FUN Puts a Number on Mkanda. And it's a Big One

A maiden exploration target built from just three months of shallow drilling. The deposit probably goes a lot deeper.

Fortuna Metals (ASX: FUN) just put a number on its Malawi rutile project, and it’s a big one.

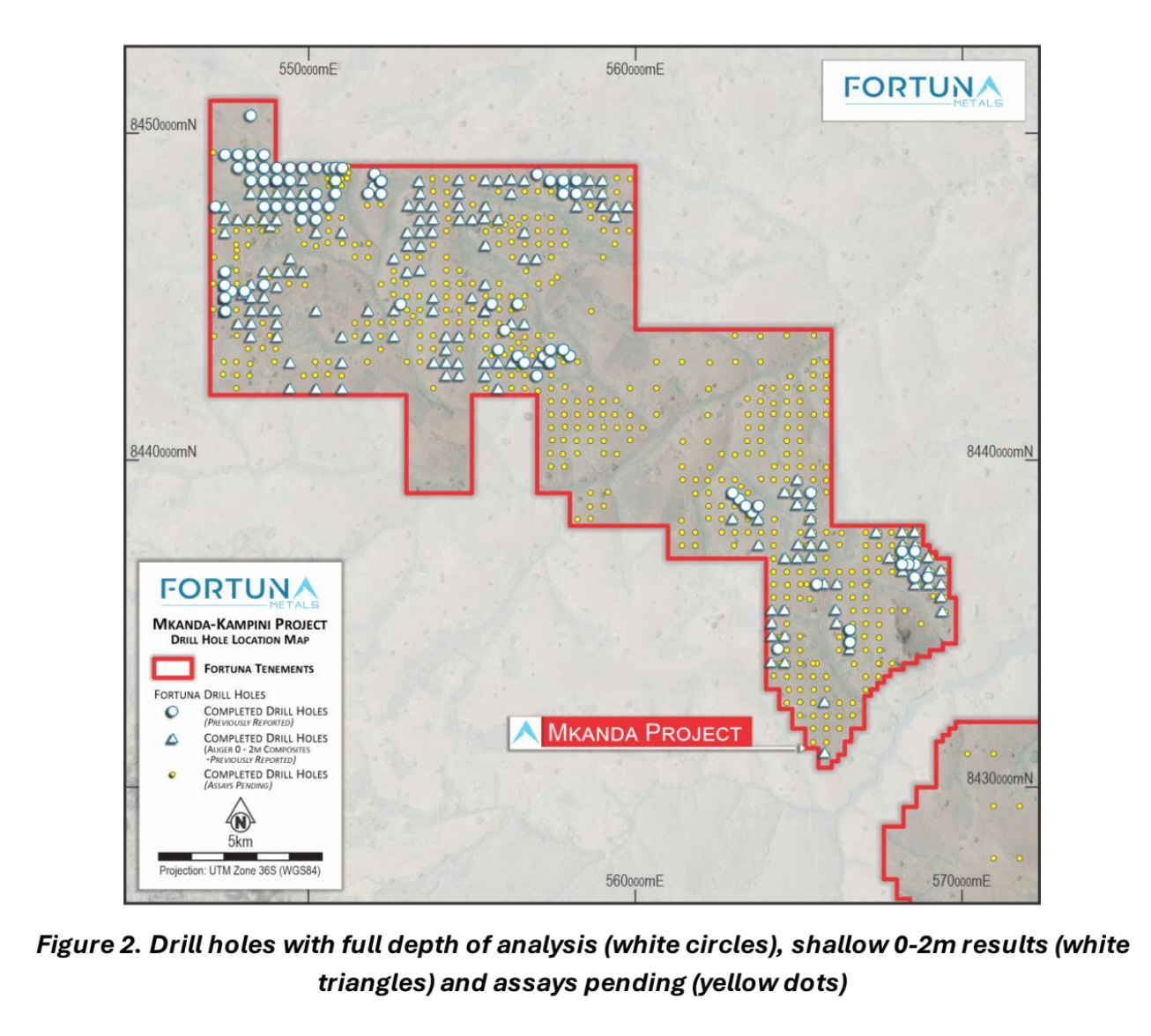

A maiden exploration target of 180 to 240 million tonnes grading 0.86% to 1.0% rutile, outlined in roughly three months of drilling since FUN acquired the Mkanda project.

We added FUN to our portfolio at 4c because the geology looked like a continuation of Sovereign Metals' (ASX: SVM) Kasiya, the world's largest rutile deposit, sitting 20km to the north.

SVM is valued at around $450 million. FUN trades at roughly $25 million, and today is the first time the story has real tonnage behind it.

But the number that matters most for FUN might be 4.1 metres, the average depth the assays actually cover. The holes went to around 8 metres and the mineralised system at Kasiya runs 20 to 30 metres deep, so FUN hasn't come close to testing the full extent of what's there.

Only a third of Fortuna’s 359 holes have been fully assayed. Aircore drilling starts in late May to push below the water table and test the deeper system, and if Mkanda behaves anything like Kasiya did when deeper drilling started, this target is a fraction of what’s there.

Three months of drilling. That’s all it took to outline a target already sitting in the same league as globally relevant rutile deposits.

FUN now has a published exploration target on ground directly along strike from the world’s largest rutile deposit, and the share price still doesn’t reflect it. We think that changes from here.

Why Rutile, Why Now

We wrote about the humanoid robot angle back in November and said it was moving quicker than most people expected.

We undercooked it.

This has moved past demo reels and conference-stage theatre. The factory rollout is already happening.

A week ago, Foshan opened China’s first automated humanoid production line. It is built for more than 10,000 units a year and is turning out one robot every 30 minutes.

They’re not the only ones scaling up.

Agibot just rolled out its 10,000th humanoid. Unitree (who’s about to go public at US$610 million) shipped around 5,500 last year and is targeting capacity of up to 75,000 a year.

Tesla has repurposed part of its Fremont factory for Optimus production. Figure AI is sitting at a $39 billion valuation. Boston Dynamics has its entire 2026 Atlas production already spoken for by Hyundai and Google DeepMind. We could go on.

The industry has evolved from a dancer in spandex on a Tesla stage five years ago to real factories shipping real robots at increasing scale.

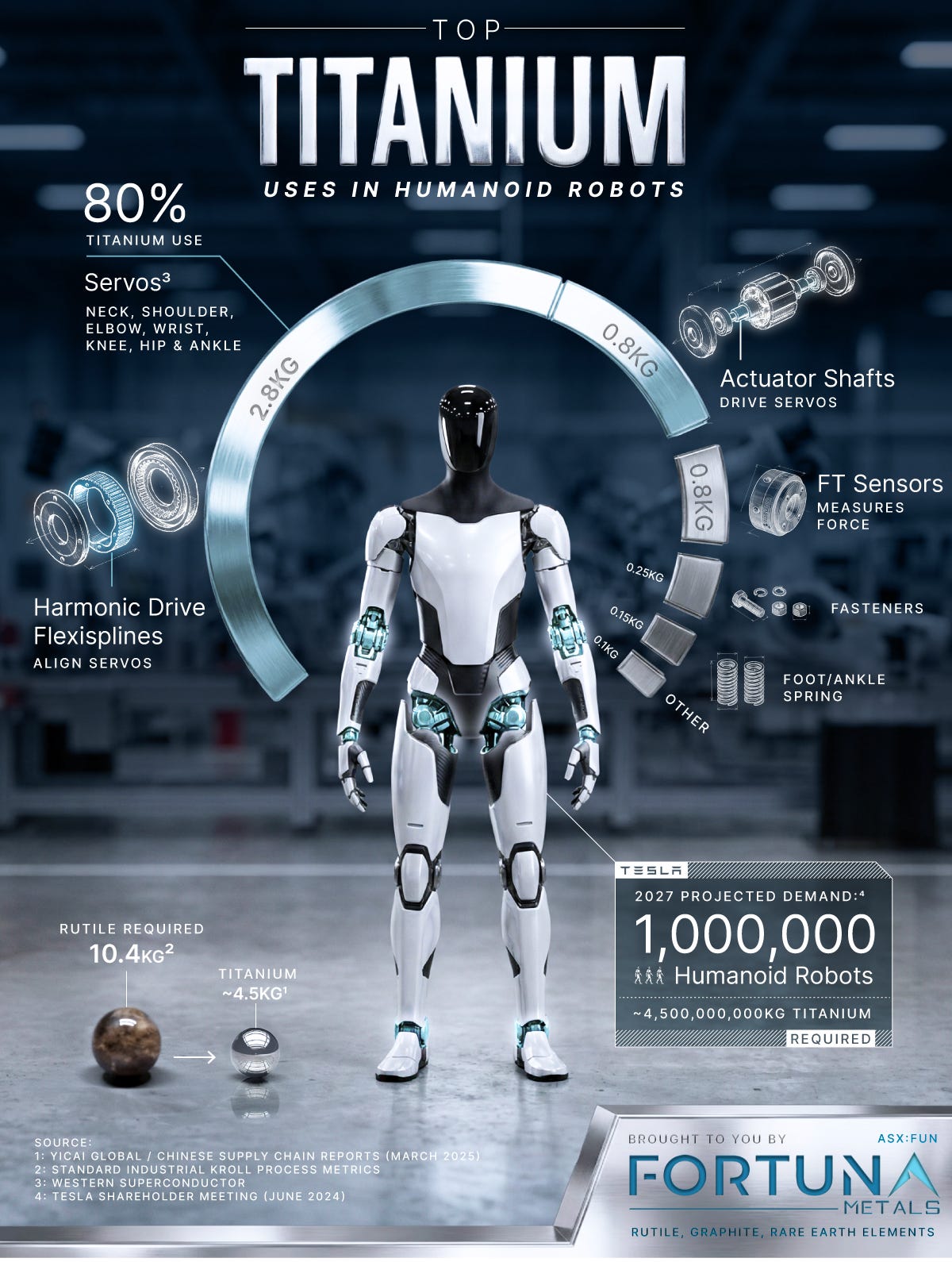

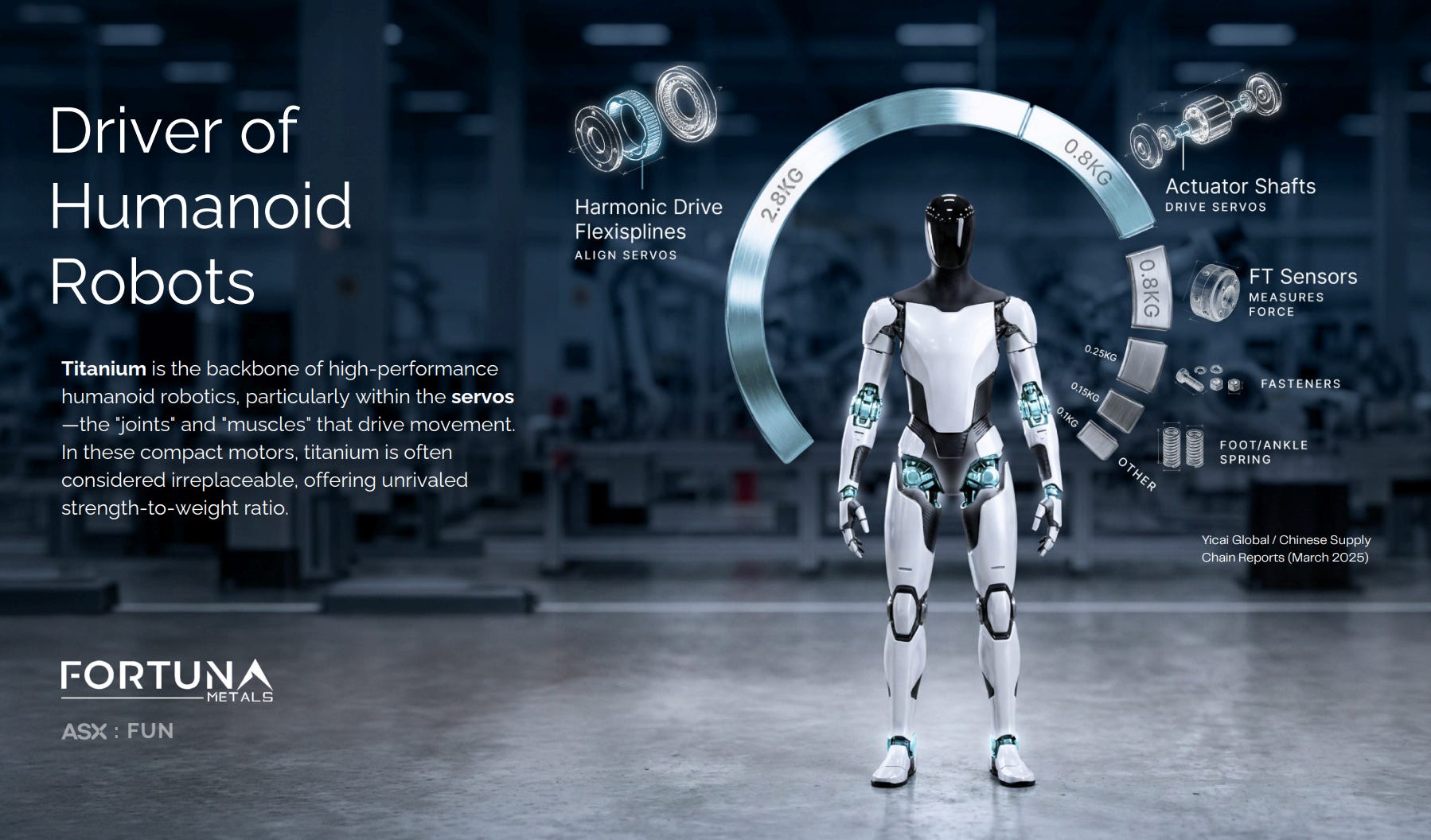

Every one of these robots needs titanium. The frames, joints and structural components rely on titanium alloys because nothing else gives you the same strength at the weight.

Fortuna’s Malawi project sits along strike from the world’s largest rutile deposit and has only been tested to shallow depths so far.

Rutile is the cleanest, highest-grade natural feedstock for titanium production. It sits at the top of the feedstock pyramid, and processors pay a premium for it because lower-grade alternatives like ilmenite cost more to upgrade and create more waste.

Each humanoid robot is estimated to contain around 10.4 kilograms of rutile.

Factories are already producing 10,000 units a year. Others are planning for hundreds of thousands.

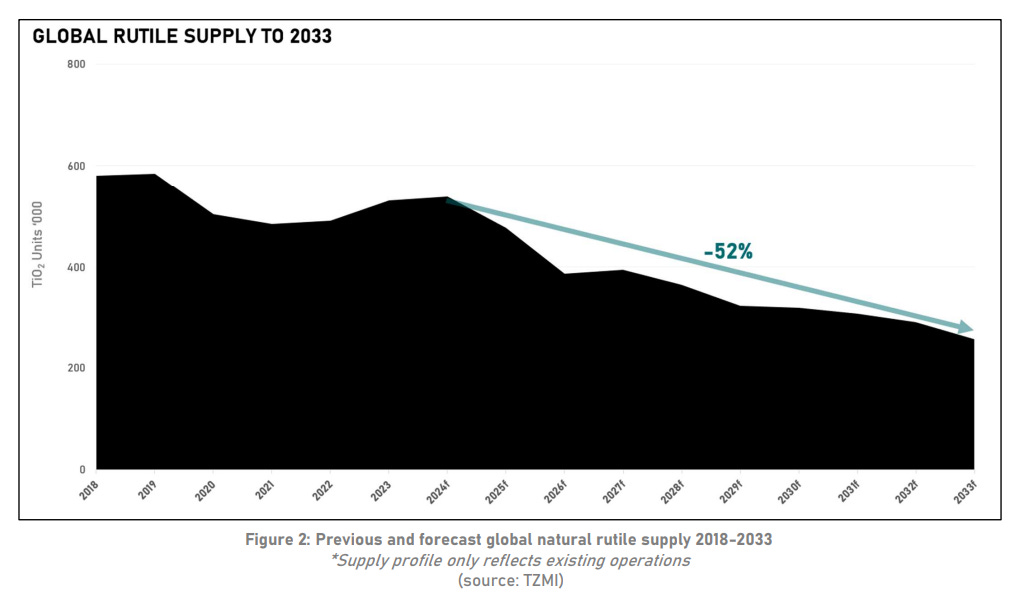

That’s a lot of rutile, and there aren’t many places to get it.

Natural rutile deposits are rare and legacy producers are in decline. And titanium demand is only going one way as robotics, aerospace and defence all scale up.

Fortuna Metals is one of a handful of ASX companies sitting on a large-scale rutile system with real drilling behind it. Mkanda sits 11km from a major railway connected to the deep-water port at Nacala, one of the best export corridors on Africa’s east coast.

The demand story and the deposit are lining up at the same time.

That doesn’t happen often.

How These Deposits Get Bigger

Rutile at Mkanda sits inside a weathered layer of rock called saprolite. Tropical weathering has been breaking down the original rock for millions of years, and the rutile concentrates through the full depth of that weathered zone.

The deeper you drill into it, the more rutile you tend to find.

The hand auger rigs FUN has been using can’t push past the water table. Once the ground gets saturated, the samples turn to mush, and at Mkanda that’s been cutting holes off at around 8 metres.

Aircore drilling, which starts in late May, solves that problem.

It punches through the wet ground and keeps going until it hits saprock, the hard unweathered rock at the base of the system where the mineralised zone ends.

At Kasiya, that base sits 20 to 30 metres down. When Sovereign tested that deeper zone at Kasiya, the resource went from 644 million tonnes to 2.1 billion tonnes.

FUN is at the stage Sovereign was before that growth kicked in.

Another 245 holes worth of assays are still in the pipeline too, so even before the deeper drilling starts there’s more data coming through.

The Valuation Gap

An exploration target tells you potential scale based on initial drilling and geological interpretation, and further work is needed before a formal resource can be declared.

But it does let you start comparing apples with apples.

FUN’s target of 180 to 240 million tonnes is roughly one tenth of Kasiya’s 2.1 billion tonne resource. One tenth of SVM’s $450 million valuation would imply about $45 million.

FUN trades at roughly $25 million.

That’s already a gap, and it’s based on a target built from shallow drilling with two thirds of the assays still outstanding. There are clear pathways for it to grow:

Deeper drilling toward the 20-30 metre saprock boundary starting in late May

Another 245 holes worth of assays still in the pipeline

Resource drilling on a 200m grid starting late April, aimed at supporting a maiden inferred resource in H2 2026

Graphite results from 241 holes expected in Q2

Each of those could change how much of the Lilongwe Plain mineral system ultimately sits within Fortuna’s tenure.

We've done this comparison in past articles and the numbers keep moving in FUN's favour. Back in 2019, SVM was valued at around $35 million and was just starting to show rutile continuity across its ground. Twelve months later it was $160 million.

FUN is sitting below that starting line with three batches of drill results and a published exploration target already in hand.

And FUN has barely scratched the surface of its own ground. The Mkanda and Kampini licences cover 658 square kilometres of the same geological corridor that hosts Kasiya. FUN controls roughly 70km of strike along it.

So far the company has drilled 675 holes across about 180 square kilometres, all on wide 400 to 800m spacing designed to find the mineralised zones.

Kampini, the southern licence, has had almost no work done on it yet.

The exploration target released today covers a portion of one project. The corridor keeps going.

Graphite is the Bonus Round

Today's exploration target is rutile only. But Mkanda is a multi-commodity system, and graphite assays from 241 drill holes are expected in Q2.

At Kasiya, graphite changed the economics of the entire project. The ore reserve went from 1.03% rutile to 2.00% rutile equivalent once graphite credits were included. It effectively doubled the payable mineral content from the same tonnes of rock.

That change helped demonstrate that the deposit could supply both titanium feedstock for aerospace and industrial markets and graphite that goes into energy storage and battery manufacturing.

POSCO, one of the world's largest battery materials manufacturers, confirmed that graphite from Kasiya could be processed into material suitable for lithium-ion batteries.

That’s not a formal offtake agreement, but it shows graphite in this corridor can support a second customer base separate from rutile buyers.

SVM also recently signed an offtake MOU with Traxys, a major global commodity trader, covering up to 80,000 tonnes per annum of Kasiya graphite.

Graphite grades at Kasiya increased with depth. FUN hasn’t tested that deeper zone yet, and aircore drilling will be the first real look at whether the same pattern holds at Mkanda.

If it does, FUN goes from a rutile story to a rutile-plus-graphite story, and that’s a very different conversation with offtake partners.

Our Take

We got into FUN at 4c. At 8.3c with a published exploration target and drilling about to step up across two programs, we’re comfortable holding.

The news flow runs through the rest of the year. Remaining assays, deeper drilling, graphite results, and a maiden inferred resource targeted for the second half of 2026. That’s a lot of catalysts for a $25 million company sitting on the same corridor as a $450 million peer.

This is still early-stage exploration. Drilling can throw curveballs and resource estimates don't always land where early results suggest.

But we think FUN is one of the most mis-priced small-caps on the ASX right now, and today’s announcement is the first real proof of scale behind that view.