Weekly Wrap: Ceasefire Chaos, Moonshots and Gunfire in Mexico

Astronauts circled the Moon, an MD dodged bullets in Mexico, and the ASX bounced hard on ceasefire headlines. Plus drill targets, big tonnage and clean tech having a moment

Astronauts splashed down in the Pacific yesterday after circling the Moon for the first time in half a century. Earlier in the week, a small-cap MD was landing his plane unscheduled after taking gunfire from the ground in northern Mexico.

Somewhere between lunar orbit and cartel airspace sits the reality of small-cap investing in 2026.

Clean-tech stocks ripped higher, the ASX bounced hard after Easter on ceasefire headlines, and gold held steady around US$4,750 while oil swung US$16 in a single session.

The Equities Club portfolio had met results, resource estimates and drill-ready targets dropping through the noise.

Let’s get to it.

Ceasefire headlines moved oil markets but gold holds steady

Artemis II circled the Moon, putting space tech back on the radar

MRD metallurgy at Grass Patch stacks up well

FUN outlines major rutile scale potential at Mkanda

10X defined drill targets ahead of Peak View drilling

Three cleantech names that ripped 45-65% this week

Shots fired in Mexico (a reminder investor risk comes in many forms)

Leadership changes as DroneShield slips despite sector demand

Ceasefire? Markets Up, Gold Steady, Oil All Over the Place

A US-Iran ceasefire was signed this week and oil dropped US$16 in a session, and the ASX ripped 2.5% higher on the back of it.

Then Israel hit Lebanon and everyone remembered how shaky a Middle East ceasefire can be.

The ASX pushed to 8,960 by Friday, its best weekly gain since 2020 and within striking distance of all-time highs. But anyone trading oil this week earned their grey hairs.

The Strait of Hormuz is still only partially reopening, and nobody seems sure whether this ceasefire holds long past this weekend’s marathon talks in Islamabad.

Gold held around US$4,750 per ounce throughout it all, which tells you the bid underneath the metal is structural. Sovereign buying and inflation hedging are propping up the price more than any single headline at the moment.

China’s central bank has added to its gold reserves for 17 straight months now. At that pace it sets a floor under the price and it almost doesn’t matter what happens in Lebanon or Iran on any given Tuesday.

Silver continued to track higher alongside gold and remains near multi-decade highs, backed by safe-haven flows and ongoing demand from solar and electrification.

If gold and silver stay anywhere near these levels, money keeps finding its way into the small-cap explorers trying to pull them out of the ground. We're already seeing that across a few of our portfolio names.

From Artemis to the ASX?

Four astronauts splashed down in the Pacific yesterday after spending ten days circling the moon. The last time anyone did that, Gough Whitlam had just moved into The Lodge.

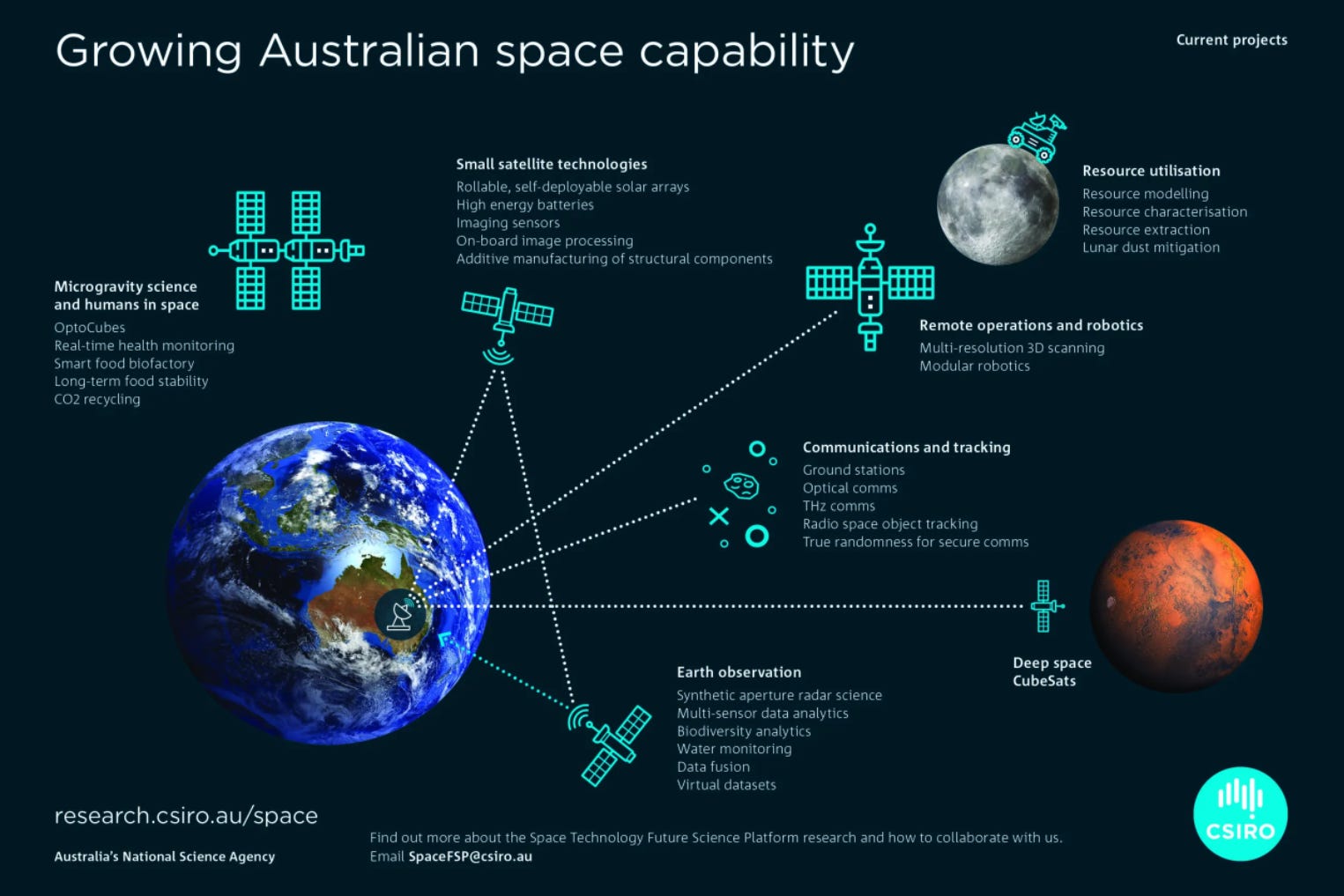

It's easy to write it off as a (very cool) NASA headline with no ASX angle, but the infrastructure keeping those astronauts alive runs through some interesting ground.

It often sits inside the same technology stack as defence electronics and satellite infrastructure.

Australia’s own deep-space tracking capability supported the mission through CSIRO facilities in Canberra, a reminder that global lunar programs rely on distributed ground networks as much as launch vehicles.

As NASA pushes toward a permanent lunar presence, that capability will only get more valuable.

A couple of ASX names sit in the orbit of all this (pun intended).

Electro Optic Systems (ASX: EOS) develops the tracking systems that monitor satellites and debris in orbit using ground-based optical networks. More missions mean more stuff in orbit and tracking infrastructure becomes critical for managing congestion and collisions across busy space corridors.

Gilmour Space Technologies (upcoming IPO) raised $217 million in Series E funding recently, valuing the company above $1 billion. They're building the Eris orbital rocket and a spaceport in Queensland. The rocket is still in testing, so there's plenty of execution risk, but the money flowing in tells you how serious people are getting about Australia having its own launch capability.

We're some ways away from space stocks being a mainstream ASX theme. But every time a crew goes around the Moon and comes back safely, the investment case for the ground infrastructure gets a little harder to ignore.

Mets Looking Good for Mount Ridley Mines

Mount Ridley (ASX: MRD) closed the week up 7% to 3.2c after metallurgical results answered the biggest question hanging over the Grass Patch heavy rare earth project: can you actually get the good stuff out?

The testwork confirmed that dysprosium and terbium can be extracted using a simple acid leach pathway, with recoveries up to 86.5% in some samples.

Those two elements sit at the very top of the heavy rare earth value chain and are among the hardest to source outside China, which is exactly why projects like Grass Patch are attracting more attention globally.

The metallurgy already works before optimisation has even begun. That’s a good starting point.

The next round of testwork targets dysprosium and terbium extraction from within the defined resource, which is where projects typically start moving from interesting geology to something the market can begin to price more seriously.

Scandium and gallium still sit in the background as potential by-product credits, so there’s more than one pathway emerging here.

You can find our full article here.

Big Tonnage Announced for Fortuna Metals

Fortuna Metals (ASX: FUN) closed the week up 8% to 9.3c after outlining a 180 to 240 million tonne rutile exploration target at Mkanda, from just three months of shallow drilling.

At that scale, Mkanda is already a serious rutile system. And most holes so far have only gone down about eight metres. There's a lot of ground left to test.

For context, Sovereign Metals’ (ASX: SVM) Kasiya project just to the north in Malawi is the world’s largest known rutile deposit and backed by Rio Tinto, and its scale only became clear once drilling pushed deeper into the weathered profile.

FUN’s Mkanda sits along strike on the same geological corridor, and the company will now be stepping into that same deeper drilling phase where we could see this already large target grow further.

SVM is valued at roughly $450 million. FUN is currently at $26 million. Back-of-the-envelope, that disconnect suggests potential upside of about 80% from its current valuation.

There are 245 holes of assays still pending, deeper drilling about to kick off, and a maiden inferred resource targeted for the second half of the year. Graphite assays in Q2 could add another commodity layer on top of the rutile.

You can find our full article here.

10X Has Four High-Priority Drill Targets

Exultant Mining (ASX: 10X) finished the week at 18c with drilling about to kick off at Peak View. We still see this as one of the more appealing near-term setups across our portfolio.

The 50 g/t gold at Undoo Creek and 339 g/t silver at Big Badja grabbed headlines over the past month, but Peak View is the drill program 10X has been building towards since listing.

Historical drilling hit zinc, lead, copper and silver, but only tested a fraction of the system. New IP and gravity surveys have now mapped out what was missed.

The standout is a 700-metre anomaly sitting west of all previous drilling. The old holes hit sulphides next to a weaker geophysical response. The stronger one has never been touched.

A 1.1km gravity high lines up in the same spot, right on the southern continuation of the fault that hosts Captains Flat, one of NSW’s biggest historic base metal mines.

Every dataset is pointing at the same piece of ground.

Senior geologist Seb Hind walks through it in the video below.

At 18c with $4 million in cash, you're paying about $3 million enterprise value for a funded 15-hole program across multiple targets on a proven mineralised structure. Late April it kicks off.

You can find our full article here.

Small-Cap Clean Tech Stocks Clean Up

Three small-cap cleantech names put up big numbers outside the resources space this week.

Environmental Clean Technologies (ASX: ECT) ran 58% after extending its PFAS destruction technology into water filtration waste.

For those who aren't chemical engineers (like us), water treatment plants use activated carbon to filter forever chemicals out of drinking water before it reaches your tap.

The water comes out clean, but the carbon is now full of toxic chemicals and currently gets trucked to landfill.

ECT's tech destroys those chemicals on site so nothing toxic leaves the plant.

In a strong sign of confidence, the Chairman bought over 50k on market this week too.

Eden Innovations (ASX: EDE) rose 45%. They make concrete additives that cut cement use (and emissions) on big infrastructure projects.

Global construction groups are under pressure to reduce the carbon footprint of concrete, and technologies that slot directly into existing batching plants are starting to get attention.

The company cleared its debt earlier this year and is now installed across multiple ready-mix networks in North and South America, so the story is shifting from trials to repeat orders.

Sparc Technologies (ASX: SPN) climbed 65% and the ASX wanted to know why. The company’s response, more or less, was “our MD went on a podcast.”.

If you needed proof that new media moves small-cap stocks now, there it is.

Sparc makes graphene-enhanced coatings that protect steel infrastructure from corrosion.

In the podcast, MD Nick O’Loughlin said they’re testing with five of the eight largest protective coatings companies globally and are close to getting their first additive into a commercial coating line.

Their lab work has shown up to 79% improvement in how coatings resist corrosion spread. Recoating a bridge or dry-docking a ship costs a fortune. So if the paint lasts longer, you do it less.

At $20 million with first revenue only arriving in December last year, Sparc is still very early in the story and chasing a slice of a $30 billion global coatings market.

New media like podcasts is moving markets now, and where investors get their information is shifting fast.

Mayhem in Mexico

Most MDs spend their week in boardrooms. Mithril Silver & Gold's (ASX: MTH) managing director spent his dodging gunfire over Northern Mexico.

The company reported that its MD and two staff were forced into an unscheduled landing after their aircraft took fire from the ground while flying between the Copalquin silver-gold project in Durango and the city of Chihuahua.

News reports linked the gunfire to La Linea cartel activity in the area. Everyone walked away unharmed and drilling continued as planned.

Mexico is the world's largest silver producer and a lot of that output comes from the northern states where mining districts and cartel territory overlap. It comes with the address.

The incident happened away from the project site and it was described it as isolated.

When people talk about risk in small-cap investing, they usually mean dilution or a dud drill hole. Not many annual reports have a section for incoming gunfire.

DroneShield Drops as CEO and Chairman Exit

We like the drone tech space a lot. The demand story across Ukraine, the Middle East and the broader defence build-up is only getting stronger.

But DroneShield (ASX: DRO) had a rough week, falling 13% on about $334 million in traded value after a series of governance and pipeline updates unsettled investors.

Founder CEO Oleg Vornik and chairman Peter James both stepped down on Wednesday after having already sold their entire shareholdings months earlier. Holders noticed that sequence at the time, and we covered it here.

The sales pipeline also slipped $100 million, from $2.3 billion to $2.2 billion. Contract timing shifts constantly in defence procurement, but when your CEO and chairman have both walked out the door, investors often aren’t in the mood to give you the benefit of the doubt.

DroneShield still sits inside one of the fastest-growing defence technology segments globally, but weeks like this show how critical execution and communication are when valuations are already pricing in strong growth.

Hamish McLennan is coming in as chairman. He's currently chair of REA Group and well connected across corporate Australia, so the board is clearly trying to attract a different class of investor to the register.

The sector tailwind is still blowing hard. New management now needs to prove they can keep up with it.

The Week Ahead

The ceasefire talks are going to dominate everything. Pakistan-mediated talks between the US and Iran kicked off yesterday and what comes out of that room will set the tone for Monday (and potentially the foreseeable).

As markets push higher we expect gold to keep climbing as a hedge to debt, a theme that will likely take control of the news cycle again soon.

The ASX is still within striking distance of all-time highs and small-cap volumes tend to pick up when the big end of town is running.

Gold looks to have found a base around US$4,750/oz, and if we'd said that figure two years ago we'd have jumped at it. With sovereign debt piling up and inflation staying sticky, we expect that base to hold.

There's still a lot of upside in small-cap gold discoveries and developments.

A few of our portfolio names have drill programs kicking off or results pending over the coming weeks, so there’s plenty to watch.

Though as we’ve all learned by now, one post on Truth Social can rearrange the whole board.

Till next week.