices, a tech company a lot of our readers hadn’t heard of seven days earlier topped the ASX gainers board and added around $110 million to its market cap.

Weeks like that don't come along often.

AI1 had spent six years on a problem the semiconductor industry had not cracked in a decade.

They landed the microchip result on Monday, signed an exclusive worldwide licence on stealth drone material on Wednesday, and had a $14 million book filled mostly by Israel’s largest investment house and Regal Funds Management on Thursday.

By Friday's close, all the week's news was in the share price.

A lot of you got in on Monday. The posts started popping up not long after and didn’t slow down as the stock nearly tripled and hit daily volume records.

Six years of work for the Adisyn team. Four trading days for the market to catch up. And there’s plenty more to play out from here.

What caught our eye this week:

Mount Ridley kicks off a 17,000-sample re-assay across Grass Patch

Asian Battery Metals locks down 100% of Maikhan Uul ahead of fresh Mongolian drilling

Goldman Sachs holds 2026 copper forecast at US$12,650/t, flags DRC supply risk

Cochlear cuts net profit after tax guidance by 30%, share price at a decade low

Canaccord forecasts a structural lithium deficit through to 2035

PLS posts 52% revenue jump for the March quarter, share price testing $6 again

But first, who is Adisyn and what just happened...

AI1: From Tel Aviv to the Top of the ASX

A handful of people in a lab in Tel Aviv have been working on the same problem since 2020. The chip industry has been working on it for over a decade.

On Monday morning, Adisyn's team got there first.

That's the short version of what happened to AI1 this week. Here's the longer one.

Most chip factories on the planet make their chips with copper wiring. The wiring has been getting thinner with every new generation, and it's now thin enough that signals are stalling and resistance is climbing.

Graphene is the answer everyone agrees on. A sheet of carbon one atom thick, conducts electricity better than copper, holds up at dimensions where copper physically gives out.

The catch has always been making it. Graphene normally needs about 1,000 degrees Celsius to grow. A real chip factory caps out at 450. Cook a chip at a thousand degrees and you get a puddle.

That's the problem AI1's team in Tel Aviv has been chasing since 2020. On Monday morning, they cleared it. Full-coverage graphene on a 1cm by 1cm coupon, grown below 450 degrees.

No one else has done it. Imec, the Belgian research hub the entire chip industry uses to figure out what's coming next, has been publicly naming graphene as the answer for years.

AI1 just delivered the first version that actually works.

The market noticed by Monday afternoon. Around 40 million shares changed hands for roughly $3.5 million in turnover, a new all-time volume record for AI1.

Then Wednesday happened.

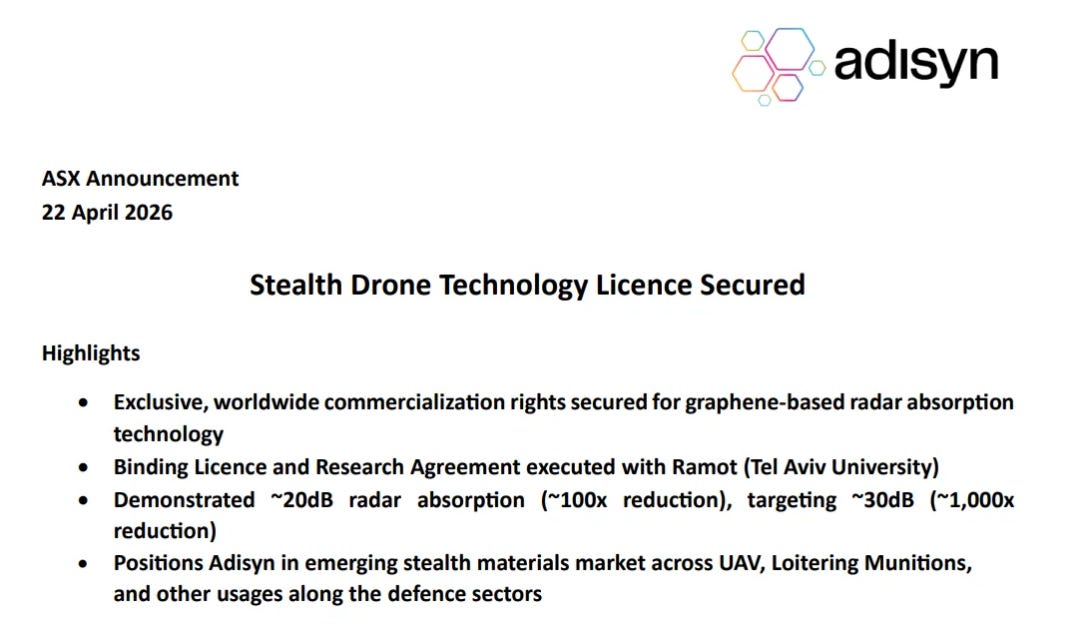

AI1 announced an exclusive worldwide licence with Ramot, the commercial arm of Tel Aviv University, on the same graphene platform - this time pointed at making a drone that radar can't see.

Right now, a quadcopter drone on a military radar screen reads as roughly the size of an F-35 fighter jet. Adisyn’s tech has already shrunk that signature by 100 times in lab testing. A full attack drone now reads on radar somewhere closer to a bird.

The next target is 1,000 times, where the drone shows up looking more like an insect than an aircraft.

Two breakthroughs inside 48 hours, on the same graphene platform, pointed at two markets each tracking toward hundreds of billions of dollars.

Thursday morning, AI1 announced a $14 million placement at 6.75c. Cornerstoned by Meitav, Israel's largest investment house with roughly A$190 billion under management.

Meitav cornerstoned another Israeli ASX-listed deep-tech company called Weebit Nano (ASX: WBT) in 2021. WBT now trades at a market cap just shy of A$1 billion.

They were joined in AI1 by Regal Funds Management, which has A$20 billion under management and a long track record of being early on good ASX tech.

Chairman Kevin Crofton and non-executive director Dominic O'Hanlon also tipped $200,000 of their own cash in on top, subject to shareholder approval.

Funds with $210 billion between them don't show up to a $14 million book unless they've spent serious time on the file.

The trading on Thursday set a new record. Over 60 million shares changed hands. Friday slotted in at 43 million, the second-biggest day in the company's history.

The volume record AI1 had held since Monday was beaten twice in three sessions.

Sitting behind all this is a capital-light commercial model. AI1 licences the tech, clips royalties, and lets someone else build the factories.

The global chip market is tracking toward US$1 trillion a year later this decade. Military drone spending alone is forecast to climb from around US$20.7 billion this year to US$66.5 billion by 2035.

AI1 doesn't need to own much of either market to justify a valuation several multiples above where it sits today.

Two weeks ago AI1 barely registered on the ASX. This week it was the biggest gainer on the ASX, with the smartest money in Israel and one of the sharpest small-cap funds in Australia on the new register. Equities Club subscribers had been told the Sunday before that a new addition was coming.

The market knows AI1 exists now. From here, the milestones do the talking. Repeatability testing on the chip side, the 30dB target on the drone side, and first commercial conversations with the chipmakers Crofton spent thirty years selling into.

All of that could be inside the next 12 months.

We’re not done with this story. Not even close.

MRD Opens a Low-Cost Path to Resource Growth

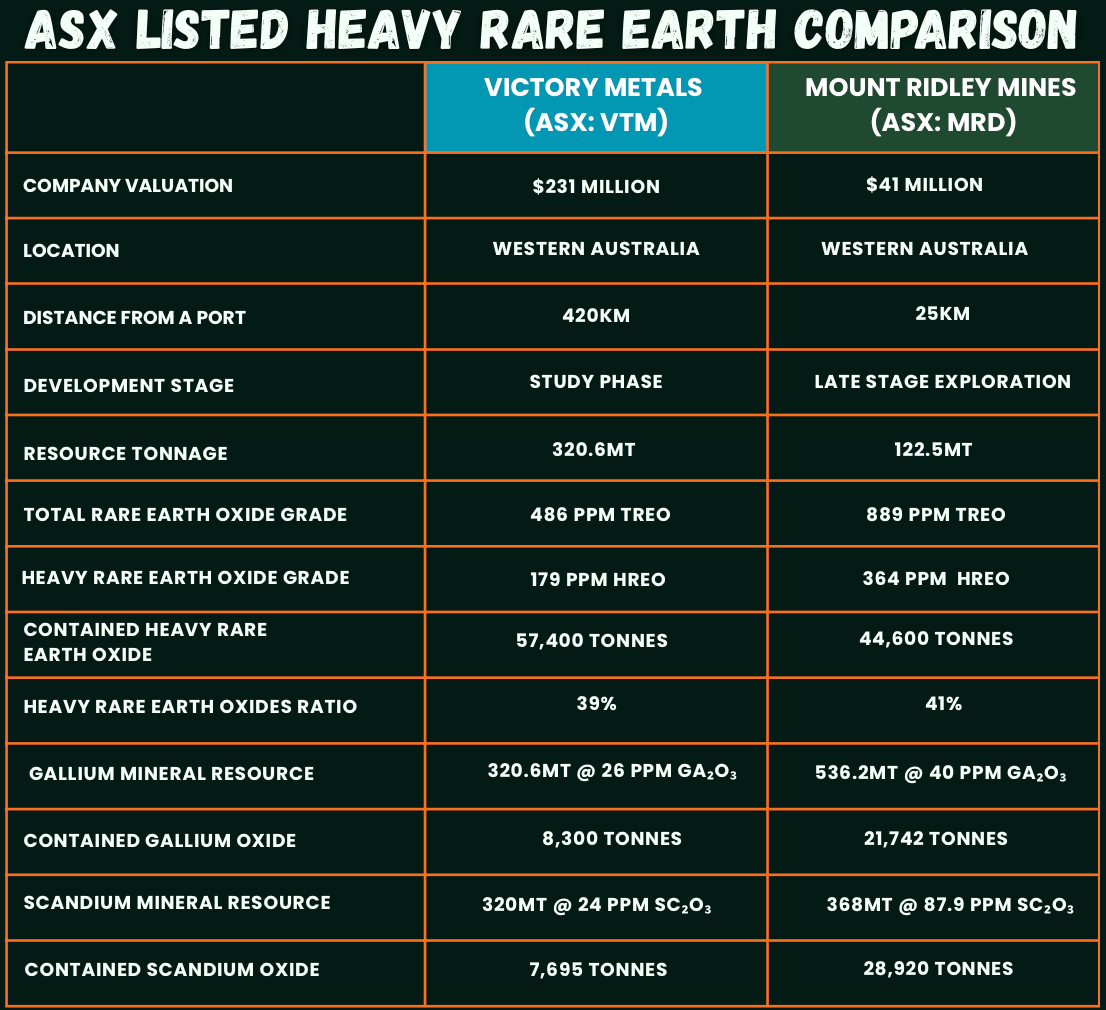

Mount Ridley Mines (ASX: MRD) is one of our portfolio companies, and it sits on three commodities the West desperately needs to source outside China - heavy rare earths, scandium and gallium.

All from one deposit in Western Australia, 25km from the deep-water port at Esperance.

This week MRD took a useful step toward growing the resource without spending much to do it.

The company submitted around 3,300 historical drill samples to the lab, the first batch of a broader 17,000-sample pipeline the team turned up while cleaning out their database.

The work targets better coverage across heavy rare earths, scandium and gallium, with the aim of lifting both the scale and the confidence of the current resource.

Most of these samples were drilled years ago when MRD was hunting nickel and copper. Nobody thought to test them for rare earths at the time. Now they’re sitting in storage, already paid for, ready to go.

For a junior, re-assaying samples already on the shelf is about as cheap as exploration gets.

It also feeds the story we keep coming back to on MRD, which is how wide the valuation gap has become with peer Victory Metals (ASX: VTM). VTM is trading at around a $230 million market cap this week, with MRD at around $41 million. VTM has one commodity. MRD has three.

On contained heavy rare earth oxide tonnage alone, MRD holds 44,600 tonnes against Victory’s 57,400.

That’s not a six-times difference.

If the re-assay work delivers the resource growth management expects, the gap between what MRD owns and what the market is paying for it gets harder to justify with every batch of results.

AZ9 lines up a fresh Mongolian drill run

It has been a little while since we last checked in on Asian Battery Metals (ASX: AZ9), but activity is picking up again across its Mongolian copper-gold ground.

AZ9 is a small-cap copper explorer with two discoveries in southwestern Mongolia, sitting eight kilometres apart in the same volcanic belt.

The flagship is Oval, a copper-nickel-PGE deposit that delivered 95% copper recovery rates earlier this year. That puts Oval inside the top 10 reported copper deposits globally for recovery, at a $18 million market cap.

The newer discovery is Maikhan Uul, eight kilometres up the road. A twin hole drilled in October pulled more than 20 metres of massive sulphide outside the existing resource boundary.

This week AZ9 took 100% ownership of Maikhan Uul. Drilling kicks off within a week as part of a broader 2026 campaign across the Yambat district.

The earlier work has already confirmed thick massive sulphide mineralisation, including a standout intercept of 14.5 metres at 2.23% copper and 0.73g/t gold, alongside multiple supporting zones of copper and gold mineralisation extending to at least 215 metres depth and open along strike.

Maikhan Uul also sits just eight kilometres from the Oval discovery, where AZ9 has already hit sulphide-rich mineralisation and identified what looks like a developing feeder-style system beneath the existing zone.

For that pipeline of targets, AZ9 still trades at roughly an $18 million valuation with around $6 million in cash.

If the upcoming drilling can repeat or extend those earlier sulphide intercepts, the market probably will not leave it sitting at this level for long.

Copper’s second-half setup keeps getting more interesting

Copper is back to looking like a second-half story.

Goldman Sachs held its 2026 copper price forecast this week at an average of US$12,650 a tonne. They also flagged real supply risk if the Middle East disruption drags on.

Their longer-run 2035 target sits at US$15,000 a tonne, but the near-term story is running on the supply side.

Sulphuric acid and diesel flows have been knocked around by the shipping disruption in and around the Strait of Hormuz, and it is landing on African copper producers first.

The most exposed are the operations using a chemical leaching process called SX-EW, which accounts for roughly 17% of global copper supply. The DRC has the largest concentration of these mines and is sitting on two to three months of acid inventory.

If delays push past late May, Goldman estimates DRC production alone could be curtailed by around 125,000 tonnes this year.

Demand is climbing on top of all that. Power grids are chewing through more copper as electrification rolls out, and AI data centres are adding another leg.

New supply is slower to respond than it used to be, with permitting timelines extending and grades falling.

Even on flat demand, the market looks short. Every junior copper hit gets a tailwind in this market.

Cochlear's Worst Day in Years Wakes Up Confession Season

One of the ASX's most reliable defensive names dropped nearly 40% in a session this week. Cochlear (ASX: COH) doesn't usually do that.

Cochlear is a global medtech that makes implantable hearing devices sold into hospitals across developed markets. The company has traded as one of the steadier operators on the ASX for years, which is why the downgrade landed as hard as it did.

The company cut FY26 profit guidance guidance to $290-330 million from $435–460 million. That is a ~30% reduction at the midpoint, wiped about $4 billion off the market cap in a single session, and sent the share price to a decade low around $100.

Developed market implant volumes have softened since January, with Western Europe particularly weak, and the stronger Australian dollar is doing extra damage on top.

Middle East disruption added cancellations, delivery delays and a one-off provision for receivables.

Small caps do this from time to time. A $10 billion medtech rarely does.

A defensive name issuing a downgrade of this size makes the rest of confession season worth reading carefully.

Lithium's Deficit Story is Back on the Table

Lithium sentiment has had a brutal couple of years. The long-term supply picture is starting to reassert itself anyway.

Canaccord is now calling a material structural deficit from 2026 through to 2035, driven by a chronic lack of investment in new supply rather than runaway demand. Even if higher prices in 2027–28 trigger a supply response, they say the gap stays open.

Markets are starting to respond.

PLS Group (ASX: PLS), the renamed Pilbara Minerals, dropped its March quarter today. The numbers land hard in this direction.

Revenue up 52% quarter-on-quarter, realised spodumene prices up 61%, and cash margin from operations up around 178%. The share price is up roughly 35% year-to-date and testing A$6 again.

That matters well beyond the majors.

Lithium juniors were the first names crushed on the way down, and they are usually the first to move when confidence comes back. The supply picture is now pointing the right way, and the money that left during the glut has a reason to come back.

The Wrap

There are weeks in this game that justify the rest of the years and weeks that test whether you should have got into it at all.

This one was the first kind.

There’s also a particular discipline required not to mistake one good week for the shape of a year. The job from here is finding the next one.

Some of the names in the rest of the portfolio are moving - MRD’s pulps to the lab, AZ9 to Maikhan Uul, copper tightening, lithium reasserting - but those stories will tell themselves in their own time, and we will be here when they do.

We’ll be back on the hunt tomorrow.

Till next week.

Adysin looks like a pump n dump